What operations can be performed using a corporate card. Corporate cards: calculations and accounting. List of documents for issuing corporate cards using a special card account

Bank card products are not only intended for individuals. Legal entities and individual entrepreneurs can use corporate cards for their activities, which are linked to a current account.

How cards are taken into account in accounting, necessary transactions, methods of using the product, current offers from banks in 2019.

CC is required to carry out normal financial transactions: purchase of goods, inventories, fuels and lubricants, payment of expenses and services, entertainment expenses, etc. This is a modern way of providing funds for reporting, an alternative to using a checkbook.

The use in calculations is convenient; they simplify transactions and make them more mobile.

Advantages of corporate cards:

- operating expenses are reduced: the client does not need to withdraw funds from the current account, account for cash, make transactions for issuing money on account, other expenses are reduced (for withdrawing cash through the bank’s cash desk);

- the ability to replenish your account through Internet banking and ATMs;

- the ability to control and limit the funds provided to the employee: funds are transferred to the card in a certain amount; when a transaction is completed, the client is notified by SMS;

- there are no restrictions on the limit of cash payments in the amount of 100 thousand rubles;

- You can use the product around the clock;

- the ability to make transactions via the Internet;

- receiving benefits and bonuses from the bank’s partner companies;

- a company can open a credit card when it lacks its own working capital.

Transactions are carried out non-cash, so their safety and security is ensured. Users can use cards when they are abroad, which frees them from opening a foreign currency account or filing declarations.

The number of cards linked to one current account is determined by the bank, and the limit on card payments is set by the head of the company.

Bank programs

Today, many banks offer the use of CC, since funds in the current accounts of legal entities are not insured by the DIA, you should choose a credit institution from the most reliable:

| Bank | Program |

| Sberbank | Business card |

| Alfa Bank | International corporate cards |

| VTB | International bank cards |

| Vanguard | Corporate cards |

| Promsvyazbank | Bank cards for legal entities and individual entrepreneurs |

| Rosselkhozbank | Corporate bank cards |

1 Sberbank

The Sberbank corporate card provides round-the-clock access to the account:

Service parameters:

- the first year of service is free if the client is connected to the “Easy Start” package;

- unlimited number of cards to one current account;

- standard service 2500 rub. in year;

- commission for depositing funds to the card is 0.3%, a maximum of 100 thousand rubles can be topped up per day;

- withdrawal fee is 1.4–3%, the maximum you can withdraw per day is 170 thousand rubles. from each card, per month up to 5 million rubles;

- SMS notification 60 rubles/month;

- grace period for a corporate credit card is 50 days.

The client independently limits the limits on the card account: for cash withdrawals, for the amount of transactions on the account within 1 day and 1 month, the total limit for the card.

2 Alfa Bank

Alfa Bank offers clients to use international corporate cards:

Three types of cards are offered:

- International corporate Visa FIFA card – the client participates in the FIFA bank loyalty program

- International corporate cards VISA International – a chip card with an increased level of security.

- International corporate cards MasterCard Worldwide

Account currency is rubles, dollars, euros.

Service parameters:

- Free issue, monthly service cost RUR 299;

- Visa Business Gold cards are free within any service package;

- Alpha Check option – 59 rubles/month;

- Commission for withdrawing cash using a corporate card is 1.5%, for depositing cash 0.4%;

- The daily limit for cash withdrawal is 150–450 thousand rubles, per month 750–1500 thousand rubles. depending on the type of card;

- The number of cards is not limited;

- It is possible to connect an overdraft, the debt period is up to 60 days, the contract term is up to a year, if the client has high solvency, he can have an interest-free period of up to 30 days, the terms of the loan are set individually.

Account control is carried out from the Alfa-Client Online Internet bank and the Alfa-Business Mobile mobile bank.

3 VTB

The credit institution offers corporate cards to simplify expenses:

Designed for medium-sized businesses. Two card packages are offered: Business Classic, Business Gold. Card categories Business, Gold, Platinum.

Options:

- monthly service from 1200 to 2400 rub. depending on the class of corporate card;

- the number of cards is unlimited, valid for 2 years;

- possibility of automatic replenishment of the card account;

- for the gold package: concierge services, connection of insurance programs;

- commission for cash withdrawal is 1%, withdrawal limit is 300–600 thousand rubles;

- The maximum deposit amount per day is 100 thousand rubles. via ATM.

Business cards are international, so their privileges extend to business trips abroad.

4 Bank Avangard

The bank presents a personalized corporate card of the international payment system:

Options:

- account currency rub.;

- Card validity is 3 years;

- the number of cards for one account is not limited;

- the minimum balance on the account is 10 thousand rubles;

- annual fee for making payments 600–1000 rubles;

- cash withdrawal fee 3–10% depending on the amount;

- There is no commission for replenishing an account through bank ATMs, in other cases 0.3%%

It is convenient to transfer travel and other expenses to the card and use it abroad. Officials can use cash registers with one-time passwords and sign documents in online banking and mobile banking.

5 Promsvyazbank

The bank offers clients with a current account in the campaign business cards:

Options:

- free card issue;

- validity period 4 years;

- account currency: rubles, dollars, euros;

- cash withdrawal limit 300–500 thousand rubles/day, 3–7 million rubles/month;

- account replenishment limit 500 thousand rubles/day;

- Any payments on a business card are 0 rubles.

The card can be used to pay suppliers, purchase household goods, and pay travel expenses.

6 Rosselkhozbank

The credit company issues corporate cards for legal entities, individual entrepreneurs, and individuals engaged in self-employment:

The account currency is ruble. There are two types of VISA Business MasterCard Business cards available.

Product parameters are determined by the “Corporate” tariff plan:

- validity period 1 year;

- maintenance 2 thousand rubles;

- commission for cash withdrawals at bank branches is 1% of the amount, at ATMs 2%;

- you can withdraw 300 thousand rubles per day, 500 thousand rubles per month;

- It is prohibited to replenish the account with cash;

- crediting to the account is free;

- Transactions are carried out free of charge.

No more than 1 CC can be issued for each holder.

To use banking CC in production activities, the company must develop a Regulation on the use of cards and familiarize authorized employees with it against signature.

It establishes a list of operations that can be carried out using the card, the positions of persons to whom cards can be provided, limits, responsibilities, etc. are determined.

Based on Art. 9 Federal Law No. 402, primary accounting documents are developed:

The list of transactions that can be performed using a bank card is determined by the Card Issue Regulations No. 266-P.

The issuance of the CC is not reflected in the accounting accounts. Card accounting is carried out through a specialized 1C program. Corporate card account number 55.

Transactions on corporate cards:

Write-offs are reflected by posting Dt. account 71 Kt. sch. 55 (for ruble transactions). Next from the account. 71 funds are written off for their intended purpose: settlements with suppliers, with various debtors and creditors, general production expenses, etc.

Funds received: Dt. Account 55, Kt. 51.

Transactions on foreign currency corporate cards are recorded in the appropriate accounting accounts.

How to use a corporate card

A corporate card is issued at the bank where the current account of the company or individual entrepreneur is opened.

Opening methods:

- Contact the representative office of the credit institution at the place where the current account is serviced;

- Write an application via Internet banking.

The application indicates the account currency, the type of card product, and information about the authorized person for whom the card is registered.

After the bank makes a decision to provide the service, the cards are produced within 3–7 days and handed over to the client.

When opening a corporate credit card or setting an overdraft limit on an account, the client must submit to the bank the company’s financial statements, operational data, depending on the limit, determine the collateral, etc. Lending parameters are determined by banks individually for clients.

After receiving the cards and completing the necessary documents, they are handed over to authorized employees for work. The list of employees is approved by a separate order. The issuance of a card to an employee is formalized by an acceptance certificate confirming the fact of receipt of the document.

Responsibility for spending funds on the card lies with its holder within the established limit. He is obliged to promptly report on transactions made on the account, otherwise, expenses on the card may be deducted from his salary. The reporting procedure, timing, and form are determined by the management of the enterprise or the individual entrepreneur.

To record the movement of corporate cards, the enterprise must have a Journal. It records the issuance and return of cards by the employee against signature.

Answers on questions

Is it possible to top up a corporate card account from an individual’s card account at Sberbank?

This service is not provided by the credit institution.

How to cancel a corporate card?

If the company does not wish to use the service, an authorized employee must submit an application to the bank to terminate it.

The application shall indicate: number of cards, service agreement number, current account number, card details, full name. holders.

What to do if you lose your corporate card?

If your corporate card is lost or stolen, it should be blocked quickly. This is done through mobile banking by calling the Customer Support Center hotline. After blocking, the client must come to the bank and write a statement with the reason for blocking. The card will be reissued for a fee.

Conclusion

Bank corporate cards will completely replace check books in the near future. Corresponding amendments to accounting are made at the legislative level. It will be convenient for credit institutions to control the spending of funds by clients; existing limits on withdrawals will limit the use of cash in settlements between organizations.

Companies will receive a convenient tool for carrying out transactions, but difficulties may arise due to the lack of a sufficient number of self-service devices, the possibility of blocking cards, and the fact that cards are not yet accepted for payments everywhere.

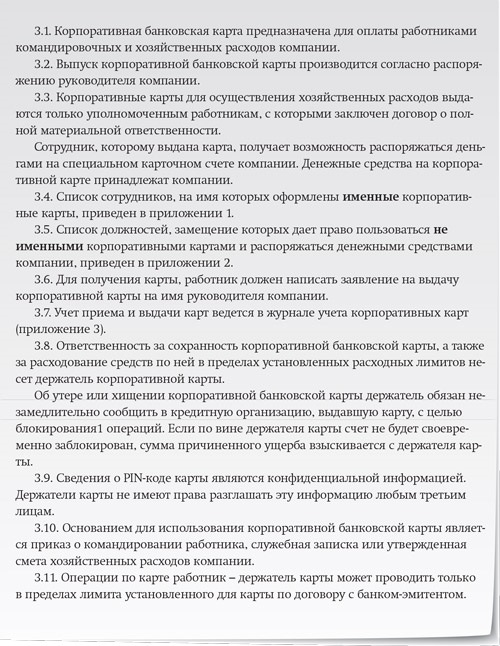

1. List of expenses and transactions that can be made by an employee of an organization using a corporate card owned by the organization

The use of corporate cards in the business activities of any organization is very convenient and every year the number of organizations using them in their activities increases.

In order to use a corporate bank card in an organization, it is advisable to issue a regulation on the use of such a banking product, which will establish a list of positions of employees who have the right to use this card, payment limits on this card, as well as a list of expenses that each employee can make using this cards, liability for its loss and other operations necessary for control.

To eliminate possible disputes with employees, it is necessary in accordance with Part 2 of Art. 22 of the Labor Code of the Russian Federation, familiarize all employees who have the right to use this card with signature.

To record the movement of corporate cards, it is necessary to develop and approve forms of primary documents on the basis of which the acceptance and issuance of corporate bank cards will be recorded (Article 9 of the Federal Law of December 6, 2011 N 402-FZ “On Accounting”, hereinafter referred to as Law N 402 -FZ).

In the accounting policy, it is advisable to prescribe the method of accounting for accountable amounts in a special account (clause 7 of PBU 1/2008), as well as the accounting methodology, which will be discussed in this article

The list of expenses that can be included in expenses that reduce the tax base is determined according to general rules in accordance with the provisions of Art. 252 of the Tax Code of the Russian Federation (TC RF).

For accounting of transactions with corporate bank cards, accounts 51 “Current account” or 55 “Other bank accounts” are used. The write-off of funds from a bank card is reflected by a posting to the credit of account 51 “Current account” or 55 “Other bank accounts” in correspondence with the debit of the accounts for accounting for settlements or expenses, depending on the economic event reflected in the accounting records.

The list of transactions that can be performed by an individual using a bank card is established in the Regulations on the issuance of payment cards and on transactions performed with their use (approved by the Bank of Russia on December 24, 2004 N 266-P) (as amended on August 10, 2012) (Registered in the Ministry of Justice of Russia 03/25/2005 N 6431) (hereinafter referred to as Regulation N 266-P).

According to clause 2.3 of the said Regulations, an individual client carries out the following operations using a bank card:

- receiving cash in the currency of the Russian Federation or foreign currency on the territory of the Russian Federation;

- receiving cash in foreign currency outside the territory of the Russian Federation;

- payment for goods (work, services, results of intellectual activity) in the currency of the Russian Federation on the territory of the Russian Federation, as well as in foreign currency outside the territory of the Russian Federation;

- other transactions in the currency of the Russian Federation, in respect of which the legislation of the Russian Federation does not establish a prohibition (restriction) on their execution;

- other transactions in foreign currency in compliance with the requirements of the currency legislation of the Russian Federation.

A client - an individual can carry out, using payment (debit) cards, credit cards, the operations specified in this paragraph on bank accounts opened in the currency of the Russian Federation and (or) on bank accounts opened in foreign currency.

