Suspension of transactions on the tax account. Suspension by the tax authority of operations on the accounts of the taxpayer. How does this happen

Alexander Zrelov, Member of the Expert Council at the Chamber of Commerce and Industry of the Russian Federation

on improving tax legislation and law enforcement practice, Candidate of Yu. n.

Let us consider the features of the procedure for suspending operations on bank accounts, as well as transfers of electronic funds, taking into account the established law enforcement practice.

Suspension of operations on a bank account in the manner prescribed by law is an acceptable form of restriction of the client's rights to dispose of the funds on the account (Article 858 of the Civil Code of the Russian Federation). The purpose and consequences of such restrictions are explained by the Tax Code. However, using only the text of this article, it is very difficult to answer a number of questions related to the “account blocking” procedure and its cancellation. Therefore, many of them have already become the cause of litigation. We will draw attention to some of the decisions taken as a result of such proceedings.

Grounds for suspending account transactions

List of grounds for acceptance tax office the decision to suspend operations on bank accounts, as well as transfers of electronic funds of the taxpayer, is exhaustive, and today it consists of the following points:

The requirement to pay tax, penalties or fines has not been fulfilled (clause 2, article 76 of the Tax Code of the Russian Federation);

Requirements for the submission of explanations (clause 3 of article 88 of the Tax Code of the Russian Federation);

Notifications of a call to the tax authority (subclause 4, clause 1, article 31 of the Tax Code of the Russian Federation).

The decision to suspend operations will be made by the head of the tax inspectorate or his deputy within 10 working days from the date of expiration of the deadline for the transfer of such receipts in electronic form.

Cancellation of the decision to suspend must be made no later than one day after the transfer of the receipt or the requested documents or the appearance of the representative of the organization summoned to the inspection.

Let us once again draw attention to the fact that the obligation to ensure receipt of documents sent by the tax inspectorate also applies to persons who, not being tax payers, must submit tax returns. Consequently, the procedure for suspending operations on bank accounts applies to them.

Peculiarities of making payments during the period of restricted use of the account

To suspend operations on the organization's accounts, the tax authority makes an appropriate decision and sends it to the bank where it has an account. Only copies, but not originals, of the decisions to suspend and cancel the suspension of these operations are handed over to the organization. A reasoned justification for the need to "block an account", as well as a mandatory preliminary imposition of a ban on the alienation (mortgage) of the taxpayer's property is not required.

Suspension of transactions on bank accounts means the termination of only debit transactions, with the exception of the categories of payments expressly provided for tax code(Post. No. 1836/11 of the Presidium of the Supreme Arbitration Court of the Russian Federation dated July 5, 2011). The suspension of operations also applies to cash credited to the account after the introduction of the suspension procedure.

Article 76 of the Tax Code does not provide for the authority of the bank, at its own discretion, to suspend debit transactions on the organization's accounts (decision of the Supreme Arbitration Court of the Russian Federation dated June 15, 2011 No. VAS-3674/11). The bank has the right to write off funds from the organization's account on instructions from the tax authority in the order established by civil law.

Thus, the write-off of funds under settlement documents providing for payments to budgets, as well as the transfer or issuance of funds for remuneration to persons working under an employment contract, are made in the order of the calendar priority of receipt specified documents after the transfer of payments made in accordance with Article 855 Civil Code in the first and second order.

The Tax Code does not contain restrictions on sending collection orders to collect debts on taxes, fees, penalties, fines to an account on which operations are suspended. Suspension of operations on accounts does not prevent the fulfillment of obligations to pay taxes, fees and mandatory payments to the budget and off-budget funds, including payment and transfer:

State duty;

Taxes withheld by the organization as a tax agent from its employees;

taxes in budget system Russian Federation on executive documents of bailiffs;

Mandatory insurance premiums pension insurance;

Insurance premiums for compulsory social insurance against industrial accidents and occupational diseases.

Carrying out debit transactions on payments not preceding tax payments during the period of execution by the bank of a decision to suspend all debit transactions on the organization's accounts until full repayment the amount of tax arrears is the basis for bringing to responsibility (Article 134 of the Tax Code of the Russian Federation). The form of settlements (on the basis of a payment order or a payment request) does not affect the decision on the admissibility of making payments under the conditions of this interim measure (post. No. 1836/11 of the Presidium of the Supreme Arbitration Court of the Russian Federation of 05.07.2011).

It is important to note that the amount tax debt during the period of suspension of operations and transfers of the taxpayer, penalties continue to accrue.

The suspension applies, in particular, to operations for debiting funds by the bank from the account of the bank's client:

For payment bank commission;

For payments made with the use of payment cards before the suspension of operations on the account;

According to executive documents providing for satisfaction monetary claims another organization;

For payment of customs duties and fees, performance fee, fines imposed bailiffs.

Suspension of operations and transfers is allowed:

According to the accounts of the liquidated organization;

By accounts open bank in violation of the established ban on opening new accounts for the taxpayer;

For bank accounts opened in a non-bank credit institution for which settlements are carried out in a non-cash manner.

At the same time, in the event of the liquidation of an organization, the suspension of operations on its bank accounts does not apply to payroll calculations for persons working or working under an employment contract.

It should also be noted that in case of suspension of operations on bank accounts in connection with the activities management company it is possible to apply this restriction to accounts on which funds owned by the management company are recorded, but the suspension does not apply to accounts trust management on which the funds of third parties are recorded and stored.

The current legislation introduces a number of restrictions on the possibility of suspending operations and transfers of organizations that have signs of financial insolvency and are at risk of becoming bankrupt.

So, the tax inspectorate has no right to decide:

Restricting the right of the debtor from the date of the introduction of bankruptcy proceedings (declaring the debtor bankrupt) to dispose of the funds belonging to him in the presence of a current debt subject to collection outside the bankruptcy case;

Restricting the right of the debtor, from the date the arbitration court issues a ruling on the introduction of supervision, to dispose of the funds belonging to him;

On the suspension of any funds (including current payments) at the stage of introduction to external management organizations.

In case of suspension of debit transactions on bank accounts, it is allowed to make payments from this account in order to repay current claims (decision of the Supreme Arbitration Court of the Russian Federation dated June 15, 2011 No. VAC-3674/11) relating to the first - third queues and named in paragraphs two - four of paragraph 2 Article 134 of the Law "On Insolvency (Bankruptcy)" ( the federal law dated October 26, 2002 No. 127-FZ).

The Tax Inspectorate has the right to suspend operations on all current accounts of the organization known to it in various banks. According to the Tax Code, the suspension is not carried out to ensure the execution of a collection order sent to the bank. Therefore, it is allowed to make decisions on the suspension of operations on those bank accounts for which collection orders have not been issued (and are not planned to be issued). It is also possible to issue collection orders to one account in one bank and make a decision to suspend operations on other accounts of the organization.

Closing by a bank of accounts in respect of which a decision of the tax inspectorate to suspend operations has been made is not a basis for recognizing this decision as invalid or terminated, and also does not cancel the ban on opening new accounts for the organization in this bank. This prohibition is valid until the cancellation of the decision to suspend the organization's operations on bank accounts.

From January 1, 2014, the ban on opening new accounts of an organization in respect of which the decision to suspend operations is in force applies not only to the bank where the account of this client already exists, but also to all other banks. The procedure for informing banks about the suspension of operations and about the cancellation of the suspension of operations on the taxpayer's accounts and transfers of his electronic funds in the bank by this time should be developed by the Federal Tax Service of Russia in agreement with the Bank of Russia (Clause 12, Article 76 of the Tax Code of the Russian Federation as amended by the Federal Law dated July 23, 2013 No. 248-FZ).

