Property tax. Reference information on rates and benefits for property taxes Kemerovo Questions on tax rates

Personal property tax is a tax paid by owners of apartments and other real estate

The tax paid in the city of Moscow goes to the city budget and, along with the receipts of other taxes, ensures the fulfillment of the city's obligations in the field of social support for citizens, improving housing conditions, providing quality healthcare, education, implementing urban development measures, etc.

In the city of Moscow, this tax is regulated by the Tax Code of the Russian Federation and the Law of the City of Moscow "On the tax on property of individuals".

residential building;

garage or parking place;

TAX RATES IN MOSCOW

|

tax rate |

|

|

up to 10 million rubles |

|

|

from 10 to 20 million rubles. |

|

|

from 20 to 50 million rubles. |

|

|

from 50 to 300 million rubles. |

For garages and parking spaces - 0.1%.

For unfinished private residential buildings - 0.3%.

1.2% on tax for 2015 (payable in 2016);

1.3% tax for 2016 (payable in 2017);

1.4% on tax for 2017 (payable in 2018);

1.5% tax for 2018 and subsequent years (payable in 2019 and beyond).

For any real estate with a cadastral value of more than 300 million rubles. – 2%.

For other non-residential real estate (for example, a warehouse, an industrial building) - 0.5%.

TAX DEDUCTION

The tax deduction provides that the following are not taxed:

50 sq.m if you own a residential building;

20 sq.m if you own an apartment;

10 sqm if you own the room.

One tax deduction is provided for each property, it does not depend on the number of owners and whether the owners belong to a privileged category.

The cadastral value of the property in the tax notice you receive by mail with the tax receipt will already be reduced by the cadastral value of the tax deduction.

Example: in an apartment of 60 sq. m are taxed only 40 sq. m.

For more information about the tax deduction, see Section 7 of the Frequently Asked Questions.

FORMULA FOR CALCULATION OF TAX

TAX AMOUNT FOR 2015 = (Ksr * S - H2014) * K + H2014

CSR = cadastral st-t, taking into account the tax deduction = cadastral st-t - (cadastral st-t / area of the object) * the amount of the deduction;

C - tax rate;

K - reduction coefficient (when calculating the tax for 2015, the coefficient is 0.2).

H2014 - the amount of tax for 2014 (determined according to the tax calculation rules in force until 2015);

If you bought or sold property during the year, the tax will only be calculated for the number of months you own or have owned the property.

For more information about tax calculation features, see Section 5 of Frequently Asked Questions.

WHEN SHOULD YOU PAY TAX?

When do I need to pay Personal Property Tax (NIFL)?

THE TAX IS PAYED ONCE A YEAR.

THE TAX AUTHORITIES SEND THE NOTIFICATION FOR THE PAYMENT OF TAX FOR THE CURRENT YEAR BEFORE NOVEMBER 1 OF THE NEXT YEAR. TAX FOR THE CURRENT YEAR MUST BE PAYED BEFORE DECEMBER 1 OF THE NEXT YEAR.

Example: A tax notice for 2015 will be sent to you by November 1, 2016. Tax for 2015 must be paid by December 1, 2016.

For more information about the terms and possibilities of paying tax, see Section 8 of the Frequently Asked Questions.

INDIVIDUAL PROPERTY TAX BENEFITS

FEDERAL BENEFITS

You are eligible for a benefit if you belong to one of the following categories of citizens and can confirm this with one of the following documents (supporting documents are in bold and are listed next to the name of each benefit category):

pensioners receiving pensions appointed in the manner prescribed by pension legislation, as well as persons who have reached the age of 60 and 55 years (men and women, respectively), who, in accordance with the legislation of the Russian Federation, are paid a monthly life allowance - pensioner's ID;

disabled people of I and II disability groups - disabled person's certificate;

disabled from childhood disabled person's certificate;

participants in the Civil War, the Great Patriotic War, other combat operations to defend the USSR from among the military personnel who served in military units, headquarters and institutions that were part of the active army, and former partisans, as well as combat veterans;

Heroes of the Soviet Union and Heroes of the Russian Federation, as well as persons awarded the Order of Glory of three degrees - book of the Hero of the Soviet Union or the Russian Federation, order book;

civilians of the Soviet Army, Navy, internal affairs and state security bodies who held full-time positions in military units, headquarters and institutions that were part of the army during the Great Patriotic War, or persons who were in cities during this period, participation in the defense of which is credited to these persons in the length of service for the appointment of a pension on preferential terms established for military personnel of units of the army in the field, – certificate of a participant in the Great Patriotic War or a certificate of the right to benefits;

persons entitled to receive social support in accordance with the Law of the Russian Federation dated May 15, 1991 No. 1244-1 "On the social protection of citizens exposed to radiation as a result of the Chernobyl disaster", in accordance with the Federal Law dated November 26, 1998 No. 175-FZ "On the social protection of citizens of the Russian Federation exposed to radiation as a result of the accident in 1957 at the Mayak production association and the discharge of radioactive waste into the Techa River" and the Federal Law of January 10, 2002 No. 2-FZ "On social guarantees to citizens exposed to radiation as a result of nuclear tests at the Semipalatinsk test site "- a special certificate for a disabled person and a certificate for a participant in the liquidation of the consequences of the disaster at the Chernobyl nuclear power plant, a special certificate issued by the executive authorities of the constituent entities of the Russian Federation, as well as a certificate of a single sample issued in the manner determined by the Government of the Russian Federation the Russian Federation;

military personnel, as well as citizens dismissed from military service upon reaching the age limit for military service, for health reasons or in connection with organizational and staff measures, having a total duration of military service of 20 years or more - a certificate of a military unit or a certificate issued by a district military a commissariat, a military unit, a military educational institution of vocational education, an enterprise, institution or organization of the former USSR Ministry of Defense, the USSR State Security Committee, the USSR Ministry of Internal Affairs and the relevant federal executive bodies of the Russian Federation;

persons who were directly involved in the special risk units in the testing of nuclear and thermonuclear weapons, the elimination of accidents of nuclear installations at weapons and military facilities; - a certificate issued by the Committee of Veterans of Special Risk Units of the Russian Federation on the basis of the conclusion of the medical and social expert commission;

family members of servicemen who have lost their breadwinner, recognized as such in accordance with the Federal Law of May 27, 1998 N 76-FZ "On the Status of Servicemen" - a pension certificate in which the stamp "widow (widower, mother, father) of the deceased soldier" is affixed or there is a corresponding entry, certified by the signature of the head of the institution that issued the pension certificate, and the seal of this institution. If the indicated family members are not pensioners, the benefit is provided to them on the basis of a certificate of death of a serviceman;

citizens dismissed from military service or called up for military training, performing international duty in Afghanistan and other countries in which hostilities were fought - a certificate of entitlement to benefits and certificates issued by the district military commissariat, military unit, military educational institution, enterprise, an institution or organization of the Ministry of Internal Affairs of the USSR or the corresponding bodies of the Russian Federation;

individuals who received or suffered radiation sickness or became disabled as a result of tests, exercises and other work related to any types of nuclear installations, including nuclear weapons and space technology - a certificate of the established form and a certificate of a participant in the liquidation of the consequences of the accident at the Chernobyl nuclear power plant in 1986- 1987 with a stamp (overprint) "flying personnel that participated in nuclear tests";

parents and spouses of military personnel and civil servants who died in the line of duty - a certificate of death of a military serviceman or civil servant, issued by the relevant state bodies;

individuals engaged in professional creative activities - in relation to specially equipped premises, structures used by them exclusively as creative workshops, ateliers, studios, as well as residential premises used to organize non-state museums, galleries, libraries open to the public - for the period their use - a certificate issued by the relevant authority that gives permission for the use of structures, premises or buildings for the above purposes.

Beneficiaries are exempt from paying tax:

one apartment or room;

one residential building;

one garage or parking space.

For the second (third, etc.) apartment, house, garage, etc., owned by the beneficiary, the tax must be paid.

Example: a pensioner who owns a dacha, a garage and two apartments must pay tax on only one of the apartments.

At the same time, all citizens have the right not to pay tax on one household building on a summer cottage with an area of \u200b\u200bno more than 50 square meters. m (for example, on a barn).

ADDITIONAL MOSCOW BENEFITS

In addition to federal benefits, the following benefits are established in the city of Moscow:

1. Benefits for owners of garages and parking spaces located in office and retail facilities (the list of such facilities was approved by Decree of the Government of Moscow of November 28, 2014 No. 700-PP).

You can find out if the building in which your garage or parking space is located is included in the approved list of retail and office facilities using a special service.

More about the benefit:

The exemption is granted in respect of one garage or parking place owned by an individual, with an area of not more than 25 square meters:

for the categories of citizens specified in the "Federal Benefits" section - in the form of a full tax exemption (if they did not use the tax benefit established by Article 407 of the Tax Code of the Russian Federation in relation to a garage or parking space);

2. Benefit for owners of apartments located in a building included in the register of apartments, approved by Decree of the Government of Moscow dated October 26, 2016 No. 706-PP.

For more information on this benefit, please see the "Register of Apartments for Benefit Purposes" section.

PLEASE NOTE THAT TAX BENEFITS DO NOT APPLY TO:

real estate used in business activities;

real estate worth more than 300 million rubles.

If you already applied to the tax authorities with an application for a benefit (for example, after you have retired), then you do not need to do this again - the documents you provided earlier will be taken into account further.

If you not previously filed such an application and are entitled to a tax exemption, then in order to be exempt from paying tax, you need to apply to any tax office with an application and submit documents that confirm that you are entitled to a tax exemption.

Register of apartments for the purpose of granting benefits

Benefit for apartments in retail and office buildings in Moscow

In addition to federal tax benefits, the city of Moscow has a benefit for owners of apartments located in office and retail facilities (the list of such facilities was approved by Decree of the Moscow Government dated November 28, 2014 No. 700-PP).

The exemption is granted in respect of one apartment owned by an individual, which simultaneously satisfies the following conditions:

1) the apartments are located in a building included in the register of apartments, approved by the Decree of the Government of Moscow dated October 26, 2016 No. 706-PP;

2) the area of the apartments does not exceed 300 square meters;

3) the cadastral value of one square meter of apartments is at least 100,000 rubles;

4) the apartments are not the location of the organization;

5) the apartments are not used by the taxpayer in entrepreneurial activities.

The procedure for the formation of the register of apartments was approved by the Decree of the Government of Moscow dated October 26, 2016 No. 705-PP.

If your apartment meets all the above criteria, then the tax rate for the first 150 sq. m of area is reduced from 1.2% to 0.5% of the cadastral value of apartments (by providing a discount to the calculated amount of tax).

The exemption is valid from the tax for 2015 (payable in 2016) and beyond.

DRAW YOUR ATTENTION TO!

The exemption is not granted for any room in the building included in the approved register of apartments, but only for those rooms that simultaneously meet all of the above criteria!

If you want to learn more about this benefit, please read Parts 4-8 of Article 1.1 of the Law of the City of Moscow dated 11/19/2014 No. 51 "On Personal Property Tax".

FREQUENTLY ASKED QUESTIONS ON INDIVIDUAL PROPERTY TAX

- General issues

- Questions regarding taxpayers

- Tax calculation questions

- Questions about tax credits

- Questions about tax deduction

- Questions about the reduction factor

- Procedure and terms of tax payment

- Questions about tax rates

General questions on personal property tax

WHAT CHANGES IN THE RULES OF TAX CALCULATION?

The key change is the transition to the calculation of tax on the cadastral value of real estate. Wherein:

significantly reduced tax rates (3-7 times for most real estate);

mandatory tax deductions have been introduced that reduce the cadastral value of real estate subject to tax;

in order to limit the abuse of privileges, the procedure for granting them has changed: now the privilege applies only to one object of each type - for example, one apartment, one house, one garage, etc. As a result, the practice is becoming a thing of the past when unscrupulous citizens, in order not to pay tax, registered a large number of real estate objects for beneficiaries. Also, benefits do not apply to real estate worth more than 300 million rubles. and real estate used in business activities.

WHEN DO THE NEW TAX CALCULATION RULES COME INTO FORCE?

IS IT TRUE THAT THE TAX AMOUNT WILL INCREASE SIGNIFICANTLY?

For some owners, the tax may indeed increase, while for others it may decrease.

WHAT PROPERTY SHOULD BE TAXED ON?

The new rules for calculating the tax came into force on January 1, 2015, but for the first time it will be necessary to pay the tax calculated according to the new rules only in the fall of 2016.

You must pay tax if you own:

residential building;

living quarters (apartment, room);

garage or parking place;

an object of construction in progress (for example, an unfinished house);

other buildings, structures, structures, premises (for example, apartments, warehouse, office, shop, car service).

If you own a share in real estate, you must pay tax only on your share.

Example: if the tax on an apartment is 2,000 rubles, and you own only half of this apartment, then you need to pay a tax of 1,000 rubles.

WHAT NORMATIVE LEGAL ACTS (LAWS, ETC.) REGULATE THE TAX?

Personal property tax in Moscow is regulated by:

Chapter 32 of the Tax Code of the Russian Federation;

Issues regarding payers of property tax of individuals

WHO MUST PAY TAX?

You must pay tax if you own:

residential building;

living quarters (apartment, room);

garage or parking place;

an object of construction in progress (for example, an unfinished house);

other buildings, structures, structures, premises (for example, apartments, warehouse, office, shop, car service).

If you own a share in real estate, you must pay tax only on your share.

Example: if the tax on an apartment is 2,000 rubles, and you own only half of this apartment, then you need to pay a tax of 1,000 rubles.

SHOULD A MINOR (MINOR) CHILD OWNING AN APARTMENT OR A SHARE IN AN APARTMENT HAVE TO PAY TAX?

The tax must be paid by the child's parents as his legal representatives. In their absence, by adoptive parents, guardians or trustees.

DO I HAVE TO PAY TAX ON THE APARTMENT THAT I RENT OR ON THE APARTMENT THAT IS PROVIDED TO ME UNDER A SOCIAL LEASE?

No, they should not, only the owners of real estate objects pay the tax.

Questions on cadastral value and cadastral registration data

What influences the amount of personal property tax (NIFL)?

WHAT IS CADASTRIAL VALUE?

The cadastral value is the value of real estate determined by the state, close to the market value. It depends on the location of the property (county, district), the year of its construction, the material of the walls, its area, the distance to the nearest metro station, the distance to recreation areas (forest, park, etc.), the fact that the property was recognized as emergency, the prices of real transactions with real estate and some other parameters.

WHERE TO FIND OUT THE CADASTRAL VALUE?

You can find out the cadastral value of your real estate using the Online Reference Information on Real Estate Objects Internet service, which is available on the official website of Rosreestr. You can also apply directly to Rosreestr or to the Centers for the Provision of Public Services of the City of Moscow "My Documents".

HOW IS THE CADASTRIAL VALUE OF MY PROPERTY DETERMINED?

The cadastral value is determined by the mass valuation method based on the information contained in a single database for all real estate objects - the State Real Estate Cadastre. When using the mass valuation method, the characteristics that determine the price of real estate on the market are revealed. Using information about these characteristics and the prices of real estate transactions, an assessment model is built, with the help of which the cadastral value of each property is determined. Since the cadastral value is determined by the mass valuation method, it does not take into account the individual characteristics of a particular apartment, which may affect its market value. That is, for example, the cadastral value of an apartment depends on whether it is located in a brick or panel house, but does not depend on the presence or absence of repairs, furniture and appliances, on where the windows of the apartment go. As a result, the cadastral value of a particular object may differ from its real market price - in order to compensate for this imperfection of the mass valuation, the state has introduced a special tax deduction (For more information about the tax deduction, see Section 7 "Frequently Asked Questions"). Independent appraisers are involved in the state cadastral valuation. The results of determining the cadastral value are approved by the Moscow Government and entered into the State Real Estate Cadastre.

WHY DID THE CADASTRIAL VALUE OF MY REAL ESTATE INCREASE?

The cadastral value could have increased as a result of the revaluation: the cadastral value in Moscow is approved by the Government of Moscow and regularly (since 2015 once every two years) is reviewed in order to fully comply with price changes in the real estate market and take into account the construction of new houses and other real estate objects.

WHAT INFORMATION ABOUT MY REAL ESTATE WAS USED IN DETERMINING THE CADASTRIAL VALUE OF MY REAL ESTATE?

The cadastral value is determined on the basis of information about the location of the property (district, district), the year of its construction, the material of the walls, its area, the distance to the nearest metro station, the distance to recreation areas (forest, park, etc.), the fact of recognition of the property emergency, prices of real real estate transactions and some other information.

I BELIEVE THE CADASTRIAL VALUE OF MY PROPERTY IS DETERMINED INCORRECTLY

If you have information that was used in determining the cadastral value of your property and you think that a mistake was made in determining it (and you have materials confirming your position), then you can contact the Moscow City Property Department.

THE CADASTRAL VALUE SPECIFIED IN THE NOTICE DOES NOT CORRECT WITH THE DATA OF THE CADASTRAL PASSPORT (OTHER DOCUMENT CONTAINING CADASTRAL REGISTRATION INFORMATION)

The cadastral value of real estate objects is regularly (starting from 2015 once every two years) reviewed in order to fully comply with price changes in the real estate market and take into account the construction of new houses and other real estate objects. Thus, the data on the cadastral value in your cadastral passport may not match the actual data on the cadastral value contained in the State Real Estate Cadastre.

WHAT IS A CADASTRIAL NUMBER?

The cadastral number of a real estate object is a unique number of a real estate object assigned to it when entering information about real estate into a single database of all real estate - the State Real Estate Cadastre.

WHERE TO FIND OUT THE CADASTRIAL NUMBER?

You can find out the cadastral number of your property using the Internet service "Reference information on real estate objects online", which is available on the official website of Rosreestr rosreestr.ru. You can also apply directly to Rosreestr or to the Centers for the provision of public services in the city of Moscow "My Documents".

Questions about inventory value

WHAT IS INVENTORY COST?

The inventory cost is the cost of materials, works and services spent on the construction of real estate, taking into account the depreciation of real estate and changes in prices for building materials, works and services.

WHERE TO FIND OUT THE INVENTORY COST?

You can find out the inventory value of your property by contacting the State Budgetary Institution MosgorBTI or the Centers for the Provision of Public Services of the City of Moscow "My Documents".

Questions on the calculation of property tax for individuals

WHY IS THE TAX INCREASED ON THE OBJECT OF REAL ESTATE WHICH I OWN?

The tax on your property could increase as a result of:

- transition to taxation of property from the cadastral value (if the cadastral value of your property is higher than the inventory value);

- applying a higher tax rate to your property;

- restrictions on the effect of the benefit (for example, before the benefit was valid for all real estate objects in your property, and now only for one object of each type - for example, for one apartment, one summer house, one garage, etc.);

- a combination of the above factors.

DOES THE AMOUNT OF TAX DEPEND ON THE NUMBER OF REGISTERED PEOPLE IN THE APARTMENT?

No, the tax is paid by the owner of the apartment, regardless of the number of citizens registered in it.

HOW TO CALCULATE TAX IF I BECOME (OR CEASED TO BE) THE OWNER OF A REAL ESTATE OBJECT DURING THE YEAR ( FOR EXAMPLE, I BOUGHT OR SOLD)?

The tax is paid in proportion to the number of full months during which your property was owned.

In this case, when calculating the tax for the seller, the month in which the object was sold is taken into account if the sale occurred after the 15th day of the month. And for the buyer, the month of purchase is taken into account if the object was purchased before the 15th day of the month (including the 15th day).

HOW IS THE TAX ON NON-RESIDENTIAL PREMISES (SUCH AS APARTMENTS) CALCULATED?

For non-residential premises (for example, for apartments, warehouses), the following rates are set:

2% if the non-residential premises are located in a shopping or office center, which is included in the list determined in accordance with paragraph 7 of Article 378.2 of the Tax Code of the Russian Federation. You can check whether the shopping or office center where your premises are located is included in the list of real estate objects for which the tax base is determined as their cadastral value on the website of the Department of Economic Policy and Development of the City of Moscow;

2% if the cadastral value of the object is more than 300 million rubles;

0.5% for all other cases.

HOW TO CALCULATE TAX IF THE OBJECT OF REAL PROPERTY IS IN COMMON SHARED OWNERSHIP / COMMON JOINT PROPERTY?

For property that is in the common shared ownership of several owners, the tax is paid by each of the owners in proportion to their share in this property.

If you and your spouse have an apartment jointly owned, each of you will pay half of the tax calculated for your apartment as a whole.

HOW TO CALCULATE THE TAX FOR REAL ESTATE OBJECTS RECEIVED BY INHERITED?

The obligation to pay tax arises for the heirs from the moment of the death of the testator or from the date of entry into force of the court decision on declaring the testator dead.

If the death of the testator occurred before the 15th day of the month (inclusive), this month is taken into account for calculating the tax payable by the heir / heiress. If the death of the testator occurred after the 15th day of the month, this month is not taken into account for calculating the amount of tax.

I AM A INDIVIDUAL ENTREPRENEUR USING A SIMPLIFIED TAXATION SYSTEM OR A PATENT TAXATION SYSTEM. WHY DID I RECEIVE A TAX?

Individual entrepreneurs applying the simplified taxation system or the patent taxation system are exempt from paying tax in respect of objects used in entrepreneurial activities, with the exception of retail and office real estate objects included in the list determined in accordance with paragraph 7 of Article 378.2 of the Tax Code of the Russian Federation. You can check whether the shopping or office center where your premises are located is included in the list of real estate objects for which the tax base is determined as their cadastral value on the website of the Moscow Department of Economic Policy and Development.

In addition, individual entrepreneurs applying the simplified taxation system or the patent system are not exempt from paying personal property tax in respect of property used for personal purposes (for example, an apartment in which they live).

Questions about personal property tax exemptions

DOES THE TAX RELIEF INVOLVE TOTAL OR PARTIAL EXEMPTION FROM THE PAYMENT OF TAX?

Tax relief - exemption from paying tax on:

one apartment or room;

alone residential building;

alone garage or parking space.

In addition, individuals engaged in professional creative activities are exempt from paying tax - in relation to one specially equipped premises (structure) used exclusively as a creative workshop, atelier, studio, as well as one residential premises used to organize a non-state open to the public museums, galleries, libraries - for the period of such use.

Also, all individuals (regardless of whether they belong to a preferential category) are exempted from paying tax in relation to one economic building or structure with an area of \u200b\u200bno more than 50 square meters. m and which is located on a land plot provided for personal subsidiary, dacha farming, gardening, horticulture or individual housing construction.

AM I ELIGIBLE FOR TAX REDUCTION? WHAT DOCUMENTS DO I NEED TO PROVIDE TO RECEIVE THE BENEFITS?

You are eligible for a benefit if you belong to one of the following categories of citizens and can confirm this with one of the specified documents (supporting documents are highlighted bold font and are indicated next to the name of each preferential category):

1) pensioners receiving pensions appointed in the manner prescribed by pension legislation, as well as persons who have reached the age of 60 and 55 years (men and women, respectively), who, in accordance with the legislation of the Russian Federation, are paid a monthly life allowance - pensioner's ID;

2) disabled people of I and II disability groups - disabled person's certificate;

3) disabled since childhood - disabled person's certificate;

4) participants in the Civil War and the Great Patriotic War, other military operations to defend the USSR from among the servicemen who served in military units, headquarters and institutions that were part of the army in the field, and former partisans, as well as veterans of military operations -

5) Heroes of the Soviet Union and Heroes of the Russian Federation, as well as persons awarded the Order of Glory of three degrees - book of the Hero of the Soviet Union or the Russian Federation, order book;

6) civilians of the Soviet Army, the Navy, internal affairs and state security agencies, who held full-time positions in military units, headquarters and institutions that were part of the army during the Great Patriotic War, or persons who were during this period in cities, participation in the defense of which is counted by these persons in the length of service for the appointment of a pension on preferential terms established for military personnel of units of the army in the field - certificate of a participant in the Great Patriotic War or a certificate of the right to benefits;

7) persons entitled to receive social support in accordance with the Law of the Russian Federation of May 15, 1991 N 1244-1 "On the social protection of citizens exposed to radiation as a result of the Chernobyl disaster", in accordance with the Federal Law of November 26, 1998 of the year N 175-FZ "On the social protection of citizens of the Russian Federation exposed to radiation as a result of the accident in 1957 at the Mayak production association and the discharge of radioactive waste into the Techa River" and the Federal Law of January 10, 2002 N 2-FZ "On social guarantees to citizens exposed to radiation as a result of nuclear tests at the Semipalatinsk test site "- a special certificate for a disabled person and a certificate for a participant in the liquidation of the consequences of the disaster at the Chernobyl nuclear power plant, a special certificate issued by the executive authorities of the constituent entities of the Russian Federation, as well as a certificate of a single sample issued in the manner determined by the Government m of the Russian Federation;

8) military personnel, as well as citizens dismissed from military service upon reaching the age limit for military service, for health reasons or in connection with organizational and staff measures, having a total duration of military service of 20 years or more - a certificate of a military unit or a certificate issued by a district a military commissariat, a military unit, a military educational institution of vocational education, an enterprise, institution or organization of the former USSR Ministry of Defense, the USSR State Security Committee, the USSR Ministry of Internal Affairs and the relevant federal executive bodies of the Russian Federation;

9) persons who were directly involved in the special risk units in the testing of nuclear and thermonuclear weapons, liquidation of accidents of nuclear installations at weapons and military facilities - a certificate issued by the Committee of Veterans of Special Risk Units of the Russian Federation on the basis of the conclusion of the medical and social expert commission;

10) members of the families of military personnel who have lost their breadwinner - a pension certificate in which the stamp "widow (widower, mother, father) of the deceased soldier" is affixed or there is a corresponding record certified by the signature of the head of the institution that issued the pension certificate and the seal of this institution. If the indicated family members are not pensioners, the benefit is provided to them on the basis of a certificate of death of a serviceman;

11) citizens dismissed from military service or called up for military training, performing international duty in Afghanistan and other countries in which hostilities were fought - a certificate of the right to benefits and certificates issued by the district military commissariat, military unit, military educational institution, enterprise , an institution or organization of the Ministry of Internal Affairs of the USSR or the relevant bodies of the Russian Federation;

12) individuals who received or suffered radiation sickness or became disabled as a result of tests, exercises and other work related to any types of nuclear installations, including nuclear weapons and space technology - a certificate of the established form and a certificate of a participant in the liquidation of the consequences of the accident at the Chernobyl nuclear power plant in 1986 - 1987 with a stamp (overprint) "flying personnel involved in nuclear tests";

13) parents and spouses of military personnel and civil servants who died in the line of duty - certificates of death of a military serviceman or civil servant issued by the relevant state bodies;

14) individuals engaged in professional creative activities - in relation to specially equipped premises, structures used by them exclusively as creative workshops, ateliers, studios, as well as residential premises used to organize non-state museums, galleries, libraries open to the public, - for the period of such use - a certificate issued by the relevant authority that gives permission for the use of structures, premises or structures for the above purposes.

I BELONG TO THE PREFERENT CATEGORY OF CITIZENS. WHY DID I RECEIVE A TAX?

The benefit is valid for one object of each type. A citizen who belongs to the preferential category of citizens is exempted from paying tax in respect of one apartment, one cottage and one garage. But he is obliged to pay tax on the second apartment in the property (for the second cottage, the second garage).

In addition, the benefit is not available if:

the property is used for business purposes;

the property has a cadastral value of more than 300 million rubles;

the object is located in a large shopping or office center included in the list of real estate objects in respect of which the tax base is determined as their cadastral value.

You can check whether the shopping or office center where your premises are located is included in the list of real estate objects for which the tax base is determined as their cadastral value on the website of the Moscow Department of Economic Policy and Development.

Also, you may not have applied for a tax relief.

HOW TO GET TAX REDUCTION?

To receive a tax benefit, you need to apply to any tax office with an application for a benefit and documents confirming the right to a benefit. In addition, you can submit an application electronically through the "Taxpayer's Personal Account" Internet service on the website of the Federal Tax Service of Russia (registration is required).

IF THERE ARE SEVERAL OWNERS, WILL THE BENEFