When can maternity capital be used for a mortgage. The procedure for repaying a mortgage with maternity capital (step by step instructions). Obtaining a new payment schedule or a certificate of loan repayment

Quite often among Russian citizens there is the question of how to pay off the mortgage with maternity capital, after all, the state has provided an excellent opportunity to direct it to the purchase of residential real estate in the property. Today, more and more Russian families want to take advantage of the benefit.

In this article, we will consider issues related to the intricacies of the procedure for making maternity capital to pay off a mortgage loan.

What is maternity capital and how it can be disposed of

First, let's deal with the concept of maternity capital. The essence of this concept is expressed in two components:

- As a way of state support for families with two or more children

- Maternal capital as a way to improve the demographic situation in Russia

Given that the state program sets itself the task of strengthening and improving the quality of life of families, the possible ways to use the amount of money allocated by the state are limited.

The use of maternity capital is possible in the following ways:

- own housing

- Transfer the amount to the Pension Fund in order to increase the mother's pension in the future

- Pay for the educational services of any child in the family

- Pay for services or purchase funds for the rehabilitation and adaptation in everyday life of children with disabilities

As you understand, the first method is most in demand. Thus, you can legally use maternity capital funds to purchase your own housing in two ways:

- By direct purchase of real estate

- Through a mortgage loan

If you opted for the second option, then the amount of maternity capital can be used to pay for an already issued housing loan (mortgage), or used as the amount of the down payment when concluding a transaction. You should know that you do not need to wait for the child to reach the age of 3, since you have the right to use maternity capital funds without any problems immediately after it is received.

We draw your attention to the fact that at the legislative level it is established that the funds of family capital can only be used by bank transfer - it is impossible to get cash in hand. The state made such a decision to control the intended use of the allocated amount of money. Therefore, if you plan to use maternity capital funds when purchasing or building your own real estate, you need to contact the Pension Fund of Russia and write a corresponding application.

Despite the strict rules established by law, there are exceptions. For example, if a family decides to build a house for housing according to its own project, then half of the maternity capital can be received to a current account opened with a bank even before construction begins. To receive the second part of the family capital, you should contact the Pension Fund (this is possible no earlier than the next six months from the moment the first part of the maternity capital is transferred) with a package of documents and an application. Documents must confirm the cost of the work performed. For example, these can be acts of work performed (building the walls of a building, pouring a foundation, installing a roof, etc.) contracts with contractors.

How to issue a certificate for the right to receive mother capital

If you decided to use maternity capital funds to pay off a mortgage loan or at your discretion, you will need to have a certificate on hand. In order to become the owner of the treasured paper, you need to visit the Pension Fund of Russia, and you can do this at any time after the corresponding right has come. That is, you have a child or you adopted him. What do you need to have with you?

You will need to collect the following package of documents:

- Passport of a citizen of the Russian Federation or a foreign citizen. There must be a mark on the registration of a citizen

- Child's birth certificate. If you are a citizen of a foreign state, then instead of a birth certificate of a baby, you can submit another document. For example, this may be a certificate that confirms that the child is a Russian citizen

Other documents - their list depends on the particular situation:

- The decision to adopt a child

- If your interests are realized through a representative, then you will need to have a power of attorney

- If the mother is deceased, a death certificate must be brought

- Court decision that the mother is declared dead

- Court decision depriving mother of parental rights

In addition, you will need to write an application for a certificate of maternity capital. After that, be patient and wait - within a month your application will be considered, and the Pension Fund will decide whether to issue a certificate or refuse to issue family capital.

What to do if the certificate is lost or damaged

Anything can happen in life, and the certificate was lost, destroyed or damaged. How to be in this case? You should visit the Pension Fund again, which will give you a duplicate. If the data of the certificate holder (name, passport details) have been changed, the applicant will also need to contact the Pension Fund.

It is important to know that the certificate does not have an expiration date. It can be used throughout the life of the mother or adopter. If a misfortune happened and the owner of the certificate died, then the second spouse, a child under the age of 23 or an adoptive parent has the right to use the capital.

How to pay a mortgage loan with maternity capital

If you already have the long-awaited certificate in your hands, you, as already mentioned above, get the legal right to use maternity capital to pay off a mortgage loan or making a down payment. So that during the procedure you do not have to deal with unforeseen situations, we suggest using the step-by-step instructions below:

1. The initial stage is to apply to the financial institution that issued you a mortgage or home loan in order to obtain a certificate of the interest rate on the loan and the balance of the principal amount. In addition, you may be given a contract for the sale of an apartment or a certificate of ownership (title documents) that you bought on bail. In most cases, financial institutions do not make life difficult for borrowers when obtaining such documents, but you cannot be 100% sure that there will be no difficulties.