Resuming account transactions

The action of the decision to suspend operations on the organization's bank accounts and transfers of its electronic funds can be terminated only by the tax authority by canceling it. The provisions of the Tax Code provide for the possibility of canceling this decision only in expressly provided cases (clause 8, article 76 of the Tax Code of the Russian Federation). Cancellation of the decision on other grounds is not allowed. The revealed fact of violations in the application of substantive law is not sufficient grounds for canceling such a decision. Revocation by the tax inspectorate of the decision to suspend operations on the taxpayer's account is also not allowed.

In the event of reorganization or liquidation of the inspectorate that made the decision to suspend, the decision to cancel it is entitled to be taken by its legal successor, as well as by a higher tax authority.

In case of exclusion from Unified State Register of Legal Entities that has terminated its activities, automatic (without the decision of the inspection) cancellation of the suspension of operations on bank accounts is not allowed.

It should be noted that the receipt by credit institutions of a court ruling on the introduction of supervision also entails the termination of the decisions available in this bank to suspend operations and transfers in respect of this taxpayer. Sufficient grounds for canceling the decision to suspend operations on the current account is the court decision to declare the debtor bankrupt and to open bankruptcy proceedings against him. In these cases, in order to remove the suspension of operations on the taxpayer's bank accounts, it is not necessary to wait for an additional decision by the tax inspectorate to cancel the suspension.

The obligation of the inspectorate to deliver the decision to cancel the suspension of operations on the account to the bank is considered fulfilled only from the moment when the decision is received by the bank. If the tax authority violates the deadline for sending to the bank a decision to cancel the suspension of operations on the organization's bank accounts, interest is charged on the amount of directly blocked funds for each calendar day of violation of the deadline (clause 9.2 of article 76 of the Tax Code of the Russian Federation). It should be noted that these interest are subject to income tax (letter of the Ministry of Finance of Russia dated February 14, 2011 No. 03-03-06/1/101).

When the tax office can suspend transactions on a current account. How to block a bank account for non-payment of taxes. What payments can be made from a current account blocked by the tax office.

Question: Tax debt. At what amount of debt does the IFTS have the right to block the account, in what time frame does this happen? Is it possible and under what circumstances the IFTS may not block the account and what is required for this, how to refer to article 64 of the Tax Code, since the company can only pay off part of the tax debt.

Answer: The tax inspectorate has the right to suspend operations on accounts in the presence of arrears. In this case, the amount of the arrears does not matter. Account blocking does not apply:

for payments, the order of which, according to civil law, precedes the fulfillment of the obligation to pay taxes, fees, penalties and fines.

Those. current payments on taxes and fees, if there are funds in the accounts, will be transferred to the budget on time, and the bank will also execute instructions for transferring payments of the 1st and 2nd priority (including wages).

The tax inspectorate has the right to remove the suspension of operations on accounts only when the taxpayer fully repays the arrears, no later than one business day following the day the tax inspectorate receives documents (copies thereof) confirming the collection of tax (penalties, fines) - if the account was blocked in connection with the organization's failure to comply with the requirements of the tax inspectorate for the payment of tax (penalties, fines)

At the same time, debit transactions are suspended only within the amount specified in the decision to suspend operations on accounts. If several accounts are indicated in the decision to suspend operations, the bank must block each of them for the amount indicated in the decision.

Deferral or installment payment of debts on taxes and fees is provided only under certain conditions established by the Tax Code of the Russian Federation

If there are such grounds, a tax deferral or installment plan may be granted to an organization for an amount not exceeding the value of its net assets.

An application for a deferral or installment plan for the payment of tax, indicating the grounds, is submitted to the appropriate authorized body (Article 63 of the Tax Code of the Russian Federation). Documents confirming the existence of grounds for obtaining a deferment or installment plan are attached to this application. A copy of the said application shall be sent by the person concerned within five days to the tax authority at the place of its registration. Upon receipt by the tax authority of a decision to defer or installment payment of debt, the suspension of operations on accounts will be lifted.

A detailed procedure for preparing documents for obtaining an installment plan (or deferment) is given in the Rationale for this answer.

Rationale

When the tax office can suspend transactions on a current account

Blocking for non-payment of taxes

How to block a bank account for non-payment of taxes

If the blocking of the account is caused by the collection of debts to the budget, the decision to suspend operations is made no earlier than the decision to collect taxes (fees, fines, penalties) is made (paragraph 2, clause 2, article 76 of the Tax Code of the Russian Federation). At the same time, debit transactions are suspended only within the amount specified in the decision to suspend operations on accounts. If several accounts are indicated in the decision to suspend operations, the bank must block each of them for the amount indicated in the decision. Suspend spending transactions currency account the inspection may for an amount equivalent to the amount in rubles specified in the decision. The recalculation is made at the exchange rate of the Bank of Russia, established on the date of commencement of the suspension of operations on a foreign currency account. This procedure is provided for by the provisions of paragraph and paragraph 2 of Article 76 of the Tax Code of the Russian Federation and is explained in the letter of the Ministry of Finance of Russia dated January 14, 2013 No. 03-02-07 / 1-6.

The funds that are in bank accounts in excess of the amount of debt, the organization has the right to use at its discretion (letter of the Ministry of Finance of Russia dated April 15, 2010 No. 03-02-07 / 1-167).

Blocking restrictions

Although blocking an account limits the organization's ability to use funds, some types of payments can still be made.

What payments can be made from a current account blocked by the tax office

Account blocking does not apply:

for payments for the transfer to the budget of taxes, fees, insurance premiums, penalties and fines.

for payments, the order of which, according to civil law, precedes the fulfillment of the obligation to pay taxes, fees, penalties and fines;

When applying the second restriction, it must be taken into account that for operating organizations, payments on bank accounts are made in the following order:

in the first place - on executive documents for compensation for harm caused to life and health, as well as claims for the recovery of alimony;

in the second place - according to executive documents for settlements on the payment of severance pay and salaries to retiring employees, as well as on the payment of remuneration to the authors of the results of intellectual activity;

in the third place - according to payment documents for calculating wages for working employees, on behalf of tax inspectorates and extra-budgetary funds to collect debts on taxes, fees and mandatory insurance premiums;

in the fourth place - on executive documents providing for the satisfaction of other monetary claims;

in the fifth place - for other payment documents in the order of calendar priority. Including payments by which organizations transfer current taxes, fees and insurance premiums.

The collection of taxes by force, that is, at the request of inspections, belongs to the third priority. Therefore, the payments of the first and second (and in some cases, third) queues will be executed by the bank unconditionally. Even if the organization's account is blocked.

If there are not enough funds on the settlement account of the organization, payments for claims related to one queue are made in the order of the calendar order of receipt of documents. For example, in operating organizations both the transfer of wages and the collection of arrears according to the requirements of tax inspectorates and non-budgetary funds belong to one - third - priority. Therefore, at first the bank will execute those payment orders that were received earlier. This rule also applies if the organization's account is blocked. This conclusion is confirmed by the letters of the Ministry of Finance of Russia dated July 11, 2013 No. 03-02-07/1/26955, dated April 19, 2013 No. 03-02-07/1/13537, dated November 6, 2012 No. 03-02 -07 / 1-279 and the Federal Tax Service of Russia dated February 27, 2013 No. AS-4-2 / 3225.

A different procedure applies if the organization is liquidated. In this case, the sequence of payments established by paragraph 1 of Article 64 of the Civil Code of the Russian Federation is applied.

First of all, the claims of citizens to whom the liquidated organization is liable for causing harm to life or health, as well as claims for compensation are satisfied:

oral harm;

in excess of compensation for damage caused by the destruction, damage to the capital construction object;

in excess of compensation for damage caused by violation of safety requirements during construction;

in excess of compensation for damage caused by violations of the requirements for the safe operation of buildings and structures.

In the second place, calculations are made for the payment of severance pay and salaries of employees, as well as for the payment of remuneration to the authors of the results of intellectual activity.

In the third place, settlements are made on mandatory payments to the budget and extra-budgetary funds.

In the fourth place, settlements with other creditors are made.

Write-off of funds from the account for claims relating to one queue is made in the order of the calendar order of receipt of documents.

Thus, an organization in liquidation has the right to spend money on payments of the first and second priority (for example, on paying salaries), even if the organization’s current account is blocked, and mandatory payments to the budget and extrabudgetary funds are not transferred. Similar explanations are contained in the letter of the Ministry of Finance of Russia dated April 8, 2011 No. 03-02-07 / 1-112.

The decision to block

The suspension of the organization's operations on its bank accounts is valid from the moment the bank receives such a decision until the moment it is canceled. At the same time, the decision to block the account does not apply to payment orders executed by the bank on the same day when the decision was received, but earlier in time (letter of the Ministry of Finance of Russia dated May 23, 2011 No. 03-02-07 / 1-169).

The bank, having received from the tax inspectorate a document on the blocking of the account, must execute it unconditionally, even if the account is blocked unlawfully (clause 6, article 76 of the Tax Code of the Russian Federation). The organization will not be able to present any claims against the bank, since the bank is not responsible for the losses incurred by it due to the blocking of the account (clause 10, article 76 of the Tax Code of the Russian Federation). In addition, the bank will suspend operations on accounts, even if, after the inspectorate decides to block the account, the organization changes its name and account details. This is stated in paragraph 7 of Article 76 of the Tax Code of the Russian Federation.

The organization will not be able to open a new account (deposit, deposit) during the blocking period. And not only in the servicing, but also in any other bank. The exception is special electoral accounts and special accounts of referendum funds. This procedure is established by Article 76 of the Tax Code of the Russian Federation.1

Currently tax office is developing a special Internet service through which banks will be able to quickly receive information about organizations whose accounts are blocked by tax inspectorates. Information about the cancellation of the blocking will be posted on the same resource. This is stated in the letter of the Federal Tax Service of Russia dated January 22, 2014 No. ED-4-2 / 738.

Application for cancellation of blocking

If the inspection blocked several accounts of the organization at once, and only some of them are sufficient to cover the debt to the budget, the organization has the right to submit an application to the inspection to cancel the blocking. But only in relation to those accounts on which there are funds in excess of the amount necessary to pay off the debt. For example, if the inspection has blocked three accounts of the organization, and there are enough balances on two of them to cover the debt, the organization can apply to the inspection with a written application to cancel the blocking of the third account.

within two working days from the date of receipt from the bank of information about the balance of funds on the blocked accounts of the organization (if the organization did not attach supporting documents to the application) (paragraph 4, clause 9, article 76, clause 6, article 6.1 of the Tax Code of the Russian Federation).

The decision to suspend operations in relation to all other accounts is canceled:

not later than one working day following the day of submission by the organization tax return, - if the account was blocked due to the organization's late submission of a tax return (subclause 1, clause 3.1, article 76, Tax Code of the Russian Federation);

no later than one working day following the day the taxpayer fulfills the obligation to ensure reception at the location of the organization (at the place of registration of the organization as largest taxpayer) documents in electronic form according to the TMS (subclause 2, clause 3.1, article 76, clause 6, article 6.1 of the Tax Code of the Russian Federation);

not later than one business day following the day of transfer of the electronic receipt for acceptance of requirements and notifications or the day of submission of the documents themselves, explanations, appearance at the inspection (subclause 2, clause 3.1, article 76, clause 6, article 6.1 of the Tax Code of the Russian Federation). To unblock accounts, send an application to the inspection;

not later than one business day following the day the tax inspectorate received documents (copies thereof) confirming the collection of tax (penalties, fines) - if the account was blocked due to the organization's failure to comply with the tax inspectorate's requirement to pay tax (penalties, fines) (p 8 article 76, paragraph 6 article 6.1 of the Tax Code of the Russian Federation);

on the day of the decision to cancel (replace) interim measures, if the account was blocked so that the organization could not hide the property from enforcement to pay off debts identified as a result of tax audit(paragraph 2, clause 10, article 101 of the Tax Code of the Russian Federation).

The basis for unblocking an account may be other conditions that are not named in the Tax Code of the Russian Federation. Such conditions may be established by separate federal laws. For example, all restrictions on the disposal of property (including cash) are automatically removed if, as part of the bankruptcy procedure, an observation procedure is introduced or bankruptcy proceedings are opened (paragraph 1 of article 63, paragraph 1 of article 126 of the Law of October 26, 2002 city No. 127-FZ). If the cancellation of the suspension of operations on the accounts of the organization is carried out on such additional grounds, the decision of the inspection to cancel the blocking is not required. This is stated in Article 76 of the Tax Code of the Russian Federation.

Tax Code of the Russian Federation

"Tax audit", 2008, N 3

One of the ways to ensure the fulfillment of the organization's obligation to pay taxes, fees, penalties, fines, as well as the timely submission of a tax return, is to block its bank accounts by the tax authorities.

The article discusses the procedure for blocking accounts: which accounts can be blocked, what debit transactions the organization has the right to carry out on blocked accounts, ways to cancel the decision to suspend operations on accounts, and also how, if the tax authorities cancel such a decision, the organization can bring it to the bank .

Blocking organization accounts

When an organization fails to fulfill the obligations imposed on it by the Tax Code, the tax authority may suspend its operations on bank accounts. Article 76 of the Tax Code of the Russian Federation provides for two cases in which it is possible to block accounts:

- extrajudicial collection of tax, dues, penalties, fines, if the taxpayer has not complied with the tax authority's demand for their payment (clause 1);

- non-submission by the taxpayer of the tax declaration to the tax authority within 10 days after the deadline for its submission (clause 3).

Decision to suspend operations on taxpayer's bank accounts<1>receives the head (deputy head) of the tax authority and sends it to the bank for hard copy or in electronic form. The date and time of receipt by the bank of the decision of the tax authority to suspend operations on the organization's bank accounts are indicated in the notice of delivery or in the receipt of receipt of the decision.

<1>The form was approved by the Order of the Federal Tax Service of Russia dated 01.12.2006 N SAE-3-19 / [email protected]The decision to suspend the organization's operations on bank accounts is subject to unconditional execution by the bank. That is, the latter must block the accounts of the organization, regardless of the fact that, in the opinion of the organization, this decision was made on the basis of erroneous conclusions. Also, the taxpayer needs to take into account that, in accordance with paragraph 10 of Art. 76 of the Tax Code of the Russian Federation, the bank is not liable for losses incurred by the taxpayer as a result of the suspension of operations by decision of the tax authority.

Suspension of operations on bank accounts means the termination by the bank of all debit operations on the accounts of the organization, subject to certain restrictions, while the bank carries out profitable operations in full (receipt of funds to the accounts of the organization).

If the suspension of operations is associated with the collection of payments to the budget, then the termination of debit operations on accounts is valid within the amount specified in the decision. The Letter of the Ministry of Finance of Russia dated June 21, 2007 N 03-02-07 / 1-304 clarifies that the organization has the right to use the funds on its bank accounts in excess of the amount specified in the decision of the tax authority to suspend operations on its accounts , at your discretion. In practice, the tax authorities usually suspend transactions on all accounts of the taxpayer, not taking into account this limitation.

Failure to file a tax return. Since in Art. 76 of the Tax Code of the Russian Federation refers to the blocking of accounts in case of failure to submit only a tax return, the financiers in Letter N 03-02-07 / 1-324 dated 12.07.2007 explained that this measure does not apply if the organization fails to submit settlements for advance payments, financial statements and other documents serving as the basis for the calculation and payment of taxes. FAS MO in the Decree of 12.03.2008 N KA-A40 / 1246-08 indicated: from the provisions of Art. 76 of the Tax Code of the Russian Federation, it does not follow that the tax authority has the right to suspend operations on bank accounts with an organization that is a tax agent in the event of failure to provide information on foreign income individuals according to the form 2-NDFL.

It is very important for the taxpayer to determine in which cases it can be said that they did not fulfill the obligation to submit a tax return in a timely manner. Let's consider some situations.

In paragraph 1 of Art. 80 of the Tax Code of the Russian Federation states that a tax return is submitted by each taxpayer for each tax payable, unless otherwise provided by the legislation on taxes and fees. Accordingly, a taxpayer is not required to file tax returns for those taxes for which he is not a payer. In accordance with this Letter of the Federal Tax Service for Moscow dated 09.06.2007 N 16-10 / [email protected] clarified that for non-submission of tax returns, the tax authorities have the right to decide to suspend operations on the accounts of the organization only if it is obliged to submit them.

For the case when the amount of tax on the tax return is zero, the Tax Code does not provide for the possibility of not submitting a "zero" declaration. The need to submit such a declaration was indicated by the Presidium of the Supreme Arbitration Court of the Russian Federation in paragraph 7 of the Information Letter dated March 17, 2003 N 71: by virtue of Art. 80 of the Tax Code of the Russian Federation, the duty of a taxpayer to submit a tax return for a particular type of tax is due not to the presence of the amount of such tax payable, but to the provisions of the law on this type of tax, by which the relevant person is classified as a payer of this tax. This position was guided by the Ministry of Finance in the Letter dated 16.01.2008 N 03-02-07 / 1-14.

It is not uncommon for a tax authority to refuse to accept a tax return submitted under the old form. If the organization did not have time to re-submit this declaration in the current form before the expiration of 10 days after the deadline for its submission, the tax authorities may block its accounts.

The taxpayer can challenge the actions of the tax authorities in court. For example, in the Resolutions of the FAS VVO dated February 22, 2007 N A82-4019 / 2006-99, the FAS SZO dated February 26, 2007 N A56-16164 / 2006 states that the basis for making a decision to suspend the taxpayer's operations on his bank accounts is the failure to submit or untimely submission by the taxpayer of the tax declaration to the tax authority. The Code does not provide for the possibility of suspending transactions on a taxpayer's accounts for non-compliance with the form of a tax return. At the same time, in order to avoid disputes with the tax inspectorate, we recommend that taxpayers check whether the form is valid before filling out a tax return.

The organization may delegate authority to maintain tax accounting and reporting to its representative, such as a specialized company. If an authorized representative has not timely filed a tax return with the tax authority, then liability for this violation, in accordance with Art. 76 of the Tax Code of the Russian Federation, will be borne by the taxpayer organization. This conclusion follows from paragraph 7 of the Decree of the Plenum of the Supreme Arbitration Court of the Russian Federation dated February 28, 2001 N 5, according to which the subject of the tax legal relationship is the taxpayer himself, regardless of whether he personally participates in this legal relationship or through a legal or authorized representative.

For the case of suspension of operations on accounts related to the failure to submit a tax return, the Tax Code of the Russian Federation did not establish a limit on the balance of funds on accounts, which is subject to the decision to suspend operations. Therefore, the tax authorities block all funds on bank accounts.

If operations on the accounts of the organization are suspended and the funds on them are not enough to cover the debt to the budget, then the organization, in order to continue its economic activity can open an account with another bank. In this case, after notifying counterparties of the opening of a new account, short term will be able to use the funds at their discretion. In doing so, she will need to consider the following:

- she is obliged to report the opening of an account to the tax authority within 7 days from the date of its opening;

- the bank is obliged to inform the tax authority about opening an account within 5 days from the date of its opening.

Accordingly, the tax authority, having learned about the opening of a new account, will also block it, but until that moment the organization will be able to use the funds received.

Debit transactions carried out during the period of blocking accounts. The decision to suspend operations on bank accounts does not apply to:

- for operations to write off funds to pay taxes, advance payments, fees, penalties, fines transferred to the budget system of the Russian Federation;

- for payments, the sequence of execution of which precedes the fulfillment of the obligation to pay taxes, fees, penalties, fines. Since, according to Art. 855 "Priority of debiting funds from the account" of the Civil Code of the Russian Federation, settlements on mandatory payments to the budget are made in the order of the fourth priority, then during the period of suspension of operations on the account, funds can be debited from it:

- first of all - according to executive documents providing for the transfer or issuance of funds from an account to satisfy claims for compensation for harm caused to life and health, for the recovery of alimony;

- in the second place - according to executive documents providing for the transfer or issuance of funds for settlements on the payment of severance benefits and wages with persons working under an employment contract (contract), for the payment of remuneration to the authors of the results of intellectual activity;

- in the third place - for deductions to the Pension Fund, the Social Insurance Fund and the Compulsory Medical Insurance Fund (paragraph 4, clause 2, article 855 of the Civil Code of the Russian Federation). Also, in the third queue of the Civil Code of the Russian Federation, payments are indicated that are excluded from this queue by the Decree of the Constitutional Court of the Russian Federation dated December 23, 1997 N 21-P - this is a write-off according to payment documents providing for the transfer or issuance of funds for settlements on wages with persons working on a labor basis. agreement (contract).

Since the relevant amendments to the Civil Code of the Russian Federation have not yet been adopted, this issue is annually regulated by the federal law on federal budget for the respective year. According to Art. 5 of the Federal Law of July 24, 2007 N 198-FZ "On the federal budget for 2008 and for the planning period of 2009 and 2010" before amending paragraph 2 of Art. 855 of the Civil Code of the Russian Federation, in accordance with the Decree of the Constitutional Court of the Russian Federation N 21-P, if the funds in the taxpayer's account are insufficient to satisfy all the requirements presented to him, the debiting of funds under settlement documents providing for payments to the budgets of the budget system of the Russian Federation, as well as the transfer or issuance of funds for payroll settlements with persons working under an employment contract are made in the order of the calendar order of receipt of the specified documents after the transfer of payments made in accordance with the specified article of the Civil Code of the Russian Federation in the first and second turn. Thus, the organization will not be able to withdraw funds from the account for the payment of employees if it is blocked.

According to paragraph 2 of Art. 855 of the Civil Code of the Russian Federation, funds are debited from the account for claims relating to one queue, made in the order of the calendar order of receipt of documents. Based on this, in the Letter of the Ministry of Finance of Russia dated April 12, 2007 N 03-02-07 / 1-172, it is explained that the bank, in the presence of a decision of the tax authority to suspend operations on the taxpayer's account, executes the taxpayer's order to write off funds for paying the state fee from his account and enrolling them in the budget system in the order of calendar priority of receipt of documents belonging to the same group. State duty, in accordance with paragraph 10 of Art. 13 and paragraph 1 of Art. 333.16 of the Tax Code of the Russian Federation, referred to federal fees, therefore, its payment and payment of debts to the budget for taxes, fees, penalties, fines on a collection order is carried out in the fourth order, taking into account the calendar order of receipt of documents.

