How to make vat correctly in 1s 8.3. Accounting info. Purchase of goods by import

Step 1. Preparing a VAT declaration in 1C 8.3

Before you start filling out the VAT declaration in 1C 8.3, you should definitely check whether all primary documents have been included in the program. This is about:

- Current account documents - statements;

- Cash transactions - cash orders;

- Waybills and invoices for the arrival and sale of goods.

After making sure that all documents are correctly and timely entered into the 1C 8.3 program, it is recommended to close the period for editing for employees who work with primary documents and start the process of preparing a declaration.

Step 2. Generation of the report Availability of invoices

At the second stage, you need to check that all supplier invoices entered into the 1C 8.3 program are correct, that is, if VAT is highlighted in the invoice or act, then it is also highlighted in the invoice. To do this, in the 1C 8.3 program there is a report Availability of invoices located on the Reports tab:

The report can be configured for various options: Yes, No, Doesn't matter. If the Doesn't matter option is configured, the report will show both the presence and absence of invoices:

Also, the report can be generated in the context of documents, through the Settings button in this document:

When generating a report, the 1C 8.3 program informs that, for example, there is no invoice for position 18, if there is a document Receipt:

The example shows that the invoice is not registered for this document. To eliminate the error in 1C 8.3, open the Receipt document (act, invoice) by clicking on its name, and enter the supplier's invoice. Then click the Register button:

After entering the invoice, it is recommended to repost the Receipt document and its subordinate documents:

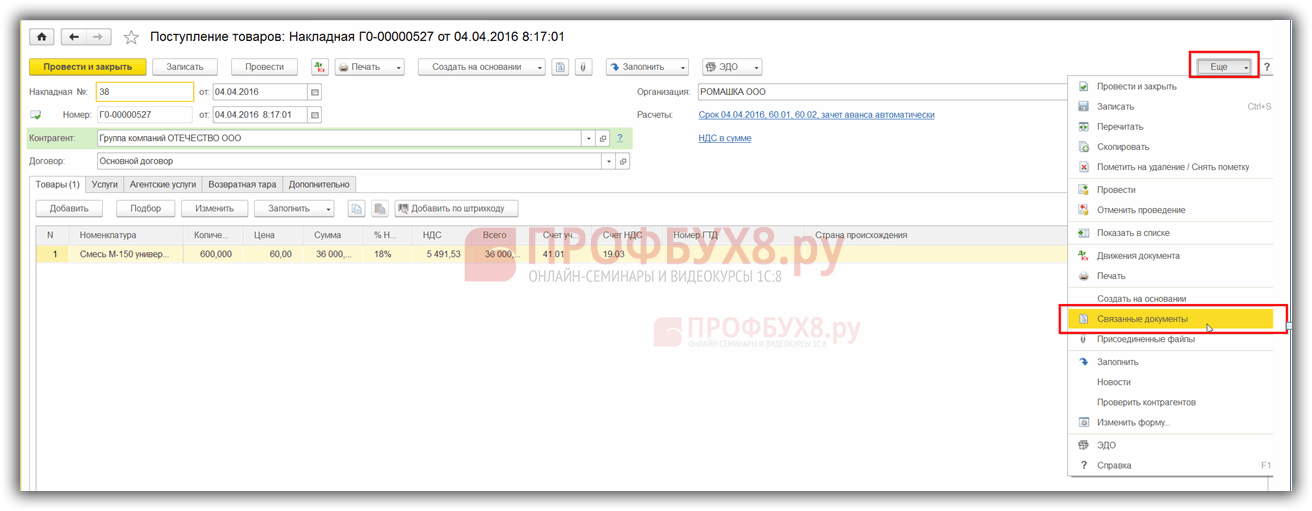

We will find related documents by clicking the More button:

By clicking on the Related Documents, we will see all the documents that need to be re-posted:

Then we again generate the Report on the presence of invoices and see that the invoice is present:

If a point is not marked in the Posted column, then you need to go to the indicated invoice and repost it. Then re-generate the report.