2. Visiting the Pension Fund in order to write an application for the transfer of family (maternity) capital in payment of a mortgage loan. The form will be given to you by an employee of the Pension Fund and you will not need to pay for it. You need to have the necessary package of documents with you:

- Certificate for receiving maternity capital;

- Passport of a Russian citizen. If you are a citizen of a foreign state and you have been granted the right to receive maternity capital, then you need to bring a passport of a foreign citizen and documents confirming your place of residence;

- Documents that confirm the right to housing - a certificate of ownership of real estate, which was purchased using borrowed funds from a financial institution. In addition, you will need a personal account number and an extract from the house register;

- The application of the applied citizen that after the full repayment of the value of the property purchased for housing, he undertakes to formalize it with all family members (children, spouse) into common shared ownership. This paper must be certified by a notary;

- If there is also a co-borrower under the loan (mortgage agreement) (for example, it may be the second spouse), then you will need the following papers:

a) copies of his documents confirming citizenship

b) identity documents (passport)

c) paper that determines the place of residence

d) document confirming kinship - marriage certificate

- Documents evidencing that the borrower has debt obligations is a mortgage agreement. You will need a paper where the amount of debt is indicated - for this you need to take a certificate from the bank.

When the borrower collects all the necessary package of documents and transfers it to the registrar, it is necessary to obtain a receipt from him confirming the fact that the papers have been received. The receipt must indicate the date of their submission. 1 month is allocated for consideration of the appeal, so during this period you should receive a positive or negative (in case of refusal) response. Officials are not entitled to consider the application for more than this period.

3. When the Pension Fund officials make a decision, you will receive a notification - it will answer whether they will transfer it. If you have received a positive decision, then the matter remains small - contact the bank. It is necessary to focus on such an important point: funds from the Pension Fund on a loan to a bank account will be received only after 2 months.

4. In a situation where the amount of maternity capital fully repays the payment that remains, you need to visit your credit institution to obtain a certificate of debt payment and the absence of any claims against you. In case of partial debt closure, you are given the right to:

- To reduce the term of a housing loan, subject to maintaining the original amount of contributions;

- Or to recalculate the monthly payment.

To understand how you will continue to make settlements with a financial institution, you need to visit the lender and write an appropriate application. One way or another, you should get a new payment schedule.

If the bank refuses to repay the mortgage with mother capital

In the event that the bank gives you a negative answer in accepting maternity capital funds for a mortgage loan, we can safely defend our legal rights. Today, at the legislative level, the state obliges absolutely all banking structures, without exception, to accept maternity capital as payment for a mortgage loan. This applies to all banks that operate in Russia. The difference lies in only one thing - how much of the debt can be repaid by the borrower. This question will be determined by the bank.

A number of banks allow their consumers to use maternity capital funds as a down payment. Some consumers decide to reduce the amount of the principal debt at the expense of maternity capital. This is the most profitable option, since interest on the loan will already be charged on the remaining, that is, reduced amount of debt, which will significantly reduce the overpayment. There is another option

There is one important point - you do not have the right to use family capital funds to pay off penalties, fines or other financial sanctions on a mortgage loan.

State subsidies and assistance to large families

Many families, in addition to the maternity capital allocated at the federal level, may qualify for other subsidies. For example, most Russian regions at the local level approve their amounts of payments for large families with more than two children. The sum of money is allocated, as a rule, after the birth of the third child. At the same time, the family has a wider range of opportunities where they can spend these funds. For example, a mother has the right to receive monthly payments of a fixed amount in her hands, that is, in cash. The family also has the right to own a vehicle.

It should be noted that sometimes programs to improve the demographic situation at the regional level are superior in their generosity to the federal ones. You can become a happy owner of an amount from 100,000 rubles to 500,000! A number of Russian regions have developed special programs that guarantee full repayment of the loan in the event that a 3rd child is born in the family.

Therefore, before visiting the Pension Fund, ask and collect information about fertility programs that exist in your area. This must be done in order to “kill two birds with one stone”, that is, to do 2 things at once and arrange all the cash payments and benefits due to you. In this state of affairs, you will significantly reduce the time for solving your housing issue. The website of the Pension Fund contains a huge amount of information regarding this issue. In addition, you should visit the websites of regional authorities of the constituent entities of the Russian Federation.