Account concept. When applying Art. 76 of the Tax Code of the Russian Federation, it is important to determine what is meant by an account. The fact is that the suspension of operations affects only those accounts of the organization opened with the bank, which are recognized as such for the purposes of the Tax Code. You also need to take into account that if there is a decision to suspend operations on bank accounts, he is not entitled to open new accounts for the organization. These restrictions apply to all bank accounts of the organization. According to paragraph 2 of Art. 11 of the Tax Code of the Russian Federation, settlement (current) and other accounts in banks opened on the basis of an agreement are recognized as accounts bank account, to which funds of organizations are credited and from which funds can be spent. Thus, there are three requirements for the concept of "account" used in the Tax Code of the Russian Federation:

- availability of a bank account agreement on the basis of which a bank account is opened;

- the possibility of crediting funds to the account;

- the possibility of spending money from the account.

The legal regulation of the bank account agreement is devoted to Ch. 45 of the Civil Code of the Russian Federation. In Art. 845 of the Civil Code of the Russian Federation it is said that under a bank account agreement, the bank undertakes to accept and credit incoming to the account, open to the client(to the account holder), funds, execute the client's instructions on transferring and issuing the relevant amounts from the account and carrying out other operations on the account. Taxpayers open many different accounts in banks, not all of them can be unambiguously said whether they are recognized as accounts in accordance with Art. 11 of the Tax Code of the Russian Federation and whether they will be affected in the event of blocking.

In the Letter of the Ministry of Finance of Russia dated November 21, 2007 N 03-02-07 / 1-497, it is explained that, for example, deposit and loan accounts do not have the characteristics of accounts, are not opened on the basis of a bank account agreement and have a special special purpose, therefore, the bank has the right to open these accounts for the organization if there is a decision to suspend operations on accounts. The Letter of the Ministry of Finance of Russia dated April 27, 2007 N 03-02-07 / 1-208 states that accounts with funds belonging to third parties, for example, targeted financing, do not have the features of an account defined in Art. 11 of the Tax Code of the Russian Federation.

From the Letter of the Ministry of Finance of Russia dated May 11, 2007 N 03-02-07 / 1-225, it follows that if, by decision of the tax authority, operations on the taxpayer's bank account are suspended if there is a balance of funds on it, then the bank is not entitled to close this account, since termination of a bank account agreement if there is a balance of funds on it is associated with the conduct of debit transactions on this account. A similar position was expressed in Letter No. 11-14/16108 of 11.03.2004 of the UMNS for Moscow, which clarified that in the absence of funds on the client's account, the bank, at the request of the client, has the right to close the specified account, since the termination of the bank account agreement in this case will not entail debit transactions on the account.

Unblocking accounts

Suspension of operations on bank accounts is valid from the moment the bank receives the decision of the tax authority and until the moment it is canceled. If the suspension of operations on accounts is the right of the tax authority, then the cancellation of this suspension is its obligation, which it must fulfill within the time limits established by the Tax Code of the Russian Federation when the taxpayer fulfills certain requirements. The grounds for canceling the decision to suspend operations on accounts may be:

- the court's decision;

- the decision of the tax authority to cancel the suspension of operations on the taxpayer's bank accounts. It is accepted in cases where the organization submits a tax declaration, collects the amount of tax indicated in the decision to suspend operations on accounts. In these cases, the suspension of operations on accounts is canceled by the tax authorities no later than one business day following the day the organization submits a tax return or documents (copies thereof) confirming the payment of tax, dues, penalties, fines (clause 3, article 76 of the Tax Code of the Russian Federation). In practice, if an organization has made these payments to the budget, the tax authority will make a decision to cancel the suspension of operations on accounts only after it checks the receipt of funds to the corresponding account of the UFK.

The procedure for canceling the decision to suspend operations on accounts

The basis for the cancellation of the decision to suspend operations on accounts is the decision of the tax authority or the court. The decision of the tax authority to cancel the suspension of operations on accounts is sent to the bank in paper form or via telecommunication channels. The procedure for sending this decision to the bank in in electronic format established by the Central Bank of the Russian Federation. At present, this procedure has not been approved by the Central Bank of the Russian Federation, and the Procedure for sending to banks a decision to suspend operations on taxpayer accounts and a decision to cancel the suspension of operations in electronic form via telecommunication channels, approved by Order of the Federal Tax Service of Russia dated 03.11.2004 N SAE-3-24 / [email protected], is not applicable, since it is not approved by the Central Bank of the Russian Federation.

According to clause 2 of the Procedure for sending to the bank the decision of the tax authority to suspend operations on the accounts of the taxpayer (payer of fees) or the tax agent in the bank and the decision to cancel the suspension of operations on the accounts of the taxpayer (payer of fees) or the tax agent in the bank on paper<2>(hereinafter referred to as the Procedure for sending a decision on paper to the bank) the decision to cancel the suspension of operations on the taxpayer's accounts is sent by the tax authority to the bank by registered mail with a return receipt or is handed by the tax authority against receipt to the representative of the bank. The moment of receipt by the bank of the decision of the tax authority is the date and time indicated:

- in the notice of delivery, if it is sent to the bank by registered mail;

- in the note on the adoption of the decision, if it is handed over against receipt to the representative of the bank.

Changing the location of an organization. A situation is possible when an organization, during the period of validity of the decision to suspend operations on accounts, has changed its location and entered tax records at a new location. The Letter of the Ministry of Finance of Russia dated December 14, 2007 N 03-02-07 / 1-484 states that the decision to cancel the suspension of such operations is taken by the tax authority at the new place of registration of the taxpayer. In practice, this situation causes a lot of problems for the organization.

Judicial procedure for the cancellation of the decision to suspend operations. The tax code does not regulate the procedure judicial cancellation such a decision. The financiers in the Letter of December 14, 2007 N 03-02-07 / 1-484 indicated that, in accordance with paragraph 1 of Art. 16 of the Arbitration Procedure Code of the Russian Federation, the judicial acts of the arbitration court that have entered into legal force are binding on the bodies state power, local government, other bodies, organizations, officials and citizens and are subject to execution throughout the territory of the Russian Federation. Consequently, from the moment the court decision comes into force, the decision to suspend operations is cancelled.

Since this procedure for canceling a decision is not prescribed by law, and there are no official explanations from fiscal departments, it is possible that the taxpayer will need to submit a court decision both to the bank and to the tax authority.

Can the organization expedite communication to the bank of the decision to lift the suspension of operations?

Before the decision of the tax authorities to cancel the suspension of operations on accounts goes to the bank, time will pass, which is precious for the organization, because it cannot make payments. Therefore, it is very important for her that the decision reaches the bank as soon as possible. In this regard, questions often arise about the possibility of an organization submitting to the bank a copy of the decision on paper, which was issued to it by the tax authority, or submitting the original decision to the bank when the organization acts on the basis of the bank's power of attorney. According to financiers, not all of these cases are effective.

A copy of the decision to unblock accounts. The Letters of the Ministry of Finance of Russia dated May 31, 2007 N 03-02-07 / 1-266 and dated March 30, 2007 N 03-02-07 / 1-150 say that a copy of the decision to cancel the suspension of operations on the organization's bank accounts received by the bank from the client on paper, is not a basis for the bank to cancel the decision of the tax authority to suspend operations on the accounts of the organization. The effect of the decision of the tax authority to suspend operations on the organization's bank accounts is preserved until the bank receives the original decision to cancel the suspension of operations on the organization's bank accounts.

The conclusion of the financiers is based on the following: from Art. 76 of the Tax Code of the Russian Federation and the Procedure for sending a decision on paper to the bank, it follows that the tax authorities send the original decision to cancel the suspension of operations to the bank on paper, but there is no mention of the possibility of sending a copy. Therefore, it does not make sense for an organization to send a copy of the decision received from the tax authorities to the bank.

Power of attorney. The Tax Code provides for the possibility of participation of a person in tax legal relations through a legal or authorized representative. As a result, the question arises as to whether the organization, acting as an authorized representative of the bank, has the right to obtain from the tax inspectorate a decision to cancel the suspension of operations on paper and transfer it to the bank.

The Letter of the Ministry of Finance of Russia dated January 16, 2008 N 03-02-07 / 1-16 states that since the Tax Code of the Russian Federation and the Procedure for sending a decision to the bank on paper provide for the transfer by the tax authority of the decision to cancel the suspension of operations on the organization's accounts to the bank by handing it representative of the bank, such a decision, if there is an appropriate power of attorney, can be handed over to the organization (its representative), operations on bank accounts of which were suspended.

Thus, the organization can use this method to speed up the unblocking of accounts.

V.V. Nikitin

Magazine editor

"Acts and comments

The material was provided by the corporate publication for the clients of the IRBiS Group of Companies "Sistema success"

Surely, most of us are familiar with such an unpleasant and very problematic phenomenon for any business entity as a “blocking” of a current account by a tax authority. You can’t withdraw money for your own needs, you won’t be able to pay for the services of the supplier either, the organization’s activities seem to be paralyzed. How should a taxpayer behave in such a difficult but often occurring situation? How to prevent its occurrence? What effective ways can I "unblock" the organization's accounts? You can find answers to these and many other questions in this article.

1. General provisions on the suspension of operations on bank accounts

We all know very well that in order to ensure the activities of the state, the Constitution of the Russian Federation establishes the obligation to pay legally in a timely manner. established taxes and fees (Article 57 of the Constitution of the Russian Federation). In turn, in order to ensure the fulfillment of the obligation to pay taxes, the legislator established measures of state coercion, which are designed to ensure that the taxpayer fulfills his constitutional obligation.In the Tax Code, the constitutional obligation to pay legally established taxes and fees is detailed: in accordance with paragraphs. 1 p. 1 art. 23 of the Tax Code of the Russian Federation, taxpayers are required to pay legally established taxes, and in accordance with paragraph 4 of the same article, submit tax declarations (calculations) to the tax authority at the place of registration in the prescribed manner.

In case of non-fulfillment or improper fulfillment of the duties assigned to the taxpayer, the tax authority may hold him accountable, as well as use mechanisms for forcing him to fulfill the obligations established by the Tax Code.

Chapter 11 of the Tax Code of the Russian Federation is devoted to ensuring the fulfillment of the duties of taxpayers. So, in accordance with paragraph 1 of Art. 72 of the Tax Code of the Russian Federation, the fulfillment of the obligation to pay taxes and fees can be ensured in the following ways:

- pledge of property,

- guarantee,

- penalty,

- seizure of property of the taxpayer,

- suspension of operations on bank accounts.

Moreover, the situation becomes very depressing when the account is “blocked” completely unexpectedly, at the most inopportune moment, for example, when the taxpayer urgently needs money to conclude a profitable and important contract.

Due to the fact that the suspension of operations on accounts for the taxpayer is sad news, in order to better understand this process, as well as in order to be able to challenge the actions of the tax authority, it is necessary to consider in more detail the procedure for suspending operations on accounts, which is commonly referred to as “blocking accounts”, “account freeze” or “account arrest”.

2. Procedure for suspension of operations on accounts

The procedure and terms for the suspension of operations on taxpayer accounts in banks are regulated by Art. 76 of the Tax Code of the Russian Federation.In order to suspend operations on the taxpayer's accounts, the tax authority, represented by the head or his deputy, makes a decision to suspend operations and sends it to the banks where the taxpayer has current accounts, and a copy of this decision must be in without fail transferred to the taxpayer against signature or in any other way indicating the date of its receipt. The transfer of the decision to the bank is carried out on paper or in electronic form (clause 4 of article 76 of the Tax Code of the Russian Federation).

Having received the decision of the tax authority to suspend operations on accounts, the bank is obliged to execute it unconditionally and suspend operations on the taxpayer's accounts from the moment the decision is received (clause 7, article 76 of the Tax Code of the Russian Federation).

In addition, after receiving a decision to suspend operations on accounts, the bank is obliged to report to the tax inspectorate information on the balance of funds on the taxpayer's accounts (clause 5, article 76 of the Tax Code of the Russian Federation).

The bank will be able to “unblock” frozen accounts only after the tax authority cancels the decision to suspend operations on accounts, because the Tax Code of the Russian Federation establishes a clear period of validity of the decision (from the moment the bank receives it from the tax authority and until it is canceled) and does not provide for options for suspending its validity (p. .7 article 76 of the Tax Code of the Russian Federation).

Note! If the taxpayer has funds on several current accounts in the aggregate sufficient to pay off the arrears, fines, penalties specified in the decision to suspend operations on the account, then the taxpayer has the right to file with the tax authority an application to cancel the suspension of operations on bank accounts, indicating the accounts, on which there are sufficient funds to enforce the decision to collect the tax. (clause 9, article 76 of the Tax Code of the Russian Federation).

The application must be accompanied by Bank statements confirming the availability of funds in the accounts. Having received the appropriate package of documents, the tax authority, within two days from the date of receipt of the application, is obliged to decide on the cancellation of the suspension of operations on individual accounts of the taxpayer.

If the package of documents is insufficient to confirm information about the bank account proposed by the taxpayer, then the inspection may take some time to verify this information. After receiving information from the bank that there are enough funds in the accounts indicated by the taxpayer, two days are allotted for the decision to “unblock” (clause 9, article 76 of the Tax Code of the Russian Federation).

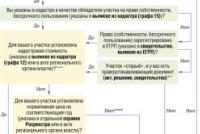

3. Reasons why the tax authorities “block” accounts

Tax legislation provides for three grounds for blocking an account:The declaration has not been submitted;

The tax has not been paid;

Ensuring the execution of the decision of the tax authority based on the results of the audit.

Let's take a closer look at each of them.

3.1. Declaration not submitted

If the taxpayer has not submitted a tax return within 10 working days after the expiration of due date its submission, the tax authority may decide to suspend operations on accounts (paragraph 1, clause 3, article 76 of the Tax Code of the Russian Federation).

In this case, the tax authority is obliged to cancel the suspension the next day, after the taxpayer submits the relevant declaration (paragraph 2, clause 3, article 76 of the Tax Code of the Russian Federation).

In practice, there are cases when accounts are “blocked” by the tax authority, and the taxpayer is not required to submit a declaration.

As the court rightly pointed out cm.Decisions of the Federal Antimonopoly Service of the North Caucasian District dated July 12, 2006 in case N F08-3078 / 2006-1320A, FAS of the Moscow District dated December 2, 2004 in case N KA-A40 / 11311-04), Art. 23 of the Tax Code of the Russian Federation imposes on the taxpayer the obligation to submit to the tax authority at the place of tax registration in the prescribed manner tax returns for those taxes that he is obliged to pay, if such an obligation is provided for by legislation on taxes and fees.

Moreover, Article 80 of the Tax Code of the Russian Federation corresponds to this obligation, according to which a tax return is submitted by a taxpayer for each tax payable by this taxpayer. Thus, if the taxpayer has no obligation to pay tax, then the tax authority has no grounds to suspend the taxpayer's operations on his bank accounts.