How to work with the report on the presence of invoices in 1C 8.2 (8.3) is also discussed in our video tutorial:

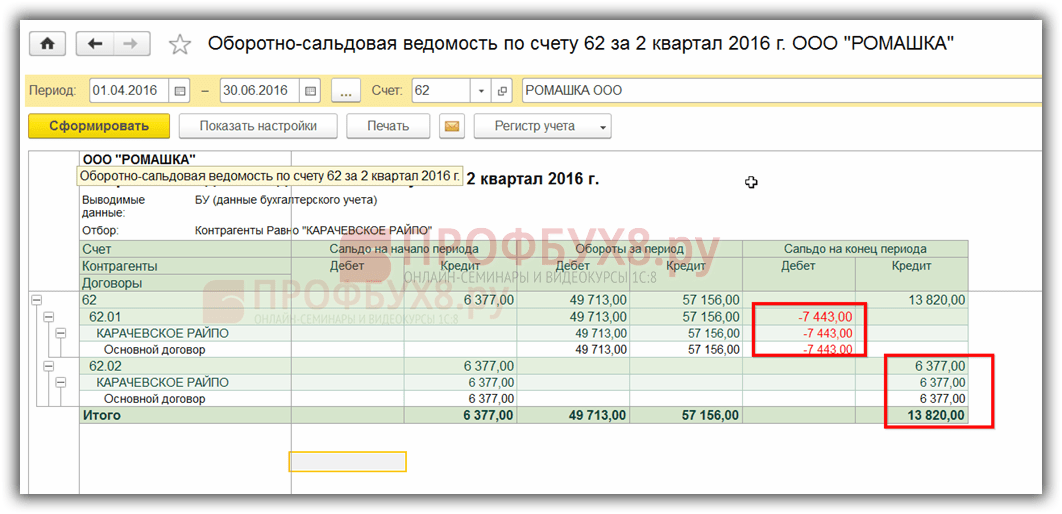

Step 3. Check accounts for settlements with counterparties

To identify a credit balance for account 62.01 and a debit balance for account 62.02:

This situation may arise if the document is incorrectly specified in the document Implementation of the account of advances or the method of offsetting advances.

To eliminate the error, open this document and put down the correct settlement accounts. After that, you need to repost the sales document and the payment document:

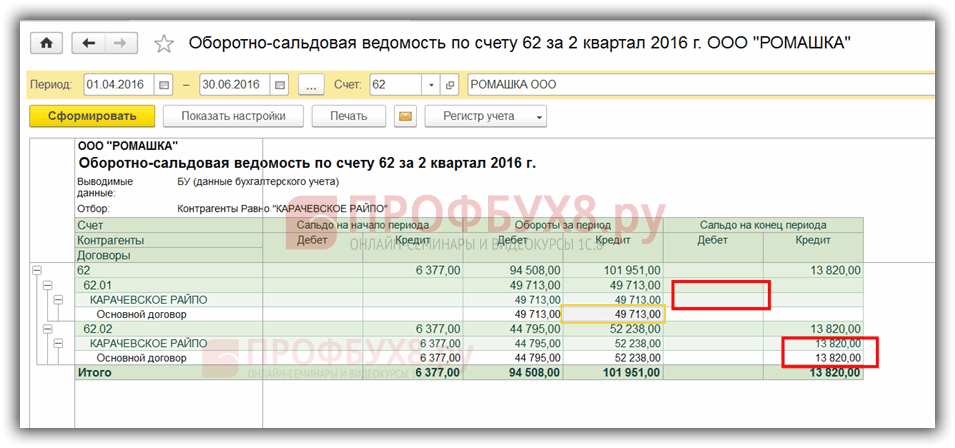

Again, we form the SAL and see that the balance in the context of sub-accounts is formed correctly:

Step 4. Assistant for VAT accounting

When you open the Assistant, the 1C 8.3 program suggests taking specific actions in stages if errors are detected. As operations are performed, they will be highlighted in green and marked with a check mark:

If necessary, documents should be cross-checked again. For example, if during the preliminary check, changes and corrections were made to documents.

Then, step by step, we perform the actions specified in the document:

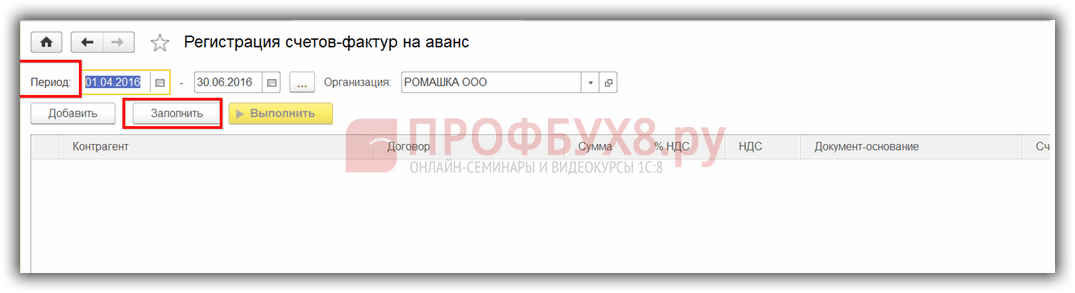

- We carry out an operation to register invoices for advance payment. Set the period and click the Fill button:

After filling out, we press the Execute button and the document is posted according to VAT registers:

We carry out the same procedure in the following stages:

- Formation of records of the Sales Book;

- Formation of records of the Purchase Book.

