Monitoring the financial situation of the bank client. Analysis of the financial condition of the client. Study of market and non-market factors

According to the recommendations of the Bank of Russia, commercial banks are required to develop their own methodology for assessing the financial position of large corporate borrowers(hereinafter referred to as the OFPZ methodology), based on a system of indicators of financial performance of borrowers, as well as business and industry risk indicators.

Methodologies of various banks: characteristic features and features

The methodology for assessing the financial position of large corporate borrowers and the system of financial indicators described in it, as well as the scoring system for each group of coefficients for business risks (business and industry risks) must comply with the requirements and recommendations of the Bank of Russia, drawn up in a separate regulation and approved by the bank's management. In some cases, for example, if a Russian bank is part of an international financial group (the parent organization is located in another country), in addition to the requirements of the Bank of Russia, the OFPZ methodology must meet the criteria and requirements of the parent company.

The Bank of Russia recommends that banks annually adjust the approaches set out in the OFP methodology, as well as the set of coefficients for assessing the performance of enterprises, taking into account the current economic situation, going beyond the “classic” financial analysis. It is worth paying special attention to qualitative parameters, that is, the characteristics of the industry in which the borrower operates, to focus on business reputation, positive qualification characteristics of managers, the dynamics of the enterprise's profitability, including in the face of fierce competition and aggressive government policy in recent years. It is also necessary to develop methods for determining the reliability and reality of the financial statements of a potential borrower, which will help to identify symptoms of financial danger in a timely manner.

Each bank applies its own methods and means of analyzing the creditworthiness of large corporate borrowers. The reasons for this diversity may be a different degree of confidence in quantitative and qualitative methods for assessing creditworthiness factors, historically established individual principles, lending culture and creditworthiness assessment practices, and the use of a certain set of tools to minimize credit risk.

To assess the financial condition and creditworthiness of a large corporate borrower - a legal entity (except for credit institutions), objective indicators of its activity should be taken into account:

- the volume of sales of products;

- profit and loss;

- profitability;

- liquidity and turnover ratios;

- cash flows (receipt of funds to the borrower's accounts) to ensure the repayment of the loan and the payment of interest on it;

- composition and dynamics of receivables and payables;

- availability of reliable sources of loan repayment;

- relationships with contractors;

- dependence on suppliers and buyers;

- other parameters characterizing the financial and economic activities of the enterprise.

In addition, banks must take into account the business risks of the borrower (business and industry risks). Indicators for assessing such risks are often subjective (in international banks, these criteria are placed in a separate block and analyzed more carefully):

- efficiency of enterprise management (participation of shareholders in management);

- the market position of the borrower and its dependence on cyclical and structural changes in the economy and industry;

- the presence of government orders and government support for the borrower in a particular region or industry (for example, reimbursement of part of the paid excise taxes to the production alcohol enterprises from the federal budget of the region);

- history of repayment of the borrower's credit debt in the past;

- the possibility of introducing restrictions on the production and (or) supply of products (or raw materials for its production), including export / import;

- the level of competition in the industry, typical for the region;

- international risks (sales and delivery of products, political instability in the country of the manufacturer/buyer), etc.

All OFPZ methods have their similarities and differences. Each method has its own advantages and disadvantages. Let's carry out a comparative analysis of methods for assessing the financial position of large corporate borrowers.

Comparison of methods for assessing the financial position of large corporate borrowers of various banks

Bank No. 1 (Russian subsidiary of one of the international banks)

To determine the credit risk limit, a quantitative and qualitative assessment of two groups of risk factors is carried out with the assignment of a score to each:

1. disclosure of client risks, their characteristics:

- risks of business owners;

- client group risk;

- company management risks;

- industry risks;

- financial risks;

- relationships with banks;

- risks associated with the business plan, the limit per client;

2. disclosure and qualification of the transaction risk. The financial condition of the borrower is assessed on the basis of four groups of coefficients: profitability, liquidity, turnover and financial stability.

Evaluation of the results of calculating the coefficients is that after calculating the indicators, depending on the industry, the sum of points is calculated taking into account the weight of the indicator.

After that, the final score of the analysis of financial statements indicators and the financial position are determined: good / average / poor (according to the Regulations of the Bank of Russia dated 26.03.2004 No.

Advantages. Simplicity and transparency of assessment. Accounting for quantitative and qualitative indicators of the borrower's creditworthiness. For each group of factors, the analyst indicates not only scores, but also positive and negative factors. Analysts are not limited to accounting and reporting data. The credit history and business reputation of the borrower are taken into account. Management efficiency is taken into account, including the level of top managers. The position of the borrower in the industry and the region, the level of penetration of modern technologies are taken into account. Flaws. A large amount of assessed indicators (two groups, each of which is divided into indicators). Need for Industry Risk Assessment: The analyst should be aware of all industries in which borrowers operate. Short deadlines for evaluation (no more than two days). Writing a conclusion in English.

Bank No. 2 (included in the top 4 large Russian banks)

To determine the credit risk limit, a quantitative and qualitative assessment of five risk groups is carried out:

- risks associated with the share capital structure and the internal structure of a corporate client;

- risks associated with the credit history and business reputation of the borrower;

- risks associated with management efficiency;

- risks associated with the position of the borrower in the industry and the region, production equipment and the level of penetration of modern technologies;

- risks associated with the financial condition of the borrower.

The financial condition of the borrower is assessed on the basis of three groups of indicators. Evaluation of the coefficient calculation results consists in assigning a category for each of these indicators based on a comparison of the obtained values with the established sufficient values. After that, the sum of points is calculated taking into account the weight of the indicator, the borrower's creditworthiness class is determined, and a conclusion is made about the possibility of issuing a loan.

Advantages. Simplicity and transparency of assessment. Accounting for quantitative and qualitative indicators of the borrower's creditworthiness. The information used by analysts is not limited to accounting and reporting data. The structure of the share capital and the internal structure of the corporate client are taken into account. The credit history and business reputation of the borrower are taken into account. Management efficiency is taken into account, including the level of top managers. The position of the borrower in the industry and the region, the level of penetration of modern technologies are taken into account. Each of the coefficients used to assess the financial condition has a reference value with which its calculated analogue is compared. With the full repayment of overdue debt, the creditworthiness class is restored. Flaws. The rating score does not allow taking into account all the key features of the client. The reference value of the coefficients is not differentiated for individual industries with a different structure of assets and liabilities. The reference value of the coefficients is not differentiated on a territorial basis. Weighting coefficients are subjective, while minor shifts in the system of these coefficients can fundamentally change the final result and transfer the borrower from one class to another. The indicators used in the analysis of creditworthiness are calculated on the basis of reporting data, which do not allow assessing the creditworthiness of the borrower in the future. When determining the class of the borrower, information about the expected cash flows and financial results is not taken into account. Any errors and inaccuracies in determining the critical value of the sum of points can give a fundamentally wrong result.

Bank No. 3 (one of the Russian agricultural banks)

The financial position is the most important characteristic of the reliability of a legal entity. Analysis of the financial position includes the following steps:

- analysis of the composition, structure and quality of the balance sheet;

- analysis of performance results;

- calculation of indicators of liquidity, solvency and turnover, other qualitative indicators;

- conclusions about the financial position based on the results of the analysis;

- forecast of development prospects.

When determining the financial position of a legal entity, the calculated indicators are compared with industry average values and analyzed in dynamics.

Based on the results of the review, a conclusion is made indicating the criteria on the basis of which the financial position of the borrower is assessed as good, average or bad.

Advantages. Simplicity and transparency of assessment. Accounting for quantitative and qualitative indicators of the borrower's creditworthiness. Availability of specially designed formulas for determining the financial position of the borrower. The presence of corrective factors taken into account when assessing the financial condition of a legal entity. Use of reference values of financial ratios, differentiated by industry. Accounting for changes in indicators in dynamics with the subsequent construction of a forecast. A long analyzed period, which allows you to build an accurate forecast of the prospective creditworthiness of the borrower. Flaws. Lack of formal assessment of non-financial parameters. Non-financial indicators are taken into account additionally and do not make a significant contribution to the assessment results. Any errors and inaccuracies in determining the critical value of the sum of points can give a fundamentally wrong result. The reference values of the coefficients are not differentiated on a territorial basis.

Note that all methods for assessing the financial position of large corporate borrowers have common shortcomings:

- an incomplete methodological base for assessing the non-financial parameters of the borrower (lack of unified databases with available information about the client, such as tax payments, credit turnover in other banks, the availability of file cabinets, etc.). This is the main drawback inherent in all of these methods;

- non-transparency of doing business (when assessing the financial condition of an enterprise, it is necessary to apply a combined analysis of management and financial statements, since the latter does not allow external users to see the real picture of the business in question, and therefore understand the actual risks of lending to the enterprise).

Another drawback, inherent not only to the presented, but also to all Russian methods, is associated with the peculiarity of doing business in Russia, in particular, the poor transparency of the financial and economic activities of enterprises. Thus, any method for assessing the creditworthiness of a legal entity is highly sensitive to distortion (unreliability) of the source data, especially financial statements.

The above OFPZ methods show that one of the main areas of analysis of the borrower's condition in assessing its creditworthiness is financial analysis. Various aspects of financial analysis as a specific system are reflected in all the presented methods for assessing the quality of potential borrowers used by banks. Analysis of the financial condition of the borrower is the most significant characteristic of its creditworthiness. And each commercial bank establishes a specific set of financial indicators and their normative values independently, since today there are no regulatory documents regulating this area.

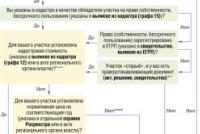

Symptoms of a possible financial danger for the bank

In practice, in order to correctly assess the financial position of a client and draw timely conclusions about its creditworthiness and the feasibility of concluding a transaction, an enlarged scheme for analyzing the risk profile of a transaction in the corporate lending segment is used, divided into financial blocks (Figure 1).

Picture 1. Scheme for analyzing the risk profile of a transaction in the corporate lending segment

Thus, risk analysts of a bank (whether it be a large Russian bank, an international bank or a regional branch) must form for each credit transaction a clear description and justification of the purpose of financing, the structure of the transaction, its risk profile (transaction with increased risk, moderate risk or risk-free transaction), as well as to assess the risks when analyzing the financial position of the client.

When financing working capital, it is necessary to analyze the operating cycle of the company, the causes and timing of the shortage of working capital, the timing and sources of replenishment of working capital. The structure of the transaction must correspond to the operating cycle (drawdown in the "low" season, repayment - in the "high" season, etc.), that is, it must be explained why the borrower is offered such a structure of the transaction.

A brief description of the cash flow model should include:

- the main assumptions on the basis of which the forecast of the movement of funds from operating activities was made (revenue remains at the same level / increases for one reason or another; the same with expenses);

- data on repayment of the loan (conclusion on the risk of refinancing);

- stress testing results;

- sensitivity analysis;

- conclusions.

Next, you need to analyze the sources of loan repayment: what determines the flow of funds, what are the possible negative factors, whether the bank satisfies (and why) the primary source of repayment. The presence of collateral can be seen as an additional comfort factor (but not as a basis for making a decision).

After that, the financial analyst provides in his opinion a description of the business model of the borrower / group: manufactured / sold products, features of the production cycle, seasonality, conditions under which sales are carried out, the specifics of settlements with counterparties, suppliers / customers (dependence), competitive advantages (reasons and the purpose of purchases from this particular borrower, the possibility of reorientation to another manufacturer), pricing (what factors affect the price), business risks, the interests of shareholders in this business, etc.

This also includes figures on the dynamics of production / sales with an explanation of the main factors determining this dynamics (how and due to what the borrower survived the crisis, what are his market positions and prospects). It would also be good to evaluate the effectiveness of the business model in comparison with similar enterprises. If there is a group, it is necessary to explain intra-group relationships, commodity-money flows.

The section "Financial analysis" should include a description of the causes and consequences of the dynamics and structure of the main indicators of the income statement and balance sheet, as well as an analysis of the ratios. All indicators should be considered in terms of their impact on the company's ability to fulfill loan obligations, that is, organically lead to the conclusion about the good/average/poor financial condition of the borrower. Particular attention should be paid to the size of the debt, its structure by maturity, to assess the risk of refinancing and the position of the bank relative to other creditors.

The final section of the risk analyst’s conclusion should contain conclusions - an assessment of the total risk when lending to a client (strengths and weaknesses of the client’s activities, business transparency, credit history in banks, dependence of the borrower’s financial condition on the activities of related structures, lack of consolidated reporting for the group, etc.) .

In addition, an important and integral element of the analysis of the financial situation of the borrower is the timely identification of symptoms and signs of possible financial danger for the bank (in banking terminology, this is called EWS - Early Warning Signals, or "early signals / signs of problem") both at the stage of issuing a loan, and and in the process of monitoring the loan until its full repayment. In banking practice, a separate large section in the OFPZ methodology is devoted to the criteria for determining early symptoms/signs of problems, as well as their set (Table 1).

Table 1. Early signals and signs of problems in the methodology for assessing the financial position of large corporate borrowers of various banks

| Signals of possible financial danger | Signs of an impending financial crisis in the client's business |

|---|---|

| financial signals | |

| Lack of receipts under contracts with buyers/customers and, as a result, lengthening the terms of settlements with suppliers | Systematic violation of the conditions for maintaining credit turnover in the bank, associated with the lack of receipts for the work performed/services rendered/delivered goods from buyers or customers |

| Lack of newly concluded contracts for the provision of goods / performance of work / provision of services (winding down of business) | Significantly exceeding the agreed credit limits in the bank(s) |

| Presence for several reporting periods in a row of negative values in lines 2400 (“Net profit (loss) of the reporting period”) of forms No. 2 and 1300 (total for sections “Capital” and “Reserves”) of form No. 1 of quarterly reporting in accordance with RAS | |

| Exceeding the value of the total debt burden indicator (Total Debt / EBITDA) according to the borrower's quarterly / annual official reporting in accordance with RAS, set at 3.5 | Opening current accounts by the borrower in other credit institutions without notifying the creditor bank, transferring all funds |

| Non-financial signals | |

| Establishing the production of previously unproduced products and, in connection with this, the development of a new sales market | Misappropriation of funds received from the loan |