The client, an individual who is a resident, can carry out the operations specified in this paragraph using credit cards at the expense of the provided loan in the currency of the Russian Federation without using a bank account.

The use of a prepaid card by an individual client is carried out in accordance with the requirements of Federal Law of the Russian Federation N 161-FZ of June 27, 2011 N 161-FZ “On the National Payment System” (hereinafter referred to as Federal Law of the Russian Federation N 161-FZ) at the expense of the balance of electronic funds in the currency of the Russian Federation and (or) in foreign currency.

A client - an individual who is a non-resident, can carry out the operations specified in this paragraph using credit cards at the expense of the provided loan in the currency of the Russian Federation, foreign currency without using a bank account.

According to clause 2.4 of the said Regulation N 266-P, clients - individuals using payment (debit) cards, credit cards can carry out transactions in a currency other than the account currency, the currency of the loan provided, in the manner and on the terms established in the bank account agreement , loan agreement. Clients - individuals using prepaid cards can make electronic money transfers in a currency different from the currency of the electronic money balance. When performing the operations specified in this paragraph, the currency received by the issuing credit institution as a result of a conversion operation is transferred for its intended purpose without being credited to the account of the client - an individual.

According to clause 2.5 of Regulation N 266-P, the client - a legal entity, an individual entrepreneur, carries out the following operations using payment (debit) cards, credit cards:

- receiving cash in the currency of the Russian Federation for making payments on the territory of the Russian Federation, in accordance with the procedure established by the Bank of Russia, related to the activities of a legal entity or individual entrepreneur, including payment of travel and entertainment expenses;

- payment of expenses in the currency of the Russian Federation related to the activities of a legal entity, individual entrepreneur, including payment of travel and entertainment expenses, on the territory of the Russian Federation;

- other transactions in the currency of the Russian Federation on the territory of the Russian Federation, in respect of which the legislation of the Russian Federation, including regulations of the Bank of Russia, does not establish a ban (restriction) on their execution;

- receiving cash in foreign currency outside the territory of the Russian Federation to pay for travel and hospitality expenses;

- payment of travel and hospitality expenses in foreign currency outside the territory of the Russian Federation;

- other transactions in foreign currency in compliance with the requirements of the currency legislation of the Russian Federation.

A client - a legal entity, an individual entrepreneur can carry out, using payment (debit) cards, credit cards, the operations specified in this paragraph on bank accounts opened in the currency of the Russian Federation, and (or) on bank accounts opened in foreign currency.

The issuing credit organization is obliged to determine the maximum amount of cash in the currency of the Russian Federation that can be issued to a client - a legal entity or individual entrepreneur during one business day for the purposes specified in this paragraph. The issuing credit organization is recommended to establish for a client - legal entity, individual entrepreneur - the possibility of receiving cash in the currency of the Russian Federation for the purposes specified in this paragraph in an amount not exceeding 100,000 rubles during one business day.

The client is a legal entity, individual entrepreneur, using prepaid cards, transfers electronic funds, returns the balance of electronic funds in accordance with the requirements of Federal Law N 161-FZ.

According to clause 2.6 of the said Regulations, clients - legal entities, individual entrepreneurs using payment (debit) cards, credit cards can carry out transactions in a currency other than the currency of the account of a legal entity, individual entrepreneur, in the manner and on the terms established in the bank account agreement . When performing the operations specified in this paragraph, the currency received by the issuing credit institution as a result of a conversion operation is transferred for its intended purpose without being credited to the account of the client - a legal entity, an individual entrepreneur. Clients - legal entities and individual entrepreneurs using prepaid cards can make electronic money transfers in a currency different from the currency of the electronic money balance.

According to clause 2.7 of Regulation N 266-P, in the event of absence or insufficiency of funds in the bank account when the client performs transactions using a settlement (debit) card, the client, within the limit provided for in the bank account agreement, may be provided with an overdraft to carry out this settlement transaction if there is a corresponding condition in the bank account agreement.

According to clause 2.8 of Regulation N 266-P, credit institutions, when issuing payment (debit) cards and credit cards, may provide in a bank account agreement or loan agreement a condition for the client to carry out transactions using card data, the amount of which exceeds:

- the balance of funds in the client’s bank account if the conditions for providing an overdraft are not included in the bank account agreement;

- overdraft limit;

- the limit of the loan provided, defined in the loan agreement.

Settlements for these operations can be carried out by providing the client with a loan in the manner and on the terms provided for by the bank account agreement or loan agreement, taking into account the norms of these Regulations.

If there is no bank account in the agreement, and in the loan agreement there are no conditions for granting a loan to the client for these operations, the client’s repayment of the debt incurred is carried out in accordance with the legislation of the Russian Federation.

In accordance with paragraphs. b clause 1 part 1 art. 9 of the Law of the Russian Federation dated December 10, 2003 N 173-FZ) currency of the Russian Federation - funds in bank accounts. Foreign currency - banknotes in the form of banknotes, treasury notes, coins that are in circulation and are legal means of cash payment on the territory of the corresponding foreign state (group of foreign states) - paragraphs. and clause 2, part 1, art. 9 of the Law of the Russian Federation dated December 10, 2003 N 173-FZ.

Foreign currency is a type of currency value (clause 5) of Part 1 of Art. 9 of the Law of the Russian Federation dated December 10, 2003 N 173-FZ).

Alienation by a resident in favor of a non-resident of currency valuables, the currency of the Russian Federation on legal grounds, as well as the use of currency valuables, the currency of the Russian Federation as a means of payment is a currency transaction (subclause b, clause 9, part 1, article 9 of the Law of the Russian Federation dated December 10, 2003 N 173- Federal Law).

Based on this, payment with a corporate card in foreign currency is a foreign currency transaction; therefore, to reflect this operation in accounting, it is necessary to apply PBU 3/2006 “Accounting for assets and liabilities, the value of which is expressed in foreign currency” (hereinafter referred to as PBU 3/2006 ).

PBU 3/2006 establishes the specifics of the formation in accounting and financial statements of information on assets and liabilities, the value of which is expressed in foreign currency, including those payable in rubles, by organizations that are legal entities under the legislation of the Russian Federation (with the exception of credit organizations and state ( municipal institutions) - clause 1 of PBU 3/2006.

We offer a list of possible card transactions in Table No. 1.

Table No. 1. List of possible operations on the card.

2. Payment of travel expenses by employees of the organization in foreign currency on the territory of Russia and abroad using ruble corporate cards. Accounting Features

As mentioned above, it is allowed to pay travel and entertainment expenses in foreign currency outside the Russian Federation using a corporate card issued both in the currency of the Russian Federation and in foreign currency (clause 2.5 of Regulation No. 266-P).