When filling in these registers automatically, all tabs in these documents will be filled in.

If you need to fill in only one specific tab, then you need to use the Fill button, and not the Fill document button:

Then, to check the correctness of the formation of the Purchase Book, we make SALT on account 19 in a section, that is, separately for each sub-account. There is no balance on sub-accounts, except for account 19.07 “VAT on goods sold at the rate of 0% (export)”. On account 19.07, the balance should only be debit:

To check the correctness of the accrual of advances, you should check:

- Accrued amounts according to the formula, forming "" 60.02 and 76AB;

- Turnovers Дт 62.02 * 18/118 should be equal to the turnover according to Кт account 75АВ and vice versa, according to advances "spent";

- Also check the correctness of VAT charged on sales. If there is no sale at a rate of 0% or non-taxable, you can check it using the formula: Turnover on account CT 90.01.1 * 18% / 118% \u003d turnover on account Dt 90.03 VAT accrued.

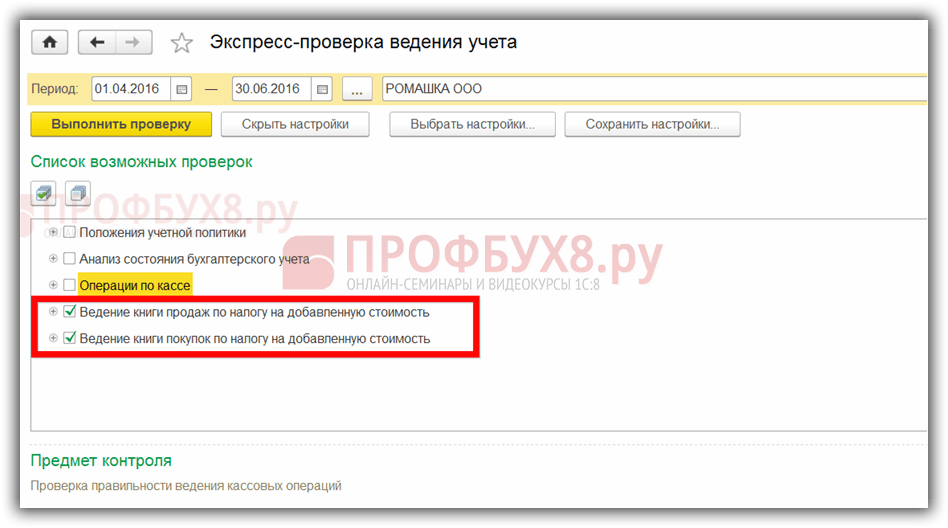

Step 5. Express check of accounting

The final stage in the preparation of the VAT declaration in 1C 8.3 is the launch of the accounting procedure:

General principles of working with the report Express check of accounting in 1C 8.3 Accounting revision 3.0 are considered in

Using the Settings button, select the setting for this report in 1C 8.3:

In our case, it is necessary to check the filling of the Purchase Book and the Sales Book:

We set the required period and selection criteria for verification:

If all the registers in 1C 8.3 are filled in correctly, the report will give the record "No errors found". If errors are detected, you must follow the prompts that are spelled out in the report. By clicking on the "-" button, a menu of errors opens and in the Recommendations field it is written how to correct errors.

In our case, we see that no invoices have been issued for sales documents. By clicking on the document Implementation, we open the primary document, issue an invoice, and post it. We fix all the errors indicated in the report in the same way. After correcting all the errors, we generate the report again:

After correction, you need to re-generate the report again. If no errors are found, then you can proceed to filling out the declaration.

How to carry out an Express check of VAT in 1C 8.3, how to avoid technical errors in VAT. What to do with the requirement to submit explanations to the Federal Tax Service, and how to verify VAT with counterparties in 1C 8.3 is discussed in the following video tutorial:

Step 6. Filling in the VAT declaration in 1C 8.3

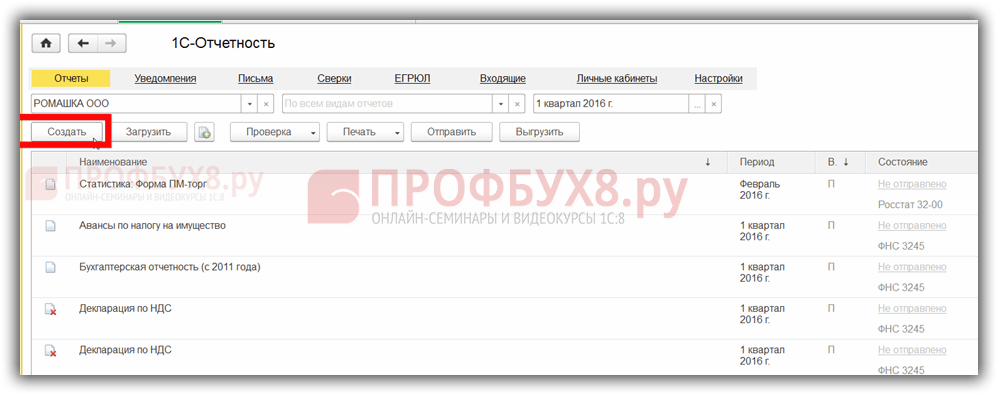

Go to the Regulated reports menu:

We choose to create a new report:

Click the Create button and select the VAT declaration in the menu that opens:

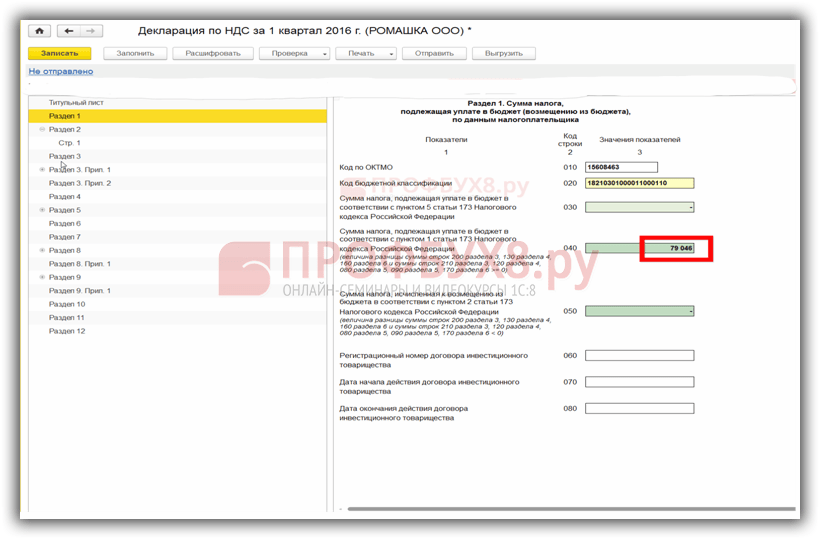

We fill in all the required details, which are highlighted in the figure below. Click the Fill button. After that, in 1C 8.3, the VAT declaration is automatically filled in:

Step 7. Checking the correctness of filling out the declaration in 1C 8.3

To check the correctness of the formation of the declaration in 1C 8.3, you should check the control calculated figures:

The total VAT amounts in the Purchase and Sales Book are equal to the turnovers according to the Account Analysis 68.02 report. To generate this report, go to the Reports menu, select Account Analysis, open. We make the necessary settings: set the period and add the By subaccounts parameter:

We form a report and compare the data with the declaration. By Dt account - Purchase book, by CT account - Sales book. The data coincide, therefore, the VAT declaration in 1C 8.3 is filled out correctly:

Step 8. Unloading the VAT declaration from 1C 8.3

Before unloading the declaration from the 1C 8.3 database for delivery via electronic communication channels, you should check the completion of the declaration so that the IFTS accepts the declaration. To do this, there is a Check button on the panel for filling out the declaration:

It is imperative to check the declaration before unloading it from the 1C 8.3 database. Checking in 1C 8.3 can be carried out according to various parameters. The dialog box displays comments after checking. You can use the bug navigator to fix them.

After correcting errors, you should re-form the declaration in 1C 8.3 and once again click the Check button for the selected parameters. After the message “No errors” appears in the dialog box, you can send the declaration to the IFTS.

Rate this article:

In 1C 8.3 configurations, there are several ways to generate a VAT declaration:

- From the general list of regulated reports (workplace "1C-regulated reporting")

- From the VAT Assistant

- From the directory ""

- From the document "Regulated reports"

Reporting from 1C

The general list of regulated reports is called from the "Reports" section, the "Regulated reports" subsection (Fig. 1).

This option is convenient in that it contains all the regulated reports generated by the user at once (Fig. 2), including various options. In addition, various services are connected here for sending, monitoring and reconciliation with the tax authorities.

The second, no less convenient option for forming a VAT declaration is the use (Fig. 3).

The assistant panel sequentially lists all the actions that need to be performed before generating the declaration (Fig. 4), as well as their state. The operation that needs to be performed at the current moment is marked with an arrow.

In our example, this is "". Operations that do not require correction are marked in bright type, pale type - a signal of possible errors. The declaration itself is displayed in the last paragraph.