Last modified: January 2019

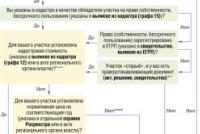

Families with two children have the right to count on assistance from the state to solve important housing issues. Among the areas in demand for the implementation of the certificate include the purchase of housing and the improvement of housing issues. If you have to wait until the baby is 3 years old to purchase housing with the help of capital, then repayment of the mortgage with maternity capital is available immediately after birth.

There are special requirements for housing, the conditions for the procedure regulated by federal law.

Methods of realization of capital

The main condition for using the MK before the child turns 3 years old is the presence of a formalized mortgage. Options for using funds from the budget involve the direction of funds:

- As a down payment on a home loan.

- For the repayment of interest and principal of the mortgage debt, in whole or in part.

- Use in military mortgage (for NIS participants).

Mortgage payment is made at a time, in an amount equal to the amount of the total debt, or in the form of partial repayment of the mortgage with a review of further repayment terms.

To exercise the right, they choose banks known for their successful long-term cooperation with the state on a number of social projects, including MK. If almost any bank allows you to pay part of the mortgage received, then the schemes for using mother capital for the first installment are not implemented by everyone.

Depending on whether the mortgage is repaid in full, or the MC reduces the amount of debt, reducing the borrower's credit burden, the registration procedure will be different. There are also general requirements for the implementation of funds from the budget. For example, the obligation to notify the bank of repayment before the due date.

What are the requirements for the borrower represented by the owner of the certificate for mother capital

The moment when you can use the capital is when the child reaches the age of three, but for mortgage borrowers this restriction is removed.

To successfully receive a tranche from the state, you must ensure that the following conditions are met:

- The loan, which was used to purchase housing, is targeted, i.e. aimed purely at improving the living conditions of the family.

- Housing must meet certain requirements put forward by the lender (real estate in private ownership, in a non-emergency, relatively fresh building, equipped with modern communications.

- The object for the residence of the Russian family must be purchased within the Russian Federation.

- In mortgage lending, the vast majority of loans are issued immediately to both spouses (in the presence of a legal marriage).

- After the last payment on the mortgage debt, it is important to have time to re-register the housing into common shared ownership within six months, with the allocation of shares to each family member. This requirement is ensured for implementation through a notarized document.

In the case of a regular home purchase without credit funds, parents are required to immediately register the property for everyone, but in the case of a mortgage, it is necessary to wait and only after that to introduce family members as owners.

Failure to comply with this condition entails a judicial challenge and cancellation of the payment with the forced collection of the amount of public funds from the borrower.

Obtaining funds to pay off a mortgage under the state program is a multi-stage procedure that requires interaction with the bank and the FIU.

Obtaining funds to pay off a mortgage under the state program is a multi-stage procedure that requires interaction with the bank and the FIU.

Since the basis for receiving the payment is the existence of a mortgage agreement, the first step is to visit the bank and conclude a mortgage transaction.

Coordination with the bank

The first stages of a mortgage transaction using capital are similar to the standard sequence of actions:

- Preliminary approval of the transaction based on the submitted application. The lender evaluates the solvency and reliability of a person by examining income documents and studying credit history.

- The bank's approval is valid for 3-6 months, during which future borrowers are looking for an option, taking into account the requirements put forward by the financial institution.

- Coordination of the selected housing and loan conditions in the bank. Evaluation and preparation of documents for the transaction.

- Transferring the advance payment to the seller and issuing a receipt.

- Signing of the contract of sale and mortgage agreement. At the same time, they purchase property insurance and sign a mortgage.

- The buyer re-registers the living space for himself, and the bank transfers the amount minus the first installment to the seller's details.

Since different banks have different programs using mother capital, it is recommended that you first study whether a mortgage for a particular type of property is available from the lender. For example, not all banks are ready to lend for the purchase of rooms or housing in shared construction.

Insurance is often issued by a subsidiary of a financial institution, or the borrower is provided with a list of accredited insurance organizations that allow collateral insurance.

The same is true with real estate valuation. The Bank recommends calling in experts with whom it cooperates and whose opinion it trusts.

Settlement with the seller is not always carried out by bank transfer. If desired, at the time of registration of real estate in Rosreestr, funds will be stored in it after the signing of the agreement and up to the re-registration of ownership.

After settlements with the seller, the mortgage transaction is considered completed, and the borrower receives an apartment and debt obligations to the bank. The owner of the certificate, having received a loan, has the right to immediately take advantage of early repayment through the state program. The next stage is related to the interaction with the FIU and the coordination of the payment of the tranche.