| The emergence of the client's dependence on loans (usually short-term) due to increasing overhead costs | Insignificant and irregular cash receipts from the sale of goods, especially in combination with significant payments to suppliers and with an unjustified increase in credit sales |

| Client lapses in controlling their working capital (total overstocking, overstocking, illiquid assets, etc.) | Payments to other credit institutions or a sharp increase in the number of requests from them about the financial condition of the client |

| The client has large and unplanned losses | Manipulation of the client with checks |

| Unexpected radical changes in the composition of the company's management or unfavorable trends in the development of the industry | Violation by the client of the deadlines for preparing reports or submitting the necessary financial documents to the bank (this is often associated with their falsification). Clarifications of clients about the reasons for delays are in themselves signs of a problematic loan |

| Requests from the client to provide him with additional funds in excess of previously agreed limits | |

| Any unmotivated non-compliance with obligations | |

Banks are required to monitor changes in the structure of shareholders of the borrowing company, the state of its business as a result of financial / political instability in the country and the economy in order to make sure that its financial position is stable and that it complies with the terms of the loan agreement, as well as to search for new business opportunities. cooperation with the client. Loan monitoring is necessary in order to timely identify signs that the borrower may have difficulty repaying the loan (examples of early warning signals about the problem of corporate clients are discussed in the figure below). This should be done at an early stage in order to maximize the effect of the bank's corrective actions and reduce its losses.

Figure 2. Warning signals about problematic corporate clients

The human factor is one of the biggest barriers to early identification of problem loans. Employees responsible for analyzing corporate borrowers often do not report alarms due to their ignorance, heavy workload and short deadlines for assessing the financial situation of clients, as well as due to the lack of an automated system in Russian banks for detecting and preventing early signals/signs of problems (in European banks such a system is widely used).

Experience shows that problem loans, even after they have been identified, often turn out to be much worse than bank employees thought. But the situation can be even worse if the bank's management, aware of the problems in its loan portfolio, hides them and at the same time tries to compensate for losses by issuing risky loans and speculation. To avoid this, banks conduct periodic independent reviews by the internal audit function so that it reveals signs of loan problems missed or hidden by employees. Supervisory and regulatory audits (the Bank of Russia, external audit companies) also often reveal undetected NPLs. In the process of effective credit risk management, the bank's internal control service is the first to identify problem loans. The measures to be taken in case of such detection are shown in the following figure.

Figure 3

Monitoring loans is especially important not only at the stage of consideration of a loan transaction, but also at all stages of the loan process, especially at the stage of repayment of the loan or when it becomes overdue, or in case of violation of the terms of the minimum collateral amount or the value of financial ratios established by the loan agreement. In order to avoid violations of loan agreements, as well as to eliminate them in a timely manner, the bank is developing a methodology for assessing the financial position of large corporate borrowers, which not only provides for assessing the borrower's creditworthiness as the main way to reduce credit risk, but also includes general principles. Using these principles, it is easy to identify early signs of problems in a timely manner and try to eliminate or prevent a loan delinquency or default by the borrower.

Based on the materials of the article: Finogeev D.G., Shcherbakov E.M. Assessment of the creditworthiness of legal entities on the example of the largest banks of the Russian Federation // Modern problems of science and education. 2013. No. 6.

The purpose of the study is to analyze the process of organizing monitoring of the financial situation of the borrower and assessing the quality of debt service.

Research objectives:

- to give a general description of credit monitoring and directions for monitoring the issued loan;

- analyze the scheme for monitoring the state of the borrower and identifying bad debts;

- determine the procedure for assessing the quality of debt service on a loan;

- characterize the legal framework governing credit monitoring;

- analyze the experience of monitoring the financial position of the borrower and assessing the quality of debt service and creating a reserve for possible losses: characteristics of business processes for supporting the loan; analysis of the financial position of the borrower; formation and regulation of a reserve for possible losses on loans; reflection in the bank's accounting of operations on the issued loan;

- identify problems of loan portfolio quality;

- identify ways to improve the mechanisms for managing bad debts;

- explore the mechanisms of control by credit organizations, the return of overdue debts by the borrower.

Introduction……………………………………………………………………………………3

Section 1 Theoretical foundations of credit monitoring……………………………..5

1.1. General characteristics of credit monitoring. Directions for monitoring the issued loan…………………………………………………………………………………….5

1.2. Scheme for monitoring the borrower’s condition and identifying problem debt……………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………

1.3. The procedure for assessing the quality of debt service on a loan…………………………..8

1.4. Legal framework governing credit monitoring……………..9

Section 2. Analysis of the experience of monitoring the financial position of the borrower and assessing the quality of debt service. Creation of a reserve for possible losses…………………...11

2.1. Characteristics of business processes to support the loan…………………11

2.2. Analysis of the financial position of the borrower………………………………………..12

2.3. Formation and regulation of a reserve for possible losses on loans……..14

2.4. Reflection in the bank's accounting of operations on the issued loan ...... .16

Section 3. Problems of improving the quality of the loan portfolio. Ways to solve them…18

3.1. Loan portfolio quality problems……………………………………………18

3.2. Improving the mechanisms for managing bad debts…...20

3.3. Control mechanisms by credit institutions, repayment of overdue debts by the borrower……………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………

Conclusion………………………………………………………………………………….24

Bibliographic list……………………………………………………………..25

Annex A - Types of monitoring and timing of its implementation………………………...27

Annex B - Differences in the content of quarterly and monthly monitoring……………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………….28

Appendix B - Documents requested as part of financial monitoring……………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………..29

Annex D - Market and non-market factors…………………………………...30

Annex D - Criteria affecting the determination of the quality of debt service on a loan…………………………………………………………………………………………….32

Appendix E - Loan quality categories……………………………………………...35

Annex G - Risk Rate…………………………………………………………..36

Appendix H - Options for determining the minimum reserve rate for a portfolio of homogeneous loans………………………………………………………………………………..

Files: 1 file

As can be seen from Appendix A, the two types of monitoring complement each other, since monthly monitoring is not carried out on the dates of the quarterly monitoring.

Based on the type of monitoring, documents requested from borrowers can also be divided into two groups: documents requested quarterly and documents requested monthly. The grouping of documents is given in Appendix B.

As part of monitoring, they usually request a detailed breakdown of long-term and short-term financial investments on pages 140 and 250 of the balance sheet, indicating the names of specific investments. In the course of the analysis of financial investments, the following are studied: the dynamics of financial investments; structure of financial investments; purpose of financial investments; sources of investment financing; liquidity of financial investments and the possibility of their rapid implementation.

The ratio of market and non-market factors is shown in Appendix D.

The monitoring results are drawn up in the form of an analytical note, which usually contains the following information: name of the borrower, type of loan product and transaction parameters; industry of the borrower, a brief analysis of market and non-market factors; conclusions based on the results of vertical and horizontal analysis of the balance sheet and income statement; conclusions based on the results of the analysis of liquidity, financial stability, business activity and profitability; analysis of sales proceeds; analysis of receivables, accounts payable, financial investments, stocks, loans and credits; analysis of turnover in banks; analysis of the order portfolio and the borrower's cash flow plan; conclusions based on the results of collateral monitoring; a general conclusion about the change in risk for a particular transaction/borrower.