Get 267 1C video tutorials for free:

All forms of regulated reports are stored in the 1C database in a special directory - "Regulated reports" (Fig. 5). This is where the latest printed versions will be written after the new release is installed.

From this panel, you can get detailed information about each report, including legislative changes. You can get to this window from the general list of directories (button "All functions"). You can create a declaration by clicking the "New" button, highlighting the required line with the cursor.

If the reference book "Regulated reports" contains actual printable forms of reports, then the reports with the data themselves are stored in the document of the same name (Fig. 6). You can get into the document from the general list of documents by clicking the "All functions" button. From this panel, you can open the declaration without the start form. You can also see the upload log here.

Checking VAT accounting in the database

VAT is a complex tax; for its correct calculation, special features are provided in 1C configurations. The VAT accounting assistant has already been mentioned above. In addition to it, it is worth using the processing "" and "Analysis of VAT accounting" (Fig. 7).

Express check contains sections on VAT accounting with a list of errors and tips for correcting them (Fig. 8).

The processing "Analysis of VAT accounting" verifies the correctness of filling in the purchase book, sales book and VAT declaration after all regulatory VAT transactions (Fig. 9).

In this article we will talk about VAT recovery and the reflection of this operation in 1C 8.3 using the example of the configuration of 1C Enterprise Accounting.

Often the term itself "VAT recovery" raises questions. Let's try to explain it. In short, then recovery is the reverse operation deduction for VAT, i.e. on the deduction already received once, an adjustment is made, reducing this deduction or completely canceling it. If someone will understand more, then theoretically we can say that we will reverse the VAT deduction in whole or in part, depending on the situation. But that's just the term "Storno" in this case does not apply, but they say that “VAT should be restored”.

In more detail, when materials, goods, fixed assets, etc. arrive. input VAT is often a tax deduction that reduces the amount of tax payable during the period of receipt. In order to apply such a deduction, several conditions must be met, for example:

- Correctly issued SF;

- The received values \u200b\u200bare used in activities subject to VAT;

- The recipient of the valuables is a VAT payer, etc.

Now let's imagine a situation when at the moment of posting values \u200b\u200ball these conditions were met and the deduction was accepted. After a while, the conditions changed, and it turned out that the deduction could not be used. In this case, VAT recovery is done.

Another option when it is necessary to recover VAT is prepayment to the supplier by the buyer. By making an advance payment, the buyer can use the VAT deduction, forming a posting 68. VAT - 76.ВА in the accounting. When the buyer receives a shipment for such an advance, he will make a deduction on the received items with a VAT posting of 68. VAT - 19. Then it turns out that there will be two deductions for one shipment. This situation is impossible, therefore the first deduction must be restored.

The list of situations when VAT should be restored is given in the Tax Code, art. 170 item 3. And although the practice of court decisions suggests that this list is closed, nevertheless, tax authorities often require VAT to be restored in other cases, for example, in case of theft of property. Here the enterprise itself must decide whether to restore the tax or not (in this case, it cannot do without court hearings).

Since the restoration of VAT always leads to an increase in the amount of tax payable, there will always be 68.VAT in the CT transactions, and there are options for Dt, depending on the situation. Such operations should be reflected in Shopping Book.

Let's consider the most common cases of VAT recovery.

VAT recovery on the example of 1C: Accounting configuration

Now from theory to practice. Let's consider two options on how to reflect VAT recovery in 1C Accounting.

Example 1. The most frequent case of VAT recovery. The buyer made an advance payment for the consignment, both contractors are VAT payers. Prepayment amount RUB 118,000, incl. VAT 18000. A few days after the prepayment, the organization received material values \u200b\u200bin the amount of 94,400 rubles, incl. VAT 14,400 rubles

Accounting for advance payments in 1C is well automated. Correct transactions were automatically generated for payment.

If at this moment to form Shopping book, we will have two deductions for one delivery.

VAT recovery should be carried out. For this in the menu Operations select item

It offers to re-post documents and form routine operations - formation of records of the purchase and sales ledger.

We are interested Press the button Complete the document, the tabular section will be generated automatically.

We look at the wiring. The program automatically recovers VAT by analyzing the amount of the advance and subsequent shipment. In our case, the delivery is less than the advance payments paid, we recover the amount equal to the shipment received from the supplier.

Example 2. In the 4th quarter, according to the received batch of materials from example 1, VAT should be restored from the amount of 40,000 rubles, the estimated amount of VAT is 7200 rubles.

In this case, the program cannot automatically determine in which period and volume the VAT should be restored. Therefore, we create an appropriate document VAT recovery. It's in the section

Push the button Create, select a document for VAT recovery from the list of options.