Coordination in the FIU

The Pension Fund of Russia is a state body that has all the powers to coordinate and control the implementation of the law on maternity capital. The basis for the transfer of funds under the state program will be a statement from a parent with a request to send money to pay off a mortgage loan.

In addition to the application itself, the parent must prepare an extensive package of papers confirming the legality of the transaction and the right to use the MK.

The package of papers includes:

- Applicant's passport (other identification document).

- Family certificate previously obtained from the FIU.

- Mortgage agreement with the bank.

- Real estate purchase agreement.

- A document from the bank indicating the amount of the balance of the debt.

- Marriage certificate (if the parents are in a legal relationship).

- Personal documents for children (certificates).

- Documents for the acquired property.

- A written undertaking to allocate an equal share in the mortgaged real estate to everyone after the removal of registration restrictions by virtue of the mortgage.

As a rule, shares are divided proportionally between all family members, but parents have the right to give up their property in favor of minors.

Based on the required list, the application to the FIU is preceded by the issuance of a certificate and the receipt of a notarial obligation. The mortgage borrower should already have the rest of the documents.

1 month is allotted for consideration and verification of the submitted application.

The legislation defines the maximum waiting time for the decision of the FIU, which cannot exceed 30 days. A few days after the decision is made, the Pension Fund notifies the borrower in writing.

The legislation defines the maximum waiting time for the decision of the FIU, which cannot exceed 30 days. A few days after the decision is made, the Pension Fund notifies the borrower in writing.

After a positive response, a transfer of money is organized equal to the amount of the mother's capital, or the amount of the balance of the debt. In the latter case, the remainder of the capital remains unused, and the parents retain the right to direct them to other uses permitted by law.

The pension fund transfers funds strictly according to the details indicated by the mortgage lender. It is impossible to receive money from the budget in cash.

Since early repayments require prior notification of the bank, the borrower is obliged to notify the bank of the upcoming transfer, about which an application is written in advance. In a written application, the client must indicate a request to accept the received amount as repayment, as well as recalculate payments if the payment is not final and exceeds the total amount of debt obligations.

Only three options for using mother capital when paying off a mortgage:

- Complete liquidation of the debt and closing of the credit line (this is possible if the loan amount was small, or it was issued long before applying for the capital).

- Reducing monthly payments by writing off the principal debt, while maintaining the duration of the contract.

- Reducing the repayment period, leaving payments unchanged.

If the client fully closes the loan obligations and terminates the contract ahead of schedule, it will be necessary to additionally verify the sufficiency of the amount. In the absence of any financial claims against the borrower, the bank prepares a certificate of liquidation of the debt, and also issues a mortgage, which will be required in Rosreestr to transfer housing to full ownership and remove restrictions. Parents have 6 months to fulfill the obligation to allocate shares to the family.

When the payment only partially covers the amount of the debt, the borrower issues a new repayment schedule (most often, banks insist on maintaining the term and reducing the payment).

Choosing a lender

The law expressly states that a loan that can be repaid with the help of an MK must be housing, i.e. directed exclusively to the purchase of housing. In the process of conducting the second stage of the sale of capital to pay off the mortgage, the FIU will consider the compliance of the financial institution with certain parameters, including the availability of a license.

Getting a loan from a microfinance organization does not give the right to direct capital funds, as well as a consumer loan from a bank.

Difficulties await those who want to get a loan in a consumer cooperative. Practice shows that it is difficult to obtain approval from the FIU from clients of agricultural consumer cooperatives, even if it is secured by a mortgage. To obtain payment, you will have to go to court and appeal the decision of the FIU, but there is little chance of satisfying the requirements of the claim.

When can it be denied?

In case of any deviation from the norms, the FIU may see signs of fraud in the transaction and refuse to approve.

The general list of reasons for a negative decision by the FIU includes:

- termination of the right to maternity capital;

- non-compliance with the requirements for the procedure, violation of the rules of action;

- the use of funds at the request of the parent goes beyond the permitted uses of the capital;

- excess of the amount in the request of the real balance by available funds;

- deprivation or restriction of a parent's rights;

- the lender does not meet the requirements of the FIU.

Due to the high risk of fraud by individual parents, the FIU will make sure to verify the identities of the father and mother for:

- deprivation of rights to children who gave the right to receive mother capital;

- established guilt in a crime against a child;

- cancellation of the right of the adoptive parent.