Factors that may indicate the emergence of potential problems for the borrower: a sharp decrease in revenue and receipts to settlement accounts; increase in inventories and work in progress; growth of receivables, growth of overdue debts; growth of accounts payable, including overdue; loan portfolio growth; the presence of a card file for accounts; presentation of requirements of tax authorities; bringing claims from third parties; drop in demand for products; the presence of predictable cash gaps without additional financing, etc.

1.3. The procedure for assessing the quality of debt service on a loan

The quality of debt service is an indicator that characterizes how timely and in full the borrower/debtor repays its obligations under the loan/factoring agreement.

Depending on how timely and in full the borrower repays mandatory payments on its obligations to the bank, the quality of debt service is classified into one of three categories: good quality of debt service; average quality of debt service; unsatisfactory or poor quality of debt service.

Determination of the quality of debt service on a loan is carried out in accordance with the criteria defined by the Regulation of the Bank of Russia No. 254-P dated March 26, 2004 No. “On the procedure for the formation by credit institutions of reserves for possible losses on loans, on loans and equivalent debts”.

The quality of debt service on loans is assessed by the bank for each issued loan, the quality of debt service under factoring agreements is assessed by the bank within the framework of each assigned monetary claim against the debtor/supplier.

Criteria influencing the determination of the quality of debt service on a loan are presented in Appendix D.

It should be taken into account that the assessment of debt service quality is an integral part of the assessment of the loan quality category. When carrying out inspections, the Bank of Russia has the right to assess the content of loan agreements for the presence / absence of conditions in them, upon the occurrence of which the borrower acquires the right to fulfill loan obligations in a more favorable regime. If there are no provisions in the original agreements that clearly stipulate such conditions and/or parameters, and an additional agreement with improved terms has been concluded in favor of the borrower, then the loan should be recognized as restructured with an appropriate assessment of the debt service quality.

1.4.Regulatory framework governing credit monitoring

The organization of the credit monitoring system is based, as a rule, on the following documents:

Current legislative acts and regulatory documents of the Russian Federation;

Regulations of the Bank of Russia, the Federal Financial Monitoring Service and the Federal Financial Markets Service;

Internal regulatory documents of a credit institution.

The legislation of the Russian Federation includes such documents as:

Federal Law of August 7, 2001 N 115-FZ "On counteracting the legalization (laundering) of proceeds from crime and the financing of terrorism" (as amended and supplemented on July 20, 2012 N 121-FZ) 2 , with p 2 tbsp. 7 of which, in order to prevent the legalization (laundering) of proceeds from crime and the financing of terrorism, credit institutions, among other organizations carrying out transactions with funds or other property, are obliged to develop internal control rules, appoint special officials responsible for the implementation of internal control rules control, as well as take other internal organizational measures for these purposes;

Federal Law No. 86-FZ of July 10, 2002 “On the Central Bank of the Russian Federation (Bank of Russia)” (with amendments and additions of November 21, 2011 N 327-FZ) 3 , in accordance with paragraph 9 of Art. 4 of which the Bank of Russia supervises the activities of credit institutions and banking groups;

Federal Law No. 39-FZ of April 22, 1996 "On the Securities Market" (with amendments and additions of July 28, 2012 N 145-FZ) 4 , in accordance with paragraph 11 of Art. 42 of which the FFMS of Russia controls the implementation by professional participants of the securities market of the legislation of the Russian Federation.

Thus, the economic purpose of implementing a credit monitoring system in a commercial bank is reduced to a more efficient use of the interdependence of the lending policy and the potential of the bank, as well as to turning the function of predicting credit policy into a source of competitive advantages for a commercial bank, expressed in maximizing profits and minimizing risks in the process of formation resource base and efficient allocation of borrowed funds.

Section 2. Analysis of the experience of monitoring the financial position of the borrower and assessing the quality of debt service. Creating a reserve for possible losses

2.1. Characteristics of business processes for loan support

The employee of the credit department constantly monitors compliance with the fulfillment of the main and accessory obligations of the borrower, including: control of the targeted use of credit resources, control of timely and full repayment of principal and interest, commissions 5 .

Control over the fulfillment by the borrower of the conditions for business development: is carried out by an employee of the business development unit responsible for this loan transaction. If the conditions for business development are specified in the loan agreement, then control is carried out within the framework of these conditions.

Credit risk control: an employee of the credit department accompanying a credit transaction is obliged to request from the borrower official financial statements, documents, as well as other information provided for by the credit, which is necessary to analyze the financial and economic activities of the borrower and may affect debt servicing and its repayment.

Financial statements are analyzed on a quarterly basis as of the date following the reporting one, throughout the entire term of the credit transaction using the calculation module. Based on the results of the analysis, a report is drawn up, which also reflects the results of assessing the level of credit risk (taking into account the quality of loan servicing) and the calculation of the reserve. The report must be signed by the employee who compiled it, the head of the credit department and included in the credit file.

The formation and regulation of the reserve for possible losses on loans and the reserve for possible losses on contingent liabilities of a credit nature is carried out in accordance with the procedure established by the current regulatory documents of the Bank of Russia and the internal documents of the Bank.

An employee of the credit department monthly monitors the amount of funds passing through the borrower's accounts with the Bank. If there is a significant decrease in the amount of cash in comparison with the amount that was taken into account when determining the creditworthiness of the borrower, the employee of the credit department is obliged to establish the reasons for the decrease in volumes.

Upon receipt of information about the borrower, which, in accordance with the loan agreement, may be the basis for the Bank's refusal to fulfill obligations under the loan agreement or the demand for early repayment of the loan, or any other information that may adversely affect the return of the loan product and the payment of interest, the loan officer is obliged notify the Head Office immediately.

Collateral control: control over the availability, safety and liquidity of property accepted as collateral is carried out by an employee of the collateral service in accordance with the procedure established by separate regulatory documents of the Bank. Valuation of the value of collateral in cases where the value of collateral is taken into account when forming a provision for possible losses on loans is carried out by an employee of the collateral service on a quarterly basis, a report with the results of the assessment is included in the credit file.

The control of the guarantor in a credit transaction is carried out by an employee of the credit department in accordance with the terms of the guarantee agreement.

If negative factors arise related to the condition of the collateral, the financial condition of the mortgagor (guarantor, guarantor), the employee of the collateral service (an employee of the credit department) immediately notifies his manager, the head of the troubled assets service, the credit department of the branch, the security service and the control department credit risks of the Head Office to determine a plan for further actions.

Control over the provision and maintenance of loan products by credit departments: the credit risk control division monitors the compliance of the terms of the provided loan products with the decisions made, as well as the compliance of the loan transaction and the maintenance of the loan product with the internal regulatory documents of the Bank and the regulatory documents of the Bank of Russia.

In addition, the appearance of debt with signs of increased credit risk is controlled.

2.2. Analysis of the financial position of the borrower

The process of assessing the financial condition of the borrower consists of several stages: filing an application with the bank; initial assessment of the borrower's creditworthiness by a bank employee and determination of his rating as a debtor (it is expressed in points and includes many quantitative indicators); assessment by the bank of credit opportunities, taking into account the amount requested by the potential client; meeting of the credit committee of the bank, where the decision on the issuance of funds is made. If this decision is positive, all the terms of the loan agreement are determined.

Consider the features of assessing the creditworthiness of an individual borrower.

An obligatory step in lending to individuals is the procedure for assessing their creditworthiness, which is carried out primarily on the basis of information regarding their income level. At this stage, a scoring assessment of the borrower and a study of his credit history are also mandatory 6 . The methodology for assessing the borrower's creditworthiness in terms of such an indicator as the level of income is carried out on the basis of data not only directly on income, but also on the degree of risk of its loss. It is possible to determine the level of income by studying the relevant salary certificates or tax returns. At the same time, it is mandatory to make certain adjustments to the results, taking into account the risk coefficients of the bank itself and mandatory payments. The term "credit history" is used to determine information about the receipt of loans by a possible borrower in the past, as well as their repayment. In many countries, the formation of credit histories is carried out by specially created bodies for this purpose - credit bureaus.

Scoring is a statistical or mathematical model, with the help of which, based on the credit histories of other customers, the bank is able to calculate how likely it is that the next potential borrower will return the funds received on time. Such a methodology for assessing a borrower in the most simplified form is a kind of weighted sum of certain characteristics, which is necessary to form an integral indicator. It, in turn, is compared with a numerical threshold (by and large, which is the so-called break-even line) and is calculated depending on how many customers making payments on time are needed to compensate for losses from one particular debtor. Such an assessment of the borrower's solvency is necessary in order to determine the integral indicator of each potential client and compare it with the above line (accordingly, only those borrowers who have this indicator above the break-even line will be able to receive a loan).

The assessment of the borrower's financial condition is made taking into account trends in changes in the financial condition and factors influencing these changes. To this end, it is necessary to analyze the dynamics of estimated indicators, the structure of balance sheet items, the quality of assets, and the main directions of the economic and financial policy of the enterprise.

When calculating the indicators (coefficients), the principle of caution is used, that is, the recalculation of the assets of the balance sheet downwards based on an expert assessment.

To assess the financial condition of the borrower, three groups of estimated indicators are used: liquidity ratios; ratio of own and borrowed funds; turnover and profitability indicators.

Liquidity ratios characterize the security of the enterprise with working capital for doing business and timely repayment of urgent obligations. The absolute liquidity ratio characterizes the ability to instantly repay debt obligations and is defined as the ratio of cash and highly liquid short-term securities to the most urgent obligations of the enterprise in the form of short-term bank loans, short-term loans and various accounts payable. Highly liquid short-term securities in this case mean only government securities and securities of the Savings Bank of Russia.

The intermediate coverage ratio (critical liquidity) characterizes the ability of the enterprise to quickly release their economic turnover of funds and pay off debt obligations.

To calculate this ratio, the groups of articles “short-term financial investments” and “accounts receivable (payments for which are expected within 12 months after the reporting date)” are preliminary evaluated. These items are reduced by the amount of financial investments in illiquid corporate securities and insolvent enterprises and the amount of uncollectible receivables, respectively.

The current liquidity ratio (general coverage ratio) is a general indicator of the company's solvency, the calculation of which includes all current assets, including tangible ones (the result of section 2 of the balance sheet).

For the calculation, the already named groups of balance sheet items are preliminarily adjusted, as well as “accounts receivable (payments for which are expected in more than 12 months)”, “stocks” and “other current assets” in the amount of bad receivables, illiquid and hard-to-sell stocks and costs, respectively and the debit balance on the account "Deferred income".

The ratio of own and borrowed funds is one of the characteristics of the financial stability of the enterprise and is determined by: Indicators of turnover and profitability. The turnover of various elements of current assets and accounts payable is calculated in days based on their volume of daily sales (one-day sales proceeds). Daily sales volume is calculated by dividing sales revenue by the number of days in the period (90, 180, 270, or 360).

Average (for the period) values of current assets and accounts payable are calculated as the sum of half values for the beginning and end dates of the period and full values for intermediate dates, divided by the number of terms, reduced by 1.

Similarly, if necessary, the turnover indicators of other elements of current assets (finished products, work in progress, raw materials and materials) and accounts payable can be calculated. Profitability indicators are determined in percentages or shares.

Other indicators of turnover and profitability are used for general characteristics and are considered as additional to the first five indicators. Evaluation of the calculation results of five coefficients consists in assigning a category to the Borrower for each of these indicators based on a comparison of the obtained values with the established sufficient ones. Further, the sum of points for these indicators is determined in accordance with their weights.

The weight of the indicator multiplied by the value of all categories. For the remaining indicators of the third group (turnover and profitability), optimal or critical values are not set due to the large dependence of these values on the specifics of the enterprise, industry affiliation and other specific conditions. Evaluation of the calculation results of these indicators is based mainly on the comparison of their values in dynamics.

In the Syktyvkar Bank of the Joint Stock Company of the Security Council of the Russian Federation, the calculation of all necessary coefficients is carried out using a software package. Financial statements are entered into a special program that calculates various indicators. Based on them, the computer determines the rating of the borrower. The inspector of the Credit Department makes the appropriate printouts of the calculations and these data are stored in the file for this borrower.

Qualitative analysis is based on the use of information that cannot be expressed in quantitative terms. To conduct such an analysis, information provided by the Borrower, the security service and database information is used.

At this stage, the risks are assessed:

Industry:

- - state of the market in the industry;

- - trend in the development of competition;

- - the level of state support;

- - the importance of the enterprise on a regional scale;

- - risk of unfair competition from other banks;

Shareholding:

- - risk of share capital redistribution;

- - Consistency of positions of major shareholders;

Regulation of the enterprise activity:

- - subordination (external financial structure);

- - formal and informal regulation of activities;

- - licensing of activities;

- - benefits and risks of their cancellation;

- - risks of fines and sanctions;

- - law enforcement risks (the possibility of changes in the legislative and regulatory framework);

Production and management:

- - technological level of production;

- - risks of the supply infrastructure (changes in supplier prices, disruption of supplies, etc.);

- - risks associated with banks in which accounts are opened;

- - business reputation (accuracy in fulfilling obligations, credit history, participation in large projects, quality of goods and services, etc.);

- - quality of management.

The final step in assessing creditworthiness is to determine the borrower's rating, or class. 3 classes of borrowers are established: First-class - lending to which is beyond doubt; second class - lending requires a balanced approach; third class - lending is associated with increased risk. The rating is determined on the basis of the sum of points for five main indicators, the assessment of the remaining indicators of the third group and a qualitative risk analysis.

S= 1 or 1.05 - the borrower can be referred to the first class of creditworthiness; S greater than 1, but less than 2.42 - corresponds to the second class; S equal to or greater than 2.42 - corresponds to the third class.

Further, the preliminary rating determined in this way is adjusted taking into account other indicators of the third group and the qualitative assessment of the Borrower. If these factors have a negative impact, the rating may be reduced by one class. This grouping allows you to control the identification of possible losses from outstanding loans and their prevention.

Initially, according to the efficiency class, the risk group is determined, respectively, in ascending order. Further, depending on how the client repays the principal and interest on it, the risk group may change. Loan classification table based on formal credit risk assessment criteria.