In addition, according to judicial practice(cm. Decree of the Federal Antimonopoly Service of the North Caucasus District dated July 30, 2009 in case N A32-22251 / 2008-12 / 190; Decree of the FAS of the East Siberian District of December 21, 2005 N A33-12414 / 05-Ф02-6442 / 05-С1) it is unlawful to suspend operations on bank accounts if the deadline for submitting a declaration is missed as a result of an unreasonable refusal of the tax authority to accept the declaration due to its incorrect completion.

Thus, individual violations in the preparation of declarations (for example, errors in the preparation title page, indicating an erroneous tax period) cannot serve as a basis for suspending transactions on the taxpayer's accounts or for imposing a fine under Art. 119 of the Tax Code of the Russian Federation for failure to submit a declaration.

3.2. Tax not paid

In accordance with paragraph 1 of Art. 46 of the Tax Code of the Russian Federation, in the event of non-payment or incomplete payment of tax within the prescribed period, the obligation to pay tax is enforced by foreclosing the taxpayer's funds in bank accounts.

In this case, the collection of tax debt at the expense of the taxpayer's funds is carried out as a result of the adoption by the tax authority of an appropriate decision on collection and by sending collection orders to the bank to write off the debt (clause 2, article 46 of the Tax Code of the Russian Federation).

Based on clause 7 of article 46 of the Tax Code of the Russian Federation, the tax authority at the stage of collecting debts from the taxpayer by foreclosing his funds has the right to suspend operations on all his bank accounts in the manner prescribed by article 76 of the Tax Code of the Russian Federation.

Thus, in order to ensure the execution of a decision on the collection of a tax or fee at the expense of funds held in the taxpayer's bank accounts, the tax authority is also entitled to suspend operations on the accounts of the taxpayer - organization in accordance with Art. 76 of the Tax Code of the Russian Federation.

The procedure for the undisputed collection of tax debts is complex and multi-stage, and therefore, at the stage of its implementation, the tax authority often commits procedural violations that can serve as a basis for canceling the decision to collect debts at the expense of the taxpayer's funds and, as a result, the decision to suspend operations on bank accounts.

The most common violations are violation of the deadlines for submitting a claim for tax payment, violation of the procedure or method for submitting a claim, on the basis of which a decision is already made to collect debts at the expense of funds and bank accounts are “blocked”.

AT Decree of May 4, 2005NКА-А40/3677-05, Federal Antimonopoly Service of the Moscow District pointed out that the tax authority violated the norms of Art. Art. 69, 76 of the Tax Code of the Russian Federation, since the demand for payment of tax was handed over to the taxpayer after the expiration of the payment period, in connection with which it was not possible for the taxpayer to fulfill it within the prescribed period. Moreover, the taxpayer was collecting a debt, the terms for collection of which, taking into account the provisions of Article 70 of the Tax Code of the Russian Federation, were missed by the tax authority.

Sending a claim for the payment of tax is not only a non-normative legal act, but also the initial stage of the process of forced collection of taxes (Articles 46, 47 of the Tax Code of the Russian Federation). Non-compliance by the tax authority with the procedure established by law for sending a claim to a taxpayer significantly violates the taxpayer's constitutional guarantees for the protection of rights and freedoms.

In addition, you should pay attention to what type of correspondence (regular or registered mail) documents are sent to you from the tax office.

As the Federal Antimonopoly Service of the Urals District pointed out in its Decree of July 12, 2010 N F09-5181 / 10-C3, sending a taxpayer a demand for payment of tax (penalty, fine) in violation of the provisions of paragraph 6 of Art. 69 of the Tax Code of the Russian Federation (that is, not by registered mail) is assessed by the court as a significant violation of the procedure for the forced undisputed collection of taxes, penalties and fines and is an independent and unconditional basis for canceling decisions to collect debts at the expense of cash and decisions to suspend operations on accounts.

3.3. Interim measure for the execution of the decision based on the results of the audit

There is one more reason when the taxpayer's current account can be blocked. Thus, the suspension of operations on accounts can be used by the tax authorities as a security measure for the execution of decisions on inspections (desk or field audits), during which taxes, penalties, and fines were assessed for payment.

In accordance with paragraph 7 of Art. 101 of the Tax Code of the Russian Federation, based on the results of consideration of the tax audit materials, the head (deputy head) of the tax authority makes a decision on holding liable for committing tax offense or denial of liability.

After the decision is made, the head (deputy head) of the tax authority has the right to take measures aimed at ensuring the possibility of executing the said decision (clause 10, article 101 of the Tax Code of the Russian Federation).

However, please note that the tax authority has the right to take interim measures in pursuance of the audit decision only if it has sufficient grounds to believe that failure to take these measures may make it difficult or impossible in the future to enforce such a decision and (or) recover arrears, penalties and fines specified in the decision. In practice, such grounds may be: the presence of debt on personal account of the taxpayer, repeated failure to fulfill tax obligations, reduction of the organization's assets, a set of circumstances indicating that the taxpayer has received unjustified tax benefits (see, for example, the Decree of the Federal Antimonopoly Service of the Volga District of September 16, 2010 in case N A12-1588 / 2010).

In order to take interim measures, the head (deputy head) of the tax authority issues an appropriate decision, which enters into force from the date of its signing and is valid until the day of execution of the decision to hold liable for committing a tax offense or the decision to refuse to hold liable for committing a tax offense, or until the date of cancellation of the decision by a higher tax authority or court.

Note! Suspension of operations on bank accounts in the procedure for taking interim measures may be applied only after imposing a ban on the alienation (mortgage) of property and if total cost such property according to accounting less than the total amount of arrears, penalties and fines payable on the basis of the decision.

So, to summarize: the Tax Code of the Russian Federation provides for three grounds for suspending operations on accounts:

a) non-payment of taxes, fees, penalties and fines;

b) a tax return not submitted on time;

c) to ensure the execution of a decision on bringing (refusal to bring) to tax liability.

However, in practice, tax officials often abuse the right granted to them and use the suspension of transactions on taxpayers' accounts as a method of psychological influence. In this connection, the following information will be useful to every accountant and manager!

4.IMPORTANT TO KNOW!

4.1. The tax authority does not have the right to "block" the account if the financial statements are not submitted, the advance calculation is not submitted, or the requested verification documents are not submitted.The tax authority does not have the right to "block" the current account if the taxpayer has not submitted financial statements or other documents related to the calculation and payment of taxes and other obligatory payments to the budget , in view of the fact that Article 76 of the Tax Code of the Russian Federation does not contain such a basis for suspending operations on accounts. This position is confirmed judicial practice (see Decree of the Federal Antimonopoly Service of the Moscow District dated October 05, 2007 N KA-A40 / 9465-07) and opinion Ministry of Finance of Russia in a letter dated July 12, 2007 N 03-02-07 / 1-324.

In addition, the courts will recognize it as illegal to “block” an account if the statistical reporting (see Resolution of the Federal Arbitration Court of the Moscow District dated January 29, 2009. N KA-A40 / 13357-08), information on the income of individuals in the form 2-NDFL is not provided ( see Decree of the Federal Arbitration Court of the Moscow District dated February 14, 2008 N KA-A40 / 235-08), the advance tax calculation has not been submitted (decision of the Arbitration Court of Moscow dated February 26, 2008 in case N A40-1160 / 08-75-5). The courts, recognizing the actions of the tax authorities in such situations as illegal, refer to the fact that the suspension of operations on accounts, in accordance with the provisions of paragraph 3 of Article 76 of the Tax Code of the Russian Federation, can be applied only in cases of failure to file a tax return, this provision of the law is not subject to broad interpretation .