Sometimes the reasons for refusal are formal and successfully appealed in court. Each situation with the repayment of a mortgage at the expense of mother capital is individual, there are difficulties in selecting housing and agreeing on the terms of payment with the seller. In order to successfully use state funds under the mother capital program, a mortgage borrower should clarify the conditions for working with the state program with the bank in advance, and also consult with an employee of the PFR department. In the absence of fundamental problems with the documents and the compliance of housing and loan conditions, the procedure for repaying a mortgage with the help of an MK does not cause any particular difficulties.

Free question to a lawyer

Do you need advice? Ask a question directly on the site. All consultations are free of charge The quality and completeness of the lawyer's response depends on how fully and clearly you describe your problem

Legislatively defined the possibility of using for the purchase of housing. All mortgage lending banks are required to accept government certificates for interest payments and/or loan principal. Read more about how the mortgage is repaid by maternity capital (the documents in the Pension Fund necessary for processing and confirming the operation will also be listed) read below.

Definition

Maternal capital (MSC) is the federal budget funds transferred to the Pension Fund of the Russian Federation for the implementation of state support measures. As confirmation of the right to receive funds, program participants are issued a state-issued certificate. You can get it at the local distance of the Pension Fund of Russia at the place of residence.

One of the ways to quickly buy a residential property is to use maternity capital to pay off a mortgage. The documents necessary for processing the operation are transferred to which and makes a decision regarding the use of MSC funds.

How to get a certificate?

Before considering how the mortgage is repaid by maternity capital, the documents required for processing the operation, we will figure out how to get an MSC certificate.

Financial assistance from the state can be received by a woman who has given birth to or adopted a second and subsequent child. Fathers who have adopted a second child also fall into this category. Money can also be received by a child left without parents, upon reaching the age of majority. Mandatory conditions:

- Education in the full-time department.

- Age - up to 23 years.

You can get a certificate at the branch of the Pension Fund of Russia at the written request of the parent. A copy of the applicant's passport, birth (adoption) certificates of all children must be attached to the document. may request additional documents, in particular if the applicant is a single father. Within a month, the PRF reviews the documents and makes a decision on issuing a certificate. Notification is sent to the applicant within 5 days. In case of a positive decision, the document will indicate where and when it will be possible to obtain a certificate.

Application

MSC is annually indexed for inflation. Funds can be used in whole or in part in several ways. One of them is the improvement of living conditions. Within the framework of this direction, funds can be directed to the purchase (construction) of premises located on the territory of the Russian Federation. For the same purposes, you can take a loan from a bank, and then arrange the repayment of the mortgage with maternity capital. The documents required for the operation will be sent further. You can dispose of funds after 36 months after the birth or adoption of the second or each subsequent child. The loan can be issued to the mother or father.

Where to begin

The following list of documents for repayment of mortgage debt must be submitted to the bank:

- a copy of the MSC certificate.

- passport of a citizen of the Russian Federation.

- application for (standard bank form).

You should also order a certificate from the bank, which indicates the amount of debt broken down into the main part of the debt and interest. Here you can also get a certificate of ownership of real estate and a contract for the purchase of an apartment. The next stage is the transfer of documents to the Pension Fund.

Mortgage repayment by maternity capital: documents

For public funds, you need to prepare and submit certificates to the FIU. A complete list of documents for repaying a mortgage with maternity capital is presented on the website of the local Pension Fund of Russia. Short list:

- The original certificate for receiving state aid.

- A copy of the certificate holder's passport or other document confirming the person's identity. If the application is submitted by the spouse, then you must additionally provide a copy of the second passport and marriage certificate. If the application is submitted by an authorized person, then you must additionally provide a copy of the power of attorney.

- A copy of the mortgage agreement with state registration.

- Documents confirming the possibility of obtaining MSC funds by the creditor organization:

- for borrowers whose loans have been refinanced by AHML - a copy of the notification of the change of the mortgage holder;

- for borrowers whose loans are sold to other companies, a copy of the letter from the second owner of the mortgage. Notification of the change of ownership of the mortgage is sent to the borrower after the loan is refinanced by mail.

- A copy of the certificate of state registration of ownership of the premises.

- personal account.

- An obligation certified by a notary to register the apartment as a common property (with all residents) after the removal of the encumbrance.

- A certificate from the bank on the size of the balance of the debt, including interest.

Here are the documents you need to pay off a mortgage with maternity capital.