In order to maintain the stability and sustainable functioning of the Russian banking system, commercial banks are required to create a reserve for possible loan losses. The allowance for possible losses on loans is used only to cover outstanding loans by customers (banks) on the principal debt.

Lending divisions of Sberbank of Russia and its branches make monthly (as of the first day of the month following the reporting month) adjustment of the risk of all issued loans and debts equated to loans, taking into account changes in the amount of actual loans or debts equated to loans, the loan risk group (changes in the duration terms of overdue payment on debt equated to a loan), the official exchange rate established by the Bank of Russia on the last day of the reporting month.

In order to reduce the likelihood of incurring losses as a result of credit relations, the Syktyvkar Bank of the Joint Stock Company of the Security Council of the Russian Federation uses one of the forms of securing the repayment of a loan (pledge, guarantee, guarantee, etc.). The risk level is set. And now it remains only to add control over the intended use of the loan and periodic inspection of the pledged property to the methods of its regulation. So, issuing one loan after another, the Syktyvkar Bank of the Joint Stock Company of the Security Council of the Russian Federation forms its loan portfolio. There is a need to analyze and evaluate specific types of risk that the bank faces in any type of operations. Here we are already talking about the risks within the aggregate of borrowers.

Posted on the site 14.10.2009

In the context of macroeconomic instability and the growth of defaults on loans to corporate borrowers, the importance of operational control over their financial and economic activities by credit institutions is growing. This control, implemented in the form of a system of in-depth monitoring of the financial condition, will help to immediately respond to negative trends in the financial and economic activities of borrowers.

The current macroeconomic situation in the Russian Federation leads to the emergence of a large number of risks that manifest themselves both in the financial sector and in the sphere of real production. It should be noted that the current economic situation has revealed all the problems of corporate governance, not only for borrowing enterprises, but also for credit institutions themselves. According to some experts, the share of problem loans in the loan portfolio of some large banks is currently approaching 10-15%.

Starting from September-October 2008, almost all banks tightened the requirements for new borrowers in terms of collateral and creditworthiness. They revised the parameters of the financial and economic activities of new borrowers, which suit creditors. Banks began to take a closer look at the activities of existing borrowers.

What is in-depth monitoring and why is it needed?

Advanced Monitoring is carried out in an unstable economic situation in order to respond faster if the borrower has problems.

Deep monitoring differs from regular monitoring:

frequency of holding;

A large amount of information under consideration;

complex character.

Monitoring— periodic assessment of the financial condition of the borrower based on financial statements in order to determine the probability of repayment of the loan and the estimated provision for possible losses on loans.

According to the Regulation of the Central Bank of the Russian Federation of March 26, 2004 No. 254-P "On the procedure for the formation by credit institutions of reserves for possible losses on loans, on loan and equivalent debt" (hereinafter - Regulation No. 254-P), the assessment of credit risk for each issued loan ( professional judgment) should be carried out by the credit institution on an ongoing basis.

The credit institution, in accordance with the procedure established by the authorized body (authorized bodies) of the credit institution, documents and includes in the borrower's file information about the borrower, including the professional judgment of the credit institution on the level of credit risk on the loan, information on the analysis, which resulted in a professional judgment , conclusion on the results of assessing the financial position of the borrower, calculation of the reserve.

These documents are compiled:

For loans to individuals - at least once a quarter as of the reporting date;

For legal entities that are not credit institutions - at least once a quarter as of the date following the reporting one;

For loans granted to credit institutions - at least once a month as of the reporting date.

Factors that determine the conduct in-depth monitoring:

The need to understand the real state of affairs of specific borrowers and the industry as a whole;

Growth of non-payments;

An atmosphere of general distrust in the corporate and financial sectors;

Increase in the number of defaults on corporate bonds;

The decline in production in the main sectors of the economy;

Refusal of most banks to provide loans, even for open limits;

Requirements of Regulation No. 254-P, Regulation of the Central Bank of the Russian Federation of March 20, 2006 No. 283-P "On the procedure for the formation of reserves for possible losses by credit institutions", as well as the need to determine the reserve for possible losses on loans, including for the purposes of generating bank reporting on IFRS.

As can be seen from the figure, the two types of monitoring complement each other, since monthly monitoring is not carried out on the dates of the quarterly monitoring.

Table 1. Differences in the content of quarterly and monthly monitoring

| Types of operations carried out as part of monitoring | Quarterly monitoring | Monthly monitoring |

| Vertical and horizontal analysis of the balance sheet and income statement | + | - |

| Analysis | ||

| liquidity | + | - |

| financial stability | + | - |

| business activity | + | - |

| Profitability | + | - |

| Revenue research | + | + |

| Study of receivables and payables | + | + |

| Analysis of reserves, financial investments, loans and credits | + | + |

| Analysis of turnover in banks, the borrower's cash flow plan, portfolio of orders, contracts | + | + |

| Analysis of the influence of market and non-market factors | + | + |

Industries most affected by the crisis

In our opinion, the factors contributing to classifying the industry in which the borrower operates as problematic may be the following:

A significant drop in demand for products;

The main product of the industry is not an essential product;

Significant production costs;

The industry is significantly dependent on government orders;

The industry's products are exclusive and targeted at a specific group of buyers.

Based on these factors, problem areas include:

Wholesale trade;

Trade in luxury goods (luxury);

Car trade;

Construction;

Metallurgy.

At the same time, it should be noted that enterprises operating in these industries do not necessarily experience serious financial difficulties, but it is necessary to pay special attention to market factors in the course of analyzing their financial activities.

Documents required for monitoring the condition of borrowers

Based on the type of monitoring, documents requested from borrowers can also be divided into two groups: documents requested quarterly and documents requested monthly. The grouping of documents is shown in Table 2.

Table 2. Documents requested as part of financial monitoring

| Title of the document | Quarterly monitoring | Monthly monitoring |

| 1. Balance | + | - |

| 2. Profit and loss statement | + | - |

| 3. Form 3, 4, 5 | + (annual reporting) | - |

| 4. Transcripts for reporting | + | - |

| — fixed assets | + | - |

| - Construction in progress | + | - |

| — long-term and short-term financial investments | + | - |

| — stocks | + | - |

| - accounts receivable | + | - |

| — long-term and short-term loans and borrowings | + | - |

| - accounts payable | + | - |

| - cost | + | - |

| - business expenses | + | - |

| - management expenses | + | - |

| — operating income | + | - |

| - operating expenses | + | - |

| 5. Certificates from banks about turnover, card file, loans | + | + |

| 6. Certificate of the IFTS on debts on taxes and fees | + | + |

| 7. Questionnaire with basic data about the borrower | + | + |

| 8. Turnover balance sheets for accounting accounts | + | + |

| - accounts receivable, c. 62, 76 | - | + |

| - accounts payable, c. 60, 76 | - | + |

| — proceeds from sales, cf. 90 | - | + |

| - stocks, c. 10, 20, 41, 43, etc. | - | + |

| - financial investments, c. 58 | - | + |

| - loans and credits 66 and 67 | - | + |

| - analysis of the account. 51 and 52 monthly | + | + |

| 9. Cash flow plan | + | + |

| 10. Tax declarations (VAT, income tax) | + | + |

| 11. Order book | + | + |

| 12. Copies of the main contracts | + | + |

Quarterly monitoring based on financial statements

The analysis algorithm based on financial statements can be represented as follows:

Vertical and horizontal analysis of the balance sheet and income statement;

Study of receivables and payables, stocks, financial investments, loans and credits;

Research of liquidity and solvency;

Analysis of financial stability;

Analysis of business activity;

Profitability analysis;

Analysis of market and non-market factors.