Also, the taxpayer’s failure to submit documents requested by the tax authority during a desk or field tax audit cannot be a basis for suspending account transactions. (see Resolution of the Federal Antimonopoly Service of the West Siberian District of March 28, 2005NF04-1592/2005(9795-A46-35); Decree of the Federal Antimonopoly Service of the West Siberian District of 07.11.2005NF04-760/2005(16440-A46-40)). At the same time, the courts proceed from the fact that, in accordance with Article 76 of the Tax Code of the Russian Federation, the suspension of operations on a bank account is one of the ways to ensure the fulfillment of the obligation to pay taxes, but not the way to ensure the fulfillment of the requirements of the tax authorities in the exercise of their control functions.

4.2. Even if the account is blocked, you can use it!

In accordance with paragraph 3, clause 1, article 76 of the Tax Code of the Russian Federation, “freezing” an account by a tax authority does not mean the termination of all debit transactions. The sequence of debiting funds from a bank account is carried out in the manner prescribed by Art. 855 of the Civil Code of the Russian Federation.

If there are funds on the account, the amount of which is sufficient to satisfy all the requirements presented to the account, these funds are debited in the order in which the taxpayer's payment documents are received, the so-called calendar sequence.

The suspension of operations does not apply to payments, the priority of which precedes the fulfillment of the obligation to pay taxes and fees.

Thus, funds can be credited to the blocked account of the taxpayer, but they are spent only in the order of priority specified in Article 855 of the Civil Code of the Russian Federation:

First of all, write-offs are carried out according to executive documents providing for the transfer or issuance of funds from the account to satisfy claims for compensation for harm caused to life and health, as well as claims for the recovery of alimony;

Secondly, write-offs are made under executive documents that provide for the transfer or issuance of funds for settlements on the payment of severance benefits and wages with persons working under an employment contract, including under a contract, for the payment of remuneration to authors of the results of intellectual activity;

In the third place, write-offs are made according to payment documents that provide for the transfer or issuance of funds for settlements on wages with persons working under an employment agreement (contract), as well as for deductions to Pension Fund Russian Federation, Fund social insurance Russian Federation and compulsory medical insurance funds;

Taking into account the Decree of the Constitutional Court of the Russian Federation N21-P of December 23, 1997, taxes and fees should be collected in the third place.

In addition, debiting funds from the account for claims related to one queue is made in the order of the calendar order of receipt of payment documents.

Thus, a taxpayer on a blocked account can make payments of the 1st and 2nd priority, as well as payments to the budget and off-budget fund s from the 3rd stage, determined by the legislation (Article 855 of the Civil Code of the Russian Federation with the features established by the Federal Law on the Federal Budget for the corresponding year).

4.3. Not only the tax office can block an account!

Our article is devoted to the procedure for suspending operations on a taxpayer's bank accounts, which is carried out by the tax authorities. However, similar rights to “freeze” settlement accounts are also granted to customs authorities when collecting debts on payment of customs duties and penalties (Article 34 of the Tax Code of the Russian Federation).

The procedure for suspending operations on accounts by customs authorities is established by Order of the Federal Customs Service of December 3, 2009 N 2184.

Similar powers to suspend operations on bank accounts are imputed by Art. 8 of the Federal Law of 07.08.2001 No. 115-FZ “On Counteracting the Legalization (Laundering) of Proceeds from Crime and the Financing of Terrorism” and Decree of the Government of the Russian Federation of 06.23.2004 No. 307 “On Approval of the Regulations on Federal Service on financial monitoring» Rosfinmonitoring.

In addition, we draw the attention of readers to the fact that if you do not pay insurance premiums on time or do not submit to statutory settlements on them, the accounts will not be blocked, since the legislator has not endowed extra-budgetary funds with the appropriate powers.

4.4. Not every decision to suspend operations on accounts must be enforced

Not the decision to suspend operations on accounts is subject to execution in the following cases:

- the decision was made by an unauthorized body;

The decision was made in relation to a bank account, which, in accordance with the definition of an account given in Art. 11 of the Tax Code of the Russian Federation does not fall under this concept.

Let us consider the last reason in more detail, since everything is simple with the first, since the decision was made by an unauthorized body, then the bank has no legal grounds for its execution.

So, in accordance with Art. 11 of the Tax Code of the Russian Federation, an account means settlement (current) and other accounts in banks opened on the basis of bank account agreements, to which funds are credited and from which funds can be spent by the account holders themselves.

Under this definition fall under: settlement, correspondent, current, current currency accounts, “ruble” accounts of type “K” (convertible) and “H” (non-convertible) of non-residents, accounts serviced using corporate bank cards.

However, the suspension of operations does not apply to taxpayer accounts opened on the basis of other agreements and transactions, for example: deposit, loan, letter of credit, currency transit and currency special transit accounts.

In addition, the suspension of operations on the accounts of bankrupt taxpayers is not lawful (paragraph 1 of article 126 of the Federal Law of October 26, 2002 N127-FZ “On Insolvency (Bankruptcy)”).

If the decision to suspend operations is made in an unestablished form, then it is also not subject to execution by the bank, the indicated follows from the meaning of clause 4 of article 76 of the Tax Code of the Russian Federation.

4.5. Blocked account - open a new one?

According to paragraph 12 of article 76 of the Tax Code of the Russian Federation, a bank is not entitled to open new settlement accounts for a taxpayer if there is a decision to suspend operations on accounts.

Confirmation of the above position Ministry of Finance of the Russian Federation set out in letter from12.12.2005 N03-02-07/1-336 , in which the financial department indicated that the closure of the taxpayer's account by the bank is not a basis for canceling the decision of the tax authority to suspend operations on the taxpayer's accounts, and, consequently, the bank opening new accounts for the taxpayer and executing the taxpayer's instructions on them to transfer funds to another person who is not related with the fulfillment of obligations to pay a tax or fee, or other payment order, which, in accordance with the legislation of the Russian Federation, has the priority of the order of execution over payments to the budget (off-budget fund), is a violation of Art. 76 of the Tax Code of the Russian Federation.

The courts also agree with the position of the Ministry of Finance of the Russian Federation, as in Decree of 23.09.2003 N A29-1832 / 2003 of the Federal Antimonopoly Service of the Volga-Vyatka district indicated that, according to paragraph 9 of Art. 76 of the Tax Code of the Russian Federation, if there is a decision to suspend operations on accounts, the bank is prohibited from opening any new accounts for the taxpayer indicated in the decision. AT Decree dated 26.01.2006NA42-4190/2005FAS Northwestern District came to the conclusion that the closure by a bank of an account of a taxpayer-organization, in respect of which a decision was made to suspend operations, does not terminate the legal consequences of such a decision of the tax authority in terms of a ban on opening new accounts for a taxpayer-organization in this bank.

Moreover, banks are unlikely to open a new account if there is a decision of the tax authority to suspend operations or to not comply with the decision of the tax authority, since this is fraught with consequences in the form of penalties for a credit institution. So, according to clause 1 of article 132 of the Tax Code of the Russian Federation, when opening an account by a bank that already has a decision on suspension, it entails a fine of 20 thousand rubles from it, in addition, administrative responsibility is also provided for the specified act for bank officials, according to Article 15.7 of the Code of Administrative Offenses of the Russian Federation in the amount of two to three thousand rubles. Article 134 of the Tax Code of the Russian Federation provides for sanctions for banks, in case they do not comply with the decisions of the tax authorities to suspend operations on the account, in the amount of 20 percent of the amount that will be transferred according to the taxpayer's payment order, but not more than the amount of the debt and not less than 10 thousand rubles . Administrative responsibility for this act entails a fine in the amount of two thousand to three thousand rubles (Article 15.9 of the Code of Administrative Offenses of the Russian Federation).