Only non-cash

The legislation states that it is only possible to repay the mortgage with maternity capital in a non-cash form. Documents are submitted to the Pension Fund of Russia in order to obtain permission for a cashless transfer of funds. But there are exceptions to this rule. If the family is building a house, then even before the start of work, you can get half the amount to a bank account. For the remaining amount, you will have to contact the Pension Fund of Russia and provide a package of documents for repaying the mortgage with maternity capital. At the same time, at least six months must elapse between tranches. Additionally, you need to prepare documents confirming the cost of the work performed: contracts with contractors, acts of work performed.

How is mortgage repayment carried out by maternity capital?

Documents for processing an application for the disposal of funds are transferred to the territorial office of the Pension Fund. The employee is obliged to provide a receipt indicating the number and date of acceptance of the document, his full name and position. Within a month, a decision is made to approve or refuse to use the MSC and is sent to the applicant in the form of a notification.

If the documents required to repay the mortgage with maternity capital are drawn up incorrectly, provided in an incomplete set, or the amount of funds for the MSC exceeds the balance of the debt, the offset may be refused. In the notification, the Pension Fund of Russia is obliged to indicate a reasoned reason for the refusal. This decision can be challenged in court.

What documents do you need for a bank to pay off a mortgage with maternity capital? Written notification from the FIU with permission to use state support funds. If there is a partial repayment of the loan, then the borrower must submit an application to the bank indicating the chosen method of changing the payment schedule:

- reduction of the term of the contract while maintaining the amount of payment;

- reduction of the amount of payment while maintaining the period of validity of the contract.

The Pension Fund of Russia is obliged to transfer funds within two months from the date of the decision. Maternity capital cannot be used to pay off fines and penalties that arose as a result of default on loan obligations. That is, until the transfer of funds to the PFR, the borrower is obliged to repay the debt in a timely manner. After mutual settlements, a new loan repayment schedule is drawn up.

The first way to pay off debt

At the expense of state aid, you can pay part of the advance, the body of the loan or interest on it. The first option is not available in every credit institution. Previously, banks classified clients who could not pay the down payment on their own as insolvent. Today, large financial institutions make concessions and accept MSCs. It should be noted that the conditions for such loans can hardly be called favorable for borrowers. These loans carry higher interest rates for short term loans.

The second way to pay off debt

A more acceptable option is to repay the body of the loan at the expense of the MSC, since after the amount of debt is reduced, interest is charged on the balance of the debt. If the borrower plans to repay it ahead of schedule, after mutual settlements, you can reduce the amount of the payment.

The third way to pay off debt

It is beneficial for the bank if only the interest on the loan is repaid at the expense of the MSC. He is guaranteed to receive part of the funds due. The same scheme is beneficial to the client, provided that he does not plan early repayment of the loan. The amount of the monthly payment is reduced, but not significantly.

Peculiarities

The certificate for MSC is issued for an unlimited period. You can receive the amount at any time. If the person indicated in the document has died, the second parent, guardian or the child himself can use the amount until he reaches 23 years of age.

You can use state aid funds at any time. The exception is when the owner of the certificate is going to use it to pay the down payment. In this case, it will be possible to use it after 36 months after the birth / adoption of the baby. There is one more limitation. The list of documents for repaying a mortgage with maternity capital should include a certificate from the Pension Fund confirming that state aid funds have not been used for any other purposes before.

In addition to federal, there are also regional programs to improve the demographic situation in the country. Some of them provide for special conditions for obtaining (registration) of property in ownership.

After the loan is repaid, the purchased property must be registered as joint property with all family members.

Closing of MSC

The maternity capital program was launched in 2007. Even then it was said that the program would not operate indefinitely. After 8 years, the first rumors appeared about the termination of the certificates. The reason for this was the fact that in 2014 the debt of the Pension Fund of Russia (through which all payments pass) amounted to about 1 trillion. rub. During the same period, 200 million rubles were paid out under MSC certificates. No final decision has been made. According to preliminary data, it will be possible to obtain a certificate until 12/31/18 inclusive, and use it in the next 10 years.

The following changes are being considered for the next year in terms of the program:

- issuance of certificates only to families with small or medium incomes;

- a new direction for the use of funds is considered - the rehabilitation of children with disabilities.

What documents for repaying a mortgage with maternity capital in 2018 should be submitted to the territorial office of the Pension Fund. It is no secret that a family that has taken out a mortgage loan and received a certificate for maternity capital can repay its debt to the bank or part of it with maternity capital. We will talk about documents for repaying a mortgage with maternity capital in the article.