Typically, credit institutions assess the financial condition of the borrower on the basis of their own methodology, which most often involves the calculation of the rating based on a number of financial indicators. Let us dwell on the most important components of monitoring in the current conditions.

RECEIVABLE RESEARCH

As part of the monitoring, a breakdown of receivables is requested (lines 240, 241, 246, etc. of the balance sheet). In general, at least 80% of all receivables, as well as all debtors whose debt is at least 5% of all receivables, must be deciphered with the indication of counterparties.

Debt analysis examines:

Dynamics of accounts receivable and its comparison with the dynamics of revenue;

The presence and dynamics of overdue receivables (determined according to the borrower's data, as well as on the basis of the dynamics of reserves for doubtful debts, account 63);

The structure of receivables (dependence on large buyers, customers, identification of companies affiliated with the borrower);

Determination of the main forms of settlements with buyers and their change.

RESERVES RESEARCH

Stocks can be classified:

For raw materials and materials;

Costs in work in progress;

finished products;

Goods shipped;

Future expenses.

In the course of the analysis of reserves, the following are examined:

Stock structure;

Inventory dynamics.

In addition, it is necessary to compare the dynamics of work in progress and finished products with the dynamics of revenue, receivables and payables.

RESEARCH OF LONG-TERM AND SHORT-TERM FINANCIAL INVESTMENTS

As part of monitoring, they usually request a detailed breakdown of long-term and short-term financial investments on pages 140 and 250 of the balance sheet, indicating the names of specific investments. In the course of the analysis of financial investments, the following are examined:

Dynamics of financial investments;

Structure of financial investments;

Purpose of financial investments;

Sources of investment financing;

Liquidity of financial investments and the possibility of their rapid implementation.

RESEARCH OF MARKET AND NON-MARKET FACTORS

The ratio of market and non-market factors is shown in Table 3.

Table 3. Market and non-market factors

| No. p / p | Name of evaluation criterion | Factors assessed |

| 1 | Changes in the principal activities of the borrower |

1. Change in the degree of legal and financial independence of the company (entry into groups of companies and holdings or separation from them), which led to the disruption of existing economic ties. 2. Loss of economic ties with the main suppliers of raw materials (goods) or buyers, a sharp increase in prices for consumed materials (purchased goods). 3. Change (tightening) of the terms of settlements with suppliers. 4. Changes in the structure of proceeds from sales through the use of "non-monetary" forms of payment (bills, offsets, and others). |

| 2 | Assessment of changes in the influence of market factors, including industry risks |

1. Narrowing of the market due to a decrease in demand for the products manufactured by the enterprise (sold goods, services rendered) or the entry of large companies into the market offering dumping conditions. 2. Change in the profile of the company's main activity due to negative changes in the market for manufactured products (sold goods, services rendered, work performed). 3. Narrowing of the range of manufactured products as a result of negative market trends. 4. Decrease in the share of manufactured products (sold goods, rendered services) in the total volume of the market (market segment) due to the deterioration of the competitive position. 5. Change in production/sales volumes under the influence of the seasonality factor. 6. Other factors identified during monitoring |

| 3 | Assessment of changes in the influence of non-market factors |

The main non-market factors are the following: 1) initiation of legal or administrative proceedings against the borrower and / or persons who provided security under the transaction, the consequence of which may be the alienation of a significant part of the property or the reduction / suspension of the main activity of the borrower (the persons who provided security under the transaction); 2) seizure of property and/or accounts of the borrower or persons who provided security for the transaction, encumbrance of their property, inconsistent with the bank; 3) the presence of overdue obligations for payments to the budget and extra-budgetary funds, as well as for the payment of wages to employees of the enterprise or violation of the conditions for restructuring debt to the budget and extra-budgetary funds (tax credit); 4) other negative factors identified during the monitoring process |

| 4 | Assessment of changes in the structure and quality of management |

1. The appearance of negative changes in the business reputation of business owners and / or its main managers. 2. The presence of conflicts between business owners and / or its main managers. 3. Changes in the composition of business owners, exit from their structure of large foreign and domestic companies, banks and financial groups, resulting in changes in the main type of activity, conditions for the supply / sale of raw materials, goods, works (services). 4. Change of key managers, resulting in a deterioration in the results of the company's core business. 5. Other factors identified during monitoring |

| 5 | Assessment of changes in credit history |

1. Obtaining information on non-fulfillment / improper fulfillment of obligations on credit products provided by other servicing banks (loans provided by other creditors). 2. Availability of information on the repayment of debts to other banks by providing property of the borrower or persons who provided security for the transaction as a release. 3. Other factors identified during monitoring |

| 6 | Assessment of changes in financial condition |

Monitoring of the financial condition is carried out in accordance with the requirements of this document. During monitoring, special attention is paid to the following factors: 1) the emerging trend of deterioration in the financial condition, expressed in a decrease in solvency, financial stability, net asset value, the ratio of borrowed and own funds; 2) the presence of a trend towards a decrease in business activity, including a decrease in sales volumes and turnovers on accounts, not related to the influence of the seasonality factor; 3) an increase in the average turnover time of total assets while accelerating the turnover of accounts payable; 4) decrease in profitability indicators of the enterprise, its sustainable unprofitable activity, not provided for by the feasibility study provided at the stage of consideration of the loan application (business plan, financial plan); 5) an increase in the volume of off-balance sheet obligations (guarantees, pledges, avals of bills issued to secure the obligations of third parties); 6) other factors identified during the monitoring process |

| 7 | Assessing the safety of the provided collateral | Identification of facts of depreciation, loss, non-compliance with storage conditions, replacement of the provided security not agreed with the bank, expiration of the insurance contract and its non-renewal for a new period |

| 8 | Evaluation of the implementation of the feasibility study (business plan, financial plan) | Identification of losses not provided for by the submitted feasibility study (business plan, financial plan), non-compliance with the planned volumes of production and / or sales, increase in total liabilities, including attraction of unplanned sources of financing for core and / or investment activities, direction of financing for purposes not provided for Feasibility study for the deal |

| 9 | Country risk assessment (used for enterprises engaged in export / import operations, other activities abroad) | The solvency of a foreign counterparty and its impact on a possible deterioration in the financial condition of an enterprise is assessed by an expert |

Monthly monitoring of financial condition

The analysis algorithm can be represented as follows:

Revenue research;

Study of receivables and payables, identification of problem debts;

Research of stocks, financial investments, loans and credits;

Analysis of turnover in banks and the borrower's cash flow plan;

Monitoring the state of collateral.

As features of the monthly monitoring, the following can be noted.

With regard to receivables, accounts payable, stocks, financial investments, loans and credits, the analysis is carried out similarly to quarterly monitoring, however, the basis for the analysis is not financial statements, but balance sheets for accounting accounts.