To ensure that VAT does not "hang" on account 19, it must be written off. You can create a document based on a receipt.

By default, the entire receipt amount is proposed for adjustment, we should adjust it.

On a bookmark Debit account we indicate the account 91.02.

Pay attention to the meaning of the reference book of expenses. Here you can set the parameter, whether expenses are included in expenses for the purpose of calculating income tax or not.

If accepted, the postings will be as follows:

Another common example that many businesses may encounter is a change in the delivery amount due to price adjustments and (or) the number of items shipped, as a result of which there may be a need to recover VAT. Such operations lead to the appearance of corrective invoices, the order of reflection of which we will consider in detail in another article.

We continue a series of lessons on working with VAT in 1C: Accounting 8.3 (revision 3.0). We will look at simple examples of accounting in practice.

Most of the material will be designed for novice accountants, but experienced ones will also find something for themselves.

I remind you that this is a lesson, so you can safely repeat my actions in your database (preferably a copy or a training one).

So let's get started.

Situation for accounting

We (VAT payer)01.01.2016 bought chair behind 11800 rubles (including VAT 1800 rubles)

05.01.2016 sold chair behind 25000 rubles (including VAT 3813.56 rubles)

Required:

- add documents to the database

- form a shopping book

- create a sales book

- fill in the VAT return for the 1st quarter of 2016

We will do all this together, and along the way, I will draw your attention to the details you need to know in order to understand the behavior of the program.

We enter the purchase

We go to the section "Purchases", item "Receipt":We create a new document for the receipt of goods and services:

We fill it in in accordance with our data:

When creating a new item, do not forget to specify the 18% VAT rate on its card:

This is for convenience - it will be automatically inserted into all documents.

We also draw attention to the item "VAT from above" highlighted in the document picture:

When you click on it, a dialog appears in which we can specify the method of calculating VAT in the document (above or in total):

Here we can set the checkbox "VAT included in the cost", if you want to make the input VAT part of the cost (attributed to 41 accounts instead of 19).

We leave everything by default (as in the picture).

We post the document and look at the resulting transactions (DtKt button):

Everything is logical:

- 10,000 rubles went to the prime cost (debit 41 accounts) in correspondence with our debt to the supplier (credit 60).

- 1,800 rubles went to the so-called "input" VAT, which we will take into account (debit 19) in correspondence with our debt to the supplier (credit 60).

Total after these postings:

- The cost of goods (debit 41) - 10,000 rubles.

- Incoming VAT for offset (debit 19) - 1,800 rubles.

- Our debt to the supplier (loan 60) is 11,800 rubles.

This seems to be all, since often accountants, out of habit, pay attention only to the bookmark with accounting entries.

But I want to tell you right away that for the “troika” (as well as for the “two”) this approach cannot be considered sufficient. And that's why.

1C: Accounting 3.0, in addition to accounting entries, also makes entries in the so-called registers. It is on the records in these registers that she is guided in her work.

The book of income and expenses, the book of purchases and sales, certificates, declarations for reporting ... almost everything (except for such reports as Account Analysis, SALT, etc.), she fills out precisely on the basis of registers, and not at all accounting accounts ...

Therefore, it is simply vital for us to gradually learn to "see" the movements in these registers in order to better understand and, when necessary, correct the behavior of the program.

So, go to the register tab “ VAT Billed»:

The income from this register accumulates our input VAT (similar to writing to debit 19 of the account).

Let's check - have we met all the conditions in order for this receipt to be reflected in the purchase book?

To do this, go to the "Reports" section and select the "Purchase book" item:

We form it for the 1st quarter of 2016:

And we see that it is completely empty.

And the thing is that we did not register the invoice received from the supplier. Let's do this, and at the same time see what movements along the registers (along with the transactions) she makes.

To do this, go back to the receipt document and fill in the number and date of the invoice from the supplier in its lower part, then click the "Register" button:

Pay attention to the checkbox "Reflect VAT deduction in the purchase book by date of receipt". It is this jackdaw that is responsible for the appearance of our receipt in the purchase book:

Let's see the transactions and movements in the registers of the received invoice (DtKt button):

Postings are quite expected:

- We subtract the input VAT from credit 19 of account in debit 68.02. By this operation, we reduce our own VAT payable.

Total after this operation:

- By 19.03 the remainder is 0.

- By 68.02 - a debit balance of 1800 (the state owes us at the moment).

And now the most interesting thing, consider the registers (over time, you need to learn them all along with the chart of accounts).

Register " VAT charged"- our old friend:

Only this time the entry was made as an expense. By doing this, we took away the incoming vat, similarly to credit 19 accounts.