Matcap capabilities increased

In 2018, unlike the previous year, the number of possible options for spending funds has been increased. Now maternity capital can be spent on the following purposes (part 3, article 7 of the Federal Law of December 29, 2006 No. 256-FZ, articles 2, 4 of the Federal Law of July 28, 2010 No. 241-FZ):

- improvement of living conditions (including repayment of mortgage loans and loans);

- children's education;

- increase in the funded part of the pension;

- purchase of goods and services for the social adaptation of a disabled child;

- monthly cash payments for low-income families;

- keeping a child in a nursery or kindergarten.

For more information about the possible directions for spending mother capital, see "".

In order to use public money, it is necessary to collect the appropriate set of documents. What documents are needed for the Pension Fund to pay off the mortgage? Let's talk about this in detail.

Since January 1, 2007, the country has been running a state program to help families with children - maternity (family) capital. Mat capital is understood as a measure of state support for families in which a second or subsequent child was born (adopted). Within the framework of this program, the state allocates funds to the family for certain targeted expenses, for example, for improving housing conditions or educating children.

Before you start talking about what documents are needed to repay the mortgage with maternity capital in 2018, you need to remember the need to issue a certificate for mother capital. Without this document, no subsequent actions to receive funds from the FIU are possible. The issuance of a certificate is the first necessary step in obtaining funding. Only after the certificate is issued, will the documents required to repay the mortgage with maternity capital 2018 be required.

We extinguish the mortgage with matcap

Maternity capital funds can be used to improve housing conditions, including (clauses 2, 3, 15 of the Rules, approved by Decree of the Government of the Russian Federation of December 12, 2007 No. 862, part 1 of article 10 of the Federal Law of December 29, 2006 No. 256- FZ):

- acquisition or construction of housing through transactions;

- construction and reconstruction of housing on their own, including with the involvement of contractors;

- for the payment of a down payment upon receipt of a credit (loan) for the purpose of acquiring (construction) housing;

- repayment of the principal debt and payment of interest on credits and loans taken for the purchase or construction of housing;

- repayment of principal and interest on credits and loans taken for the purpose of repayment of a previously received credit or loan for the purchase (construction) of housing.

To use maternity capital to pay off a mortgage, documents are submitted to the Pension Fund (clause 13 of the Rules, approved by Decree of the Government of the Russian Federation of December 12, 2007 No. 862):

- a contract for the sale of housing or equity participation in construction with a mark on state registration;

- passport of the spouse of the certificate holder and marriage certificate (if the spouse is indicated in the contract for the purchase of housing);

- loan agreement (loan agreement) for the purchase (construction) of housing;

- a mortgage agreement that has passed state registration (if the loan agreement (loan agreement) provides for its conclusion);

- an extract from the Unified State Register of Real Estate with information on the ownership of housing purchased or built using credit (borrowed) funds;

- a document confirming the non-cash transfer of money under a loan agreement to a bank account;

- a notarized written obligation of the person (persons) in whose ownership the residential premises are registered, to register the residential premises in common shared ownership with their spouse and children;

- a copy of the building permit;

- certificate of the creditor on the size of the balance of the principal debt and debt on interest for the use of the credit (loan) or certificate of the person selling the residential premises under the contract of sale with installment payment, on the size of the remaining unpaid amount under the contract;

- a previously concluded loan agreement (loan agreement) for the purchase (construction) of housing - in the case of the allocation of maternity capital funds to repay the principal debt and pay interest on loans and borrowings;

- an extract from the register of members of the cooperative (a document confirming the submission of an application for admission to membership of the cooperative, or a decision on admission to membership in the cooperative) - if you purchase housing in a cooperative.

It is these documents that must be submitted to the Pension Fund in order to repay a mortgage in a bank in the general case.

To date, many families throughout Russia have not only received a certificate for maternity capital, but have also taken advantage of it. In particular, over the 11 years of the program's existence, 4.7 million people have improved their living conditions by receiving maternity capital for a second child. In turn, 410,000 people channeled maternity capital into the education of their children.

Documents for mortgage repayment by maternity capital in 2019. We welcome you, happy owners of family happiness, but how could it be otherwise, because your family already has at least 2 children, has its own apartment, or there is a great desire to purchase one in a mortgage and have a certificate for maternity capital in your hands. It is quite reasonable to use a certificate for a partial solution of the housing issue, and in this article we will analyze the procedure, the documents necessary to repay the mortgage with maternity capital.

The law itself and the process are regulated by Decree of the Government of the Russian Federation No. 862 dated 12.12.2007. For 2019, the amount of support is 453,026 rubles.

This certificate is due to the parent at the birth (adoption) of a second child. The use of money is possible for the construction or purchase of housing in a mortgage. We do not forget about the rights of children to the acquired housing, because we spend their money.