As part of the study of receivables and payables, turnover and balance sheets are requested for accounts 60, 62, 76 for a certain period, broken down by counterparties, or a breakdown of receivables or payables for a specific date, indicating the overdue. The objectives of debt analysis are:

Comparison of receivables and payables with reporting data or data of the previous month and identification of trends;

Identification of changes in the structure of debt and the reasons for its change;

Identification of overdue debts (can be indirectly found by identifying debtors and creditors for which the debt is growing or has not changed for a long time);

Identification of affiliated companies in the debt structure, determination of a possible change in the scheme of work or forms of settlements with counterparties.

As part of the study of stocks, balance sheets are requested for accounts 10, 20, 41, 43, etc.

The objectives of stock analysis are:

Comparison of various elements of stocks with reported data or data of the previous month and identification of trends;

Identification of the structure of reserves and the reasons for its change;

Comparison of the dynamics of stocks with the dynamics of receivables and payables, as well as revenue;

Determination of possible overstocking and illiquid stocks.

As part of the analysis of revenue, either a VAT declaration (reflects quarterly revenue) or a balance sheet for account 90-1 for a certain period, as well as certificates of revenue in kind, are requested. When analyzing revenue, the focus is on:

The structure of revenue by type of product and its comparison with previous periods;

The dynamics of revenue and its comparison with previous periods.

In addition, when studying revenue, it is important to take into account seasonality, as well as the characteristics of the company's production cycle.

It is very important to analyze the turnover in banks within the framework of monthly monitoring for the following reasons:

According to RAS, revenue is recognized by shipment, so the analysis of turnover in banks allows you to evaluate the cash flow;

The certificates of servicing banks should contain information on the presence of a file of unpaid documents, which makes it possible to identify potential problems of the borrower;

Also, the certificates should contain information on loans issued by banks, which allows you to verify the specified information with accounting data and assess the credit burden.

Usually, as part of the study of turnover in banks, the following are requested:

Certificate of the IFTS on open bank accounts;

Information about turnover, card file and availability of loans, off-balance sheet liabilities.

Registration of monitoring results. Working with bad debts

The monitoring results are drawn up in the form of an analytical note, which usually contains the following information:

Name of the borrower, type of loan product and transaction parameters;

Industry of the borrower, a brief analysis of market and non-market factors;

Conclusions based on the results of vertical and horizontal analysis of the balance sheet and income statement;

Conclusions based on the results of the analysis of liquidity, financial stability, business activity and profitability;

Analysis of sales proceeds;

Analysis of receivables, accounts payable, financial investments, stocks, loans and credits;

Analysis of turnover in banks;

Analysis of the order portfolio and the borrower's cash flow plan;

Conclusions on the results of collateral monitoring;

A general conclusion about the change in risk for a particular transaction/borrower.

Factors that may indicate the emergence of potential problems with the borrower:

A sharp decrease in revenue and receipts to settlement accounts;

Increase in inventories and work in progress;

Growth of receivables, growth of overdue debts;

Growth of accounts payable, including overdue;

Loan portfolio growth;

Availability of card files for accounts;

Presentation of requirements of tax authorities;

Claims by third parties;

Falling demand for products;

The presence of predictable cash gaps without additional financing, etc.

In the event of a potentially problematic debt, you must:

Negotiate with the borrower, guarantors, mortgagors for loans;

Understand the causes of potential problems;

Understand the need for loan restructuring;

Find a mutually acceptable restructuring solution.

Basic rules of behavior of the creditor in case of overdue debt:

Correctness;

persistence;

Focus on finding a mutually acceptable solution;

Compliance with the law.

In conclusion, it should be noted that credit institutions need to restructure their work in relation to assessing the financial condition of existing borrowers by deepening and increasing the frequency of analysis. The proposed approaches to building an in-depth monitoring system will help not only to correctly assess the financial condition for the purposes of reserving, but also to immediately respond to the occurrence of financial difficulties for borrowers.

R.V. Ulyanov, NOMOS-BANK (OJSC), loan officer, Ph.D.

Assumptions and problems

For the creditor bank, the financial solvency of the borrower is important insofar as he expects to receive back the amount issued as a loan and interest on it in time. Such viability of the borrower is expressed in its solvency and creditworthiness.

Solvency is the ability (possibility) and willingness (desire) of a legal or natural person to repay their monetary obligations (debts) in a timely manner and in full. In contrast, creditworthiness is the ability and willingness of a person to repay their credit debts (principal and interest) in a timely manner and in full. Creditworthiness is a narrower concept than solvency. In order to decide to issue a loan to a given borrower, it is enough for the bank to be convinced of its creditworthiness, it is not necessary to consider the issue in a broader sense (although it is clear from the correlation of concepts that the solvency of the borrower also implies that he has the ability to pay for the loan).

There is another difference between the concepts under consideration. The borrower must repay his ordinary financial obligations (except for credit ones), as a rule, at the expense of proceeds from the sale of his products (works, services). As for credit debt, in addition to the above, it has three more sources of repayment (though not always reliable): 1) proceeds from the sale of property accepted by the bank as collateral for a loan, 2) guarantee (surety) of another bank or other person; 3 ) insurance indemnities.Consequently, a bank that competently gives loans can count on their full or at least partial reimbursement even in the case when the borrower turns out to be insolvent in the usual sense of the word 1 .

The lending activity of Russian banks, along with other circumstances, is complicated by the lack of a well-established methodology for assessing creditworthiness in most of them and the insufficiency of the information base for a full-fledged analysis.

1 In this chapter, the creditworthiness of borrowers is considered in relation to short-term and partly medium-term lending (current creditworthiness). The ability of an enterprise to receive, use and repay in a timely manner, in accordance with the terms of the agreement, a medium- and long-term loan for investment purposes (investment creditworthiness) is a special ability and a separate problem, which will be considered in Ch. 21.

Lease of the financial condition of clients. Most medium and small banks do not have a proper analytical apparatus at all and do not maintain contact with special information, analytical and consulting services, the information of which can help to more accurately assess the creditworthiness of borrowers.

In assessing the creditworthiness of borrowers, two big questions actually need to be answered:

1. How to assess the prospective financial solvency of the borrower (ie how to make sure that he will have the ability to meet his monetary obligations under the loan by the time the loan agreement expires)?

2. How to assess how ready he is to fulfill these obligations (ie, whether he wants to do this, can he be trusted)?

To adequately assess the borrower's creditworthiness means to reasonably, conclusively answer both of these questions.

The solution of both issues is possible only if the bank employees have the opportunity to obtain the information necessary for analysis and are able to correctly process and interpret it.

Studying the creditworthiness of potential borrowers is associated with significant difficulties.

In our country, it is still difficult to obtain meaningful financial and other information about the borrower (the available financial and statistical reporting does not always allow for a detailed and in-depth analysis of the financial position of the borrower), especially since such information does not yet have a representative historical retrospective in terms of working in conditions market. However, it is important that bank staff constantly and actively seek adequate data.

Creditworthiness depends on many factors. And this fact in itself means difficulties, since each factor (for a bank - a risk factor) must be evaluated and calculated. Added to this is the need to determine the relative "weight" of each individual factor for the state of creditworthiness, which is also extremely difficult.