Based on the norms of clause 5.2 of the Instruction of the Central Bank of the Russian Federation dated 04.06.2012 N 138-I “On the procedure for the submission by residents and non-residents to authorized banks of documents and information related to foreign exchange transactions, the procedure for issuing passports of transactions, as well as the procedure for accounting by authorized banks of foreign exchange transactions and control over their implementation" (hereinafter referred to as Instruction No. 138-I), when a resident carries out a foreign exchange transaction under a transaction (contract, loan agreement), the amount of obligations under which does not exceed the equivalent of 50 thousand US dollars, associated with the write-off of Russian currency from the current account resident in the currency of the Russian Federation, a transaction passport is not prepared.

Clause 3.1 of Instruction N 138-I establishes that a resident, when carrying out a currency transaction related to the debiting of Russian currency from his current account in Russian currency opened with an authorized bank, submits to the authorized bank at the same time the following documents: an order for the transfer of funds provided for by the regulatory an act of the Bank of Russia regulating the rules for transferring funds (hereinafter referred to as the settlement document for a currency transaction); documents related to the currency transaction specified in the settlement document for the currency transaction.

At the same time, clause 3.3 of Instruction No. 138-I, a settlement document for a currency transaction is not drawn up and is not submitted by the resident to the authorized bank when the resident carries out currency transactions using bank cards.

Based on the above, a resident, when carrying out foreign exchange transactions in the currency of the Russian Federation using bank cards, submits to the authorized bank documents related to the currency transaction without drawing up and submitting a settlement document for the currency transaction. At the same time, the deadline for submitting to the bank documents related to conducting currency transactions using bank cards is not directly provided for by Instruction No. 138-I. In our opinion, such a period should be agreed upon with the authorized bank before the commencement of foreign exchange transactions. We also recommend agreeing on the list of documents submitted to the bank (for example, invoices, acts confirming expenses made by employees).

If payment from a ruble corporate card occurs on the territory of the Russian Federation, there are no special features of accounting and tax accounting.

To correctly reflect in tax and accounting transactions for payment from a ruble corporate card outside the territory of the Russian Federation of any expenses, it is necessary to answer several questions.

- Is it necessary to record the conversion of rubles into other currencies in accounting?

- When does ownership of currency values pass to the organization: at the moment an employee receives currency from an ATM or at the time he makes a currency payment from a card?

- Do exchange rate differences arise in accounting for settlements with an accountable person?

In our opinion, ownership of currency values passes to the organization at the moment its employee receives currency from an ATM from a ruble corporate card (or at the time he makes a foreign currency payment from a ruble corporate card).

First, ownership of the currency passes to the organization, and then the organization issues the currency to its employee.

This conclusion is justified as follows.

According to Art. 30 of the Federal Law of December 2, 1990 N 395-1 “On Banks and Banking Activities”, relations between credit institutions and their clients are carried out on the basis of contracts.

According to paragraph 1 of Art. 845 of the Civil Code of the Russian Federation, under a bank account agreement, the bank undertakes to accept and credit funds received to the account opened for the client (account owner), carry out the client’s orders to transfer and withdraw the corresponding amounts from the account and carry out other operations on the account.

The agreement on the use of a bank account was concluded with a legal entity, therefore all relations regarding the agreement (withdrawal of money from the account, conversion of funds, etc.) take place between the bank and the legal entity. The corporate card is linked to the account and is actually only a means of payment.

According to the provisions of Art. 140 of the Civil Code of the Russian Federation, the ruble is legal tender, obligatory for acceptance at face value throughout the Russian Federation.

At the same time, currency values - foreign currency and external securities have a different legal regime (in particular, they are not a means of payment on the territory of Russia with some exceptions) in accordance with the provisions of the articles of the Federal Law of December 10, 2003 N 173-FZ “On Currency Regulation and Currency Control” "

Thus, rubles and currency are different objects of civil rights, including having different valuations in different periods of time. In this case, this difference must also be reflected in accounting and tax accounting.

In clause 2.6 of the Regulations on the issuance of payment cards and on transactions performed with their use, approved. The Bank of Russia on December 24, 2004 N 266-P (Registered with the Ministry of Justice of Russia on March 25, 2005 N 6431) established that clients - legal entities using payment (debit) cards, credit cards can carry out transactions in a currency different from the currency of the legal entity’s account in in the manner and on the terms established in the bank account agreement. When carrying out these operations, the currency received by the issuing credit institution as a result of a conversion operation is transferred for its intended purpose without being credited to the account of the client - a legal entity.

However, this does not mean that a business transaction involving currency conversion was not carried out. According to the provisions of Art. 9 of the Federal Law of December 6, 2011 N 402-FZ “On Accounting”, each fact of economic life is subject to registration as a primary accounting document. And it must be reflected in accounting.

It should be noted that when using ruble corporate cards of an organization, it is necessary to take into account that the commercial rate of the servicing bank used when converting currency, as a rule, differs significantly from the official rate of the Central Bank of the Russian Federation, which will be an additional expense for the organization. An organization has the right to take into account such costs as non-operating expenses when calculating income tax on the basis of paragraphs. 6 clause 1 art. 265 of the Tax Code of the Russian Federation.

Also, for carrying out conversion operations on behalf of the client, the bank may withhold a fee if such a condition is stipulated in the bank account agreement, which provides for settlements using a debit (payment) card. This point is also important when determining whether the conversion is to be made into the account of an organization or a third party (employee).

Accounting. Basic principles and features

Accounting for transactions with corporate bank cards depends on the account to which such a card is “linked”. If the card is “linked” to one of the company’s current accounts, then payments made using it are reflected in account 51 “Current Account”. If a separate account is opened for settlements, then such an account in accounting is account 55 “Other bank accounts”.

All write-offs of funds from a corporate bank card made by authorized persons of the company (receipt of cash and non-cash payments) are reflected by a posting to the debit of account 71 “Settlements with accountable persons” and the credit of account 51 “Current account” (55 “Other bank accounts”) , in case rubles are written off.

If an employee received foreign currency from a card, then, taking into account the above regarding the one-time transfer of ownership of foreign currency assets first to the organization, and then from the organization to the accountable person, this fact of economic life must be reflected in accounting. Due to the lack of a methodology for accounting for this operation in Russian accounting standards (RAS), the method used must be fixed in the accounting policy. In our opinion, to reflect the purchase of currency, you can use a transit account, for example, account 57 with a certain identification (D57 K55) and reflection of the amount in the currency of the accountable person at the rate of the Central Bank of the Russian Federation and reflection in expenses of the difference in purchase and conversion rates (D71, 91.2 K57). The basis for this operation must be a document from the bank confirming this operation.

Next, from account 71 “Settlements with accountable persons”, funds are written off to settlement accounts (60 “Settlements with suppliers and contractors”, 76 “Settlements with various debtors and creditors”), or expense accounts (20 “Main production”, 23 “ Auxiliary production and facilities”, 25 “General production expenses”, 26 “General business expenses”, 44 “Sale expenses”), depending on the essence of the economic event and primary documents.

Considering that primary documents can be drawn up in a foreign language, it is necessary to make a line-by-line translation into Russian (clause 9 of the Regulations on accounting and financial reporting in the Russian Federation, approved by Order of the Ministry of Finance of Russia dated July 29, 1998 N 34n “On approval of the Regulations on accounting and financial reporting in the Russian Federation", Article 68 of the Constitution of the Russian Federation), which can be carried out either by a professional translator or by an employee of the organization who speaks a foreign language (letter of the Ministry of Finance of the Russian Federation dated April 20, 2012 N 03-03-06/ 1/202)

Please note the following features. As mentioned above, this operation relates to a foreign exchange operation; accordingly, the organization must apply PBU 3/2006.

In accordance with clauses 4, 5 and 6 of PBU 3/2006, in accounting, an advance issued in a currency other than the currency of the Russian Federation is accounted for in rubles at the official exchange rate of the Central Bank of the Russian Federation established on the date of issue of money from the cash register. Based on clauses 7, 9 and 10 of PBU 3/2006, the recalculation of foreign currency debt into rubles at the end of the reporting period or at the date of approval of the advance report is not carried out. That is, the expenses of the accountable person are reflected in accounting at the exchange rate of the Central Bank of the Russian Federation on the date of issue.

However, there are exceptions. If an overspending of the advance payment is identified or the advance payment has not been fully spent, then the rate of the Central Bank of the Russian Federation as of the date of approval of the advance report will be applied to these amounts.

The employee must hand over the balance of accountable amounts to the organization's cash desk within three working days after returning from abroad (clause 26 of Resolution No. 749 of October 13, 2008 “On the specifics of sending employees on business trips”). Unspent currency should be credited to the cash desk with conversion into rubles at the exchange rate on the day the employee returned the money (clause 20 of PBU 3/2006 and clause 24 of the Regulations on accounting and financial reporting in the Russian Federation, approved by Order of the Ministry of Finance of Russia dated July 29, 1998 N 34n ).

Tax accounting. Basic principles and features

A positive exchange rate difference for the purposes of tax accounting for income tax is an exchange rate difference that arises when revaluing property in the form of currency values and claims, the value of which is expressed in foreign currency, or when depreciating liabilities, the value of which is expressed in foreign currency (clause 11 of Art. 250 of the Tax Code of the Russian Federation).

A negative exchange rate difference for the purposes of tax accounting for income tax is an exchange rate difference that arises when depreciating property in the form of foreign currency assets and claims, the value of which is expressed in foreign currency, or when revaluing liabilities, the value of which is expressed in foreign currency (clause 5 p. 1 Article 265 of the Tax Code of the Russian Federation).

At the same time, the specified norms of the Tax Code of the Russian Federation exclude exchange differences arising from the revaluation of advances issued from non-operating income and expenses.

The date of travel expenses in accordance with paragraphs. 5 paragraph 7 art. 272 of the Tax Code of the Russian Federation recognizes the date of approval of the advance report.

Until the moment specified in paragraphs. 5 paragraph 7 art. 272 of the Tax Code of the Russian Federation, an enterprise must have an extract from a ruble account and bank data on currency conversion. Based on documents from the bank confirming the conversion, the difference between the Central Bank rate and the currency conversion rate in accordance with paragraphs. 6 clause 1 art. 265 of the Tax Code of the Russian Federation and paragraph 2 of Art. 250 of the Tax Code of the Russian Federation is reflected in expenses in NU.

- In accordance with paragraph 10 of Art. 272 of the Tax Code of the Russian Federation, in the case of an advance transfer, expenses (approved advance report) expressed in foreign currency are converted into rubles at the official rate established by the Central Bank of the Russian Federation on the date of transfer of the advance (the date of debiting funds from the corporate card (in the part attributable to the advance). That is, within the limits of funds debited from the card, the rate will be equal to the rate of the Central Bank of the Russian Federation on the dates of debiting funds from the card.

- If there is an overexpenditure (economically justified) of the accountable amounts, the amount of the overexpenditure in expenses will be reflected at the exchange rate of the Central Bank of the Russian Federation on the date of approval of the advance report (clause 10 of Article 272 of the Tax Code of the Russian Federation).

For an example of accounting and tax accounting for a corporate card, we provide a table with catchy figures.

Table No. 2. Accounting and tax accounting using conventional figures and conventional examples

Designed to pay expenses related to the business or core activities of the company, including overhead, entertainment, transportation and travel expenses, as well as receiving cash. The card cannot be used for payment of wages and social payments. At its core, a corporate card is an analogue of funds issued on account. Can be either debit or credit.

To issue a card, a legal entity must enter into an agreement with the bank on the issue and maintenance of corporate cards, which displays information about the employees who will use these cards. The agreement should be accompanied by employee applications for the issuance of cards and powers of attorney for them from the company. To open a card account, you must provide the relevant documents to the bank.

The possible number of cards to be opened per account is determined by each bank at its own discretion.

Advantages of using corporate cards for organizations:

Reducing operating costs and time associated with issuing accountable amounts. The company does not need to receive cash from the bank for business expenses, as well as deliver and store it;

There is no need to buy foreign currency for foreign business trips or open a foreign currency account, and there is no need to fill out declarations when crossing borders. Funds will be debited from the company's card account with automatic conversion into the currency of the country in which the cardholder is located;

Management and control of company expenses. The ability to set limits on cards and connect SMS information allows you to control the spending of funds by an authorized employee in real time. For example, an organization can top up a card at any time or increase the limit on transactions of a posted employee. The bank also provides the company with a detailed statement of transactions using cards. Due to this, the company’s accounting department can control the targeted spending of funds by employees;

Possibility to make payments in amounts over 100 thousand rubles. In accordance with the instructions of the Central Bank of the Russian Federation dated July 20, 2007 No. 1843-U, cash payments in the Russian Federation between organizations, including individual entrepreneurs, related to their business activities, within the framework of one agreement can be made in an amount not exceeding 100 thousand . rubles. Payments using a corporate card refer to non-cash payments - thus, this restriction does not apply to transactions with corporate cards;

Using the card you can make purchases on the Internet;

24/7 access to funds in the organization’s account. Possibility to receive cash from ATMs at any time;

The ability to attach all corporate cards to one card account with a single spending limit for all employees of the organization or divide all corporate cards into groups with their own spending limit;

Reduce the risk of cash loss or theft. If the card is lost, the client can block it, saving the funds;

Also, depending on the type of card and bank program, corporate cards have certain types of discounts and benefits.

Annual servicing of one corporate card in Russian banks costs on average from 1 thousand rubles. For example, at Avangard Bank, annual servicing of a MasterCard Business card costs 900 rubles, and MasterCard Gold – 2 thousand. At St. Petersburg Industrial Joint Stock Bank (SIAB), annual servicing of a Visa Business card will cost 1 thousand rubles.

Banks can set a minimum account balance on a card. So, at Avangard Bank it is equal to 10 thousand rubles.

The use of corporate cards as a means of making payments is becoming increasingly popular. This is due to the fact that such cards are a reliable and convenient way to pay expenses related to the economic activities of the organization, primarily travel and entertainment expenses. What does the process of issuing corporate cards look like in practice? What documents can be used to confirm the expenses incurred? Which authorities should I notify about the opening of a special bank account?

What is a corporate bank card?

A corporate card, like any other plastic bank card, is a personal means of payment intended for paying for goods or services, as well as for receiving cash at ATMs and banks.

The procedure for circulation of bank cards on the territory of the Russian Federation is regulated by the Regulations on the issuance of bank cards and on transactions performed using payment cards, approved by the Bank of Russia on December 24, 2004 N 266-P. It should be noted that a number of amendments were made to the text of this Regulation N 266-P by Instructions N 2862-U, which will come into force on July 1, 2013 (Instructions of the Bank of Russia dated 08/10/2012 N 2862-U “On Amendments to the Regulations Bank of Russia dated December 24, 2004 N 266-P “On the issue of bank cards and on transactions performed using payment cards” registered with the Ministry of Justice on November 21, 2012 N 25863).

Taking into account the amendments made to clause 1.5 of Regulation N 266-P, it is established that a credit institution has the right to issue bank cards of the following types: payment (debit) cards, credit cards and prepaid cards, the holders of which are individuals, including those authorized by legal entities, individual entrepreneurs.

A distinctive feature of a corporate card is that the person in whose name it is issued must be an employee of the organization who has entered into an agreement to issue such a card, while the employee receives full access to one of the accounts of the legal entity, that is, manages the organization’s funds.

An individual spending limit can be set for each card. You can set both permanent and temporary limits for spending funds on cards, specifying any period of time. In addition, when using corporate cards, you can set limits on different categories of spending: cash and non-cash payments, transactions abroad, etc.

Typically, when using corporate cards, a number of requirements and restrictions are established:

- It is not allowed to credit funds to a special card account by non-cash transfer of funds from the accounts of third parties;

- Personal expenses using corporate cards are prohibited, since all transactions carried out are reflected in the organization’s account;

- Since funds withdrawn from such a card are considered funds issued on account, appropriate reporting is required. The bank has the right to request primary documents for all transactions made using corporate cards (accommodation invoices, transport tickets, receipts, checks and other documents enclosing original receipts from electronic terminals, ATMs, as well as business trip reports if funds are debited from the account for travel expenses);

- in accordance with the requirements of the currency legislation of the Russian Federation, when carrying out transactions in foreign currency using cards, including when making cross-border payments, the organization is obliged to submit to the bank, within ten working days from the date of the transaction, a documentary justification for its completion, including a report on expenses with the attachment of settlement documents for each such operation.

What are the main advantages of working with corporate cards?

We can name a number of advantages of using corporate cards both for the organization and for the employees for whom they are issued:

- saving time, since there is no need to contact the bank to prepare documents for receiving cash from the account or depositing it into the account. Receiving money is possible at any time, both at an ATM and at the cash desk of a bank, and not necessarily the one in which the account is opened. Cash can also be deposited into an organization's account through an ATM. In addition, cards of major payment systems are accepted at most retail and service outlets, ATMs and banks in the world. The work of not only cash services, but also accounting workers is simplified, since there is no need to issue advances for travel expenses and track the return of accountable cash that was not spent on a business trip;

- reducing costs and minimizing risks associated with receiving, transporting and storing cash;

- simplifying the accounting and control of employee expenses by opening a special card account, which allows you to account for transactions on all corporate cards of the enterprise (or several special card accounts for accounting for transactions separately for each card or group of cards);

- automatic conversion of ruble funds into foreign currency when paying for services abroad.

Is it necessary to issue corporate cards to issue employees money in a non-cash form, or can you use “salary” cards?

This question often arises among employers who have implemented “salary” projects in their organizations. Let us recall that earlier in Letter No. 14-27/513 dated December 24, 2008, the Bank of Russia indicated that there are restrictions on the list of transactions performed by individuals using bank cards, in accordance with the provisions of the current legislation of the Russian Federation. At the same time, representatives of the Bank of Russia confirmed that the issue of the admissibility of reimbursement of expenses associated with business trips by transferring them to the bank accounts of individual employees opened for transactions using bank cards is within the scope of application of labor legislation. So, according to Art. 168 of the Labor Code of the Russian Federation, the procedure and amount of reimbursement of expenses related to business trips are determined by a collective agreement or local regulations.

As for the financial department, it does not object to the use of “salary” cards for settlements with accountable persons. In Letter dated 05.10.2012 N 14-03-03/728, the Ministry of Finance noted that in connection with the use of modern banking and other payment technologies, instead of issuing cash, non-cash payments are being introduced to accounts opened for these employees for payments using bank debit cards, issued by credit institutions, including within the framework of “salary” projects.

According to department officials, it is advisable to extend the scope of application of settlement (debit) bank cards (in addition to settlements for wages within the framework of “salary” projects) to settlements with accountable persons. The advantages of this form of payment, such as non-cash settlements with accountable persons using settlement (debit) bank cards, are increasing the efficiency of payment processes and automating the reconciliation of settlements and control over the receipt (credit) of funds and their use.

The rules for organizing and maintaining accounting records with accountable persons may include provisions providing for settlements with them both in cash and non-cash. As an example, the financiers cited the practice used in their department: as part of the implementation of accounting policies and taking into account the provisions of the collective agreement, the Ministry of Finance issues funds on account for travel expenses in a non-cash manner upon the application of an accountable person containing the details necessary for transfer to the account of an employee of the Ministry of Finance , opened at a credit institution, during a business trip:

- on the territory of the Russian Federation - in the currency of the Russian Federation (in rubles) using bank cards used as part of the “salary” project;

- on the territory of foreign countries - in US dollars using bank currency cards issued by credit institutions specified in the collective agreement of the Ministry of Finance.

What is the procedure for obtaining corporate cards?

As a general rule, to implement the “Corporate Card” project, an organization must, in addition to its existing bank account, open a second one specifically for payments using corporate cards. To do this you need:

- write an application to open an account;

- draw up a sample signature card;

- sign a bank account agreement for settlements of transactions using corporate cards;

- draw up an additional agreement for direct debit from the main account.

After completing all the necessary documents and opening a second current account, the organization submits to the bank:

- register for the issuance of bank cards (list of corporate card holders);

- application for issuance of a corporate card (filled out and signed by the corporate card holder and agreed upon with the head of the organization);

- orders for issuance of reports to persons specified in the register.

Note! A corporate bank card is issued directly to the holder indicated by the organization in the application for issuing a bank card, or to a client representative acting on the basis of a power of attorney executed in accordance with the requirements of the law.

What local regulations should be developed when implementing the Corporate Card project?

To carry out accounting and control of the movement of corporate cards of an organization, it is advisable to develop an appropriate regulation. It is possible not to develop a separate regulation on the procedure for using corporate cards, but in this case the procedure for their use should be prescribed in another local regulatory act, for example, in a regulation on the procedure and amount of reimbursement of travel expenses, issuance of accountable funds, submission of advance reports on travel and business expenses expenses. As an example, we can cite the Order of JSC Russian Railways dated November 7, 2006 N 2193r, which approved the Regulations on the issuance of money on account. This Regulation contains a separate section “Procedure for using a corporate bank card”, which defines:

- purpose of a corporate card;

- reasons for issuing the card;

- reasons for its use;

- the procedure and timing for submitting an advance report on funds used through a corporate bank card;

- the procedure for collecting from the guilty employee the amount used for other purposes in the absence of documents confirming the intended use of the corporate bank card;

- responsibility for the safety of the card, as well as for spending funds on it within the established spending limits.

In addition to the regulations, it is necessary to approve the register of corporate cards. This register should reflect:

- card numbers;

- FULL NAME. holders;

- dates of transfer and return of cards.

The receipt and return of a corporate card must be confirmed by the employee who received (returned) it and the person responsible for maintaining records of card data.

What is the basis for recording the amounts of transactions made using corporate cards?

Expenses are reflected on the basis of a payment register issued by the bank or an electronic journal.

Typically, funds are written off or credited for card transactions no later than the business day following the day the bank receives the payment register or electronic journal from a single settlement center (then these documents can be transferred to the organization).

Let us remind you that employees of the organization, when using the card in stores, hotels and other places of payment, receive documents confirming the expenses incurred (checks, invoices for hotel accommodation, travel tickets, receipts, invoices, etc.). Such documents must be accompanied by original slips, receipts from electronic terminals and ATMs. The employee of the organization must submit all these documents along with the advance report to the accounting department of the organization.

The mandatory details that a document on transactions using a payment card must contain are listed in clause 3.3 of Regulation N 266-P. These include:

- identifier of an ATM, electronic terminal or other technical means intended for performing transactions using payment cards;

- type of operation;

- transaction date;

- transaction amount;

- transaction currency;

- commission amount (if any);

- authorization code;

- payment card details.

The listed details must contain features that allow one to reliably establish a correspondence between the payment card details and the account of a legal entity, as well as between the identifiers of trade organizations (services), ATMs and bank accounts of trade organizations (services) (clause 3.6 of Regulations N 266-P).

For your information. A paper document on transactions using a payment card must additionally contain the signatures of the payment card holder and the cashier. This requirement does not apply to cases where the document is drawn up at a cash dispensing point using an analogue of a handwritten signature.

What to do in a situation where, when withdrawing money using a bank card, the ATM does not issue a receipt confirming the operation? It was noted above that such checks are attached by accountable persons to the advance report. But the employee himself, the accountable person, does not have the right to request the check he needs from the bank. This is due to the fact that the bank’s client is not an employee, but an organization. Therefore, the organization must contact the bank for a statement. In this case, the bank does not have the right to refuse to issue an extract (clause 2.1, section 2, part III of the Regulations on the rules of accounting in credit institutions located on the territory of the Russian Federation, approved by the Bank of Russia on July 16, 2012 N 385-P).

Is the issuance of corporate bank cards related to the withholding of personal income tax from employees and the calculation of insurance premiums?

Since the funds transferred to such cards belong to the organization, and not to the individuals using them, there are no obligations to pay personal income tax and insurance contributions (unless proven otherwise). However, all supporting documents must be properly prepared. The judges came to such conclusions, in particular, in the Resolution of the Federal Antimonopoly Service NWO dated July 18, 2011 N A05-11476/2010. The court decision noted that, according to the agreement, transactions related to the economic activities of the enterprise are carried out using cards, including the payment of travel and hospitality expenses. The arbitrators considered the claims from the tax authorities to be unfounded, since the Federal Tax Service did not audit the bank account, did not check for what purposes the funds were written off from the corporate card, and did not provide evidence that the disputed amounts were the economic benefit of the tax agent’s employees.

Which regulatory authorities must be reported about opening a bank account?

Taxpayers, both organizations and individual entrepreneurs, are required to notify the tax authority in writing about the opening or closing of accounts within seven days (clause 1, clause 2, article 23 of the Tax Code of the Russian Federation). The message form and the procedure for filling it out were approved by Order of the Federal Tax Service of Russia dated 06/09/2011 N ММВ-7-6/362@.

Also, information about opening a bank account within seven days should be submitted to the Pension Fund and the Social Insurance Fund, which are the bodies monitoring the payment of insurance premiums (clause 1, clause 3, article 28 of the Federal Law of July 24, 2009 N 212-FZ).

If a corporate card was issued in addition to an existing account and no new bank accounts were opened, then there is no need to provide information to either the tax inspectorate or the authorities monitoring the payment of insurance premiums.

Note! According to paragraph 1 of Art. 118 of the Tax Code of the Russian Federation, violation by a taxpayer of the established deadline for providing the tax authority with information about opening or closing an account in any bank entails a fine of 5,000 rubles.

12/24/2004 No. 266-P.