You can pay off your mortgage with maternity capital as follows:

- pay the down payment;

- reduce the bulk of the debt. The most profitable solution, while there is a significant saving of the family budget on bank interest;

- full repayment of the mortgage loan, if the amount is enough.

Terms

And so, taking a mortgage under maternity capital, we observe the following conditions:

- we purchase housing only on the territory of our vast Motherland, i.е. RF;

- pay the initial fee;

- we spend money on paying off the mortgage of part of the principal debt, if it already was;

- we pay interest on the mortgage, also if the mortgage has already been taken.

There is no deadline for disposing of the certificate, use it at any time convenient for you, but you can get it only until the end of 2022.

Where and why to go

Through a painstaking and balanced decision, the family council chose the living space desired for acquisition and you are ready to make the first payment, but what is the procedure for repaying the mortgage with maternity capital and where to go first?

Let's consider two situations:

- You already have a mortgage. In this case, go to the bank for a certificate of the loan balance, and then to the Pension Fund.

- You are just about to apply for a mortgage. First of all, you decide with the bank (the best%, the smallest list of documents, etc.), conclude an agreement, then we do everything according to the first situation.

List of documents

List documents to the bank and pension fund.

To the bank

You should contact the manager with a request to prepare a special certificate of the balance of the principal debt for the PF.

- passport of a citizen of the Russian Federation;

- mortgage agreement.

After some time, you will prepare a certificate with data on the current balance of mortgage debt.

In PF

- passport of a citizen of the Russian Federation;

- an application for the transfer of maternity capital to repay a mortgage loan, the form will be provided in the pension fund;

- certificate for obtaining MK;

- documents from the bank confirming the availability of a mortgage loan (certificate, mortgage agreement, payment schedule, etc.);

- bank details for the further transfer of maternity capital funds;

- certificate of ownership and contract of sale of residential premises;

- a notarized obligation of the borrower to register the acquired residential premises in shared ownership after the loan is repaid.

After submitting the documents, you will receive a receipt on acceptance of the documents, with the obligatory indication of the date of their acceptance. Within 1 month, after checking the documents, representatives of the Pension Fund of the Russian Federation will issue you a written decision with consent, or maybe a refusal (we will tell you about the reasons for the refusal and what to do in this case a little later).

After receiving an agreement with a positive answer, go to the bank. Next, we notify the representatives of the bank and choose the method of spending your maternity capital. In Sberbank, you just need to look at your new payment schedule in Sberbank-online. You don't have to go and do anything else. The payment from the pension fund will automatically recalculate the schedule.

After approval by the Pension Fund, the payment to the bank will be made within a month.

We use it as a down payment and the best offers from banks

At the moment, quite a lot of banks accept maternity capital as payment for the down payment. The most favorable conditions are now in Sberbank and Uralsib Bank.

So in Sberbank now you can take a mortgage at a rate of 12% per annum, in Uralsib from 10.8%. At the same time, an additional down payment in cash is not required, as in VTB 24, Bank of Moscow, Raiffeisenbank. Mat. cap. counted as a down payment, but there is a special nuance.

The issuance of credit funds takes place in full and for the first 2 months (until the money from the PF comes in) you pay a mortgage from the entire value of the property. Then the maternity capital comes in and the payment schedule is recalculated. Those. after issuing a mortgage, you must quickly visit the PF with all the above documents and write an application for the use of maternity capital.

Example. Mortgage (maternity capital as PV) for an apartment worth 2 million for 10 years in Sberbank at 12% per annum. For the first 2 months you will have a payment of 28694.19 of the entire cost of the apartment (2 million), after transferring 453026 rubles from the Pension Fund, the payment will be reduced to 22137.29. Use our mortgage calculator to calculate the payment for you.

Reasons for rejection

After a long collection of documents, writing applications and other running around, you expect a positive result with trepidation, and in return you receive a decision with a refusal. The question arises: what could be the matter?

The reasons lie in the following:

- errors were made in the application;

- not provided a complete package of documents;

- the applicant has committed a crime against a child;

- deprivation of parental rights to a child for whom maternity capital was received;

- restriction by guardianship and guardianship authorities of the rights of a guardian.

After reviewing the reasons for the refusal, we draw conclusions for ourselves. When collecting a package of documents and filling out applications, be careful, it is better to double-check and ask several times than to waste time and nerves when re-submitting.

If you want to know more about mortgages, then be sure to subscribe to our website. We are waiting for questions in the comments. For free legal assistance, fill out the form in the lower right corner.