And here is a new register for us " VAT Purchases»:

You probably already guessed that it is the entry for this register that is responsible for getting into the purchase book.

Book of purchases

Trying to rebuild the buy book for the 1st quarter:

And voila! Our receipt got into this book and all thanks to the entry in the register "VAT Purchases".

About invoice journal

By the way, we have not considered the third register "Journal of accounting of invoices". A record has been made on it, but let's try to form this very log.To do this, go to the "Reports" section, "Invoice journal":

We form this magazine for the 1st quarter of 2016 and .. we see that the magazine is empty.

Why? After all, we have entered the invoice and the entry in the register has been made. And the thing is that since 2015, the register of received and issued invoices has been kept only when carrying out entrepreneurial activities in the interests of another person on the basis of intermediary agreements (for example, commission trade).

Our texture does not fall under this definition, and therefore it does not get into the magazine.

Making the implementation

We go to the section "Sales" item "Sale (acts, invoices"):

We create a document for the sale of goods and services:

We fill it in according to the task:

And again, we immediately draw attention to the highlighted item "VAT in total".

We post the document and look at the postings and movements in registers (DtKt button):

Accounting entries are expected:

- We wrote off the cost of the chair (10,000 rubles) on credit 41 and immediately reflected it at debit 90.02 (cost of sales).

- They reflected the proceeds (25,000 rubles) on credit 90.01 and immediately reflected the buyer's debt to us on debit 62.

- Finally, we reflected our debt on VAT in the amount of 3813 rubles 56 kopecks to the state on credit 68.02 in correspondence with debit 90.03 (value added tax).

And if we now look at the analysis of 68.02, we will see:

- 1,800 rubles on debit is our input VAT (from the receipt of goods).

- 3,813 rubles and 56 kopecks on the loan are our outgoing VAT (from the sale of goods).

- Well, the credit balance of 2013 rubles and 56 kopecks is the amount that we will have to transfer to the budget for the 1st quarter of 2016.

Everything is clear with the wiring. Let's move on to registers.

Register " VAT Sales"Is completely similar to the register" VAT Purchases "with the only difference that the entry into it ensures that the sale gets into the sales book:

Let's check it out.

Sales book

We go to the "Reports" section, the "Sales Book" item:

We form it for the 1st quarter of 2016 and see our implementation:

Wonderful.

The next stage on the way to the formation of a VAT return.

Analysis of VAT accounting

We go to the section "Reports" item "Analysis of VAT accounting":

We form it for 1 quarter and very clearly see all charges (outgoing VAT) and deductions (incoming VAT):

VAT payable is immediately displayed. All values \u200b\u200bare decipherable.

For example, let's double-click the left mouse button on the implementation:

Report has opened ...

In which, by the way, we see our mistake - we forgot to issue an invoice for implementation.

Let's fix this defect. To do this, go to the implementation document and at the very bottom press the "Issue an invoice" button:

VAT Assistant

Now go to the section "Operations" item "Assistant for VAT accounting":

We form it for the 1st quarter of 2016:

Here, in order, it is described the points that you need to go through to form a correct VAT return.

First, let's repost the documents for each month:

This is necessary in case we entered documents retroactively.

We skip the formation of the purchase book entries, because for our simplest case, they simply will not exist.

And finally, click on the item "VAT return".

Declaration

The declaration has opened.There are many sections here. We will only cover the main points.

First of all, in section 1, the final amount to be paid to the budget was filled in:

Section 3 shows the tax calculation itself (outgoing and incoming VAT):

Section 8 contains information from the purchase book:

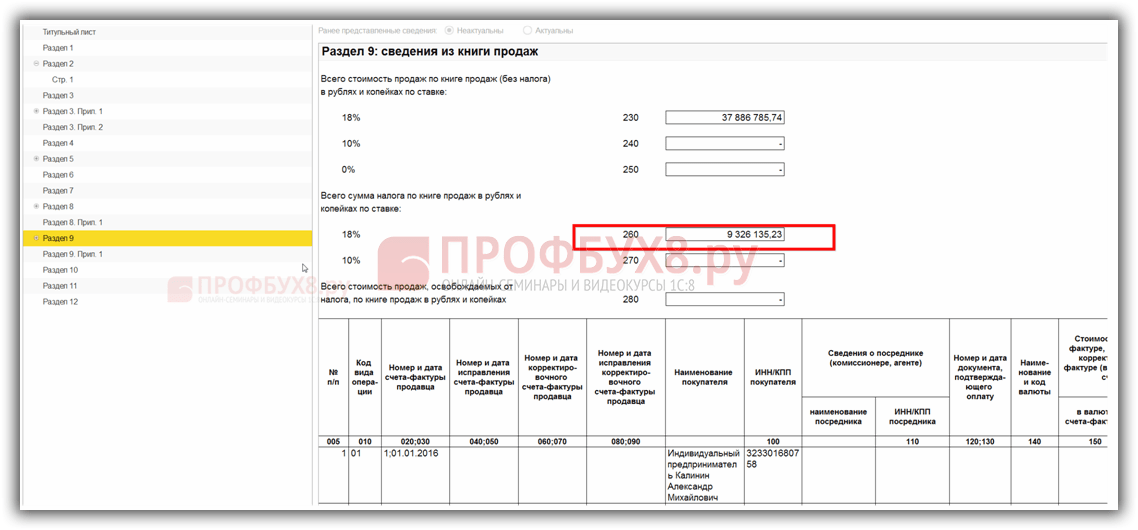

Section 9 contains information from the sales book:

We just have to fill in the title page and other required fields, and then upload the declaration electronically.

In this lesson, I tried to show, so to speak, the general train of thought of an accountant when forming VAT in 1C: Accounting 8.3 (revision 3.0).

At the same time, I focused our attention on the registers, the movements in which are formed by the program along with accounting entries. We will gradually learn these registers, their knowledge will allow us to more accurately understand the behavior of the program.

Briefly

Goods receipt- Dt 41 Kt 60 10000 [goods (cost price) arrived from the supplier]

- Dt 19.03 Kt 60 1800 [incoming vat (deducted) from the supplier]

- Coming by register " VAT charged»1800

- Dt 68.02 Kt 19.03 1800 [set off the incoming vat]

- Consumption by register " VAT charged»1800

- Recording to register " VAT Purchases»1800

- Recording to register " Invoice journal»

- Dt 90.02 CT 41 10000 [wrote off the cost of goods sold]

- Dt 62 Kt 90.01 25,000 [recorded revenue]

- Dt 90.03 Kt 68.02 3813.56 [accrued vat payable]

- Recording to register " VAT Sales"3813.56

- Recording to register " Invoice journal»

- We collect input VAT on debit.

- On the loan, read off the collected VAT to debit 68.02.

- On the loan, we charge the outgoing VAT payable.

- On debit we read off VAT collected on the account 19.03.

- We transfer to the budget the difference between credit and debit, that is, the credit balance.

We are great, that's all.

In this article, we will take a step-by-step look at how VAT is reflected when purchasing any goods, and checking it for the correctness of the previously entered data.

The very first document in the chain for reflecting VAT in 1C 8.3 in our case will be.

The organization OOO "Konfetprom" acquired 6 different nomenclature items on the basis of "Products". For each of them, the VAT rate is 18%. The received amount of this tax is also reflected here.

After the document was completed, movements were formed in two registers: "Accounting and tax accounting", as well as the accumulation register "VAT presented". As a result, the amount of VAT on all items amounted to 1306.4 rubles.

After we have conducted the purchase document for goods from the "Products" database, it is necessary. To do this, enter its number and date in the appropriate fields. After that, you need to click on the "Register" button.

All data in the created invoice was filled in automatically. Please note that in our case the flag "Reflect VAT deduction on the date of receipt" is set. Otherwise, taxes will be taken into account when forming purchase book entries with a document of the same name.

After carrying out our invoice, it created movements in all the necessary registers in the amount of 1306.4 rubles.

Data validation

Despite the fact that the program calculates and generates most of the data automatically, errors are not excluded.

Of course, you can manually check the data in the registers by setting the appropriate filters, but you can also use a special report. It's called Express Check.

In the form that opens, we will indicate that we need to verify the data on the organization of OOO Konfetprom for July 2017. You can specify any period, not necessarily within a month.

In the picture above, you can see that in some sections the last column is highlighted in red. The number of errors found is also written there.

In our example, you can see that the program found an error in maintaining the value added tax purchase ledger. When disclosing groupings, we may receive additional information due to errors.

VAT adjustment

When working with 1C Accounting 8.3, it is not uncommon for you to change the receipt document "retroactively". For this, a receipt correction happens, which is created on the basis of it.

By default, the document is already complete. Please note that we will be recovering VAT in the sales ledger. This is evidenced by the corresponding flag on the "Main" tab.

Let's go to the "Products" tab and indicate what changes should be made to the initial receipt. In our case, the number of purchased assorted candies changed from four to five kilograms. We entered this data in the second line "after the change", as shown in the image below.

The correction of the receipt, as well as the initial receipt itself, made movements in two registers, reflecting only the changes made in them.

Due to the fact that a kilogram of Assorti sweets costs 450 rubles, VAT on it was 81 rubles (18%). It is these data that are reflected in the movements of the document.