In order for employees to be able to freely operate corporate cards, the company must:

Develop regulations on the procedure for using corporate cards (Part 1, Article 8 of the Labor Code of the Russian Federation);

Approve the list of positions whose job duties involve the use of corporate cards in the company (clause 1 of Article 847 of the Civil Code of the Russian Federation, paragraphs 2 and 7 of clause 1.12 of Bank of Russia Instruction No. 28-I dated September 14, 2006 “On opening and closing bank accounts, deposit accounts";

Familiarize all employees whose positions are listed in the list with the position against signature (Part 2 of Article 22 of the Labor Code of the Russian Federation);

Organize in the company accounting for the acceptance and issuance of corporate bank cards (Article 9 of the Federal Law of December 6, 2011 No. 402-FZ “On Accounting”, hereinafter referred to as Law No. 402-FZ, information No. PZ-10/2012 “On entry into force from January 1, 2013, Federal Law of December 6, 2011 No. 402-FZ “On Accounting”);

Register in the accounting method for recording accountable amounts in a special account (clause 7 of PBU 1/2008).

Regulations on the procedure for using corporate cards

In this article we will assume that the company decided to open a separate special card account.

The regulation on the procedure for using corporate cards is a methodological guide for all company employees who, due to their duties, are somehow involved in this process.

In the regulations on the use of corporate cards, we recommend setting:

List of expenses and transactions that can be made by an employee using a corporate card. Please note: the list of operations that are permitted within the Russian Federation differs from the list of transactions permitted abroad. Both lists are shown in the table;

Limits on corporate cards. These may differ for different positions;

The period after which the employee must return the card;

Order by cardholders regarding amounts spent;

The period during which the employee must submit an advance report to the company with supporting documents attached;

An approximate list of documents that are accepted as confirmation of expenses incurred. You can compile an album of their samples and make it an appendix to the position. Then employees will have a visual idea of what document to require when paying by card;

Requirements for ensuring the protection of PIN code information;

Procedure in case of loss of the card;

Types of violations of order and the procedure for compensation for damage by cardholders.

List of card transactions

| Type of operation | Purpose of expenses | Territory | |

| RF | outside the Russian Federation | ||

| Cash withdrawn in rubles from a corporate card | + | - | |

| Travel and expenses | + | - | |

| Cashless payment in rubles with a corporate card | Economic activities of the company | + | - |

| + | - | ||

| Cash withdrawn from a corporate card | Economic activities of the company | - | - |

| Travel and hospitality expenses | - | + | |

| Cashless payment in foreign currency using a corporate card | Economic activities of the company | - | - |

| Travel and hospitality expenses | - | + | |

An alternative to the provision on the procedure for using corporate cards can be a separate section on the use of corporate cards in another local regulatory act of the company. This section, for example, can supplement the provision on the procedure and amount of reimbursement of travel expenses, submission of advance reports on travel and business expenses of company employees. It is shown below.

Who has the right to use corporate cards in the company

Those employees on whom these cards are issued have the right to use corporate cards. When issuing corporate cards, the company submits to the bank an approved list of company employees who have the right to use the cards.

If the head of the company decides that it is more convenient to use non-named corporate cards, he issues an order to approve a list of positions, the replacement of which gives the right to use non-named corporate cards to pay for goods and services on behalf and in the interests of the company. See below for a sample order.

When compiling a list, keep in mind that it cannot completely duplicate the staffing table. It is necessary to conduct a reasonable sample and not include positions (professions) in which the performance of official duties does not involve payment for goods and services on behalf and in the interests of the company.

Familiarize employees with the regulations for signature

All employees for whom personalized cards have been issued and whose positions are listed in the order must be familiarized, against signature, with the approved regulations on the procedure for using corporate bank cards or with the local regulatory act that contains the corresponding section.

The fact of familiarization can be recorded on the last sheet of the regulation or in a separate document (for example, in a statement or journal).

Storage, issuance and return of corporate cards

To eliminate cases of loss of corporate cards, as well as misuse or theft, the company must establish strict control over the storage and movement of corporate cards.

Personalized corporate bank cards may be in the hands of holders, provided they comply with security requirements.

As a rule, non-personal corporate cards are issued to an employee to perform a specific task - payment of travel, entertainment or other expenses.

Documentation of the transfer of a card to an employee is not regulated by law. It is better to approve this procedure in the regulations on the procedure for using corporate cards. The order may be as follows:

The employee writes an application for the issuance of a non-personal corporate card, justifying the purpose of the intended expenditure of funds;

The manager endorses the employee’s application and indicates the limit of the non-personalized card. A sample application form is given below.

Please note: there are no exceptions in the law for the situation when the accountable person is the head of the company. But the company has the right to independently rank the conditions for using corporate cards by position.

Corporate cards are issued for a period determined by the regulations. A card can be issued for a longer period, different from that specified in the company regulations, on the basis of an order from the head of the company.

If an employee constantly travels on business trips, by separate order of the manager, he can be issued a corporate card for a longer period.

If the deadline for returning a non-named corporate card is missed, the person authorized to control their movement must inform the main person about this. Then a decision is made to block the card or another decision with the guilty accountable person.

Journal of corporate card movement

The date, period, purpose of issuing a corporate card, its number, limit, position and surname of the employee are recorded in the journal for registering the acceptance and issuance of cards (the journal for the movement of corporate bank cards).

The facts of receipt and return of a corporate card by an employee must be confirmed by signatures in the journal of the accountable person and the accounting employee who is responsible for their storage.

See below for a sample log.

How to report money spent

The procedure for reporting by employees on the expenditure of funds on a corporate card is not established by a separate regulatory act. But the company can develop it independently, based on the rules governing the procedure for reporting the expenditure of cash accountable amounts.

The deadline for submitting an advance report on the use of funds from a corporate bank card can be set in the regulations on the procedure for using corporate cards. It can be set in working days from the date of expiration of the period allotted for the execution of the order or return from a business trip.

You can use the unified advance report form No. AO-1, approved by Decree of the State Statistics Committee of Russia dated August 1, 2001 No. 55.

The company also has the right to develop its own, taking into account the peculiarities associated with the combination of spending cash and non-cash funds (clause 4 of article 9 of Law No. 402-FZ).

Please draw the attention of your accountable persons to one feature of drawing up an advance report on the expenditure of funds from a corporate card.

The receipt that an employee receives when withdrawing cash from an ATM cannot in itself be considered as a document confirming the employee's expenses.

The advance report must be accompanied by receipts (other documents) indicating the intended use of the cash withdrawn from the card. The employee must deposit the balance of unused cash withdrawn from the card into the company cash desk. The employee's advance report must be approved by the head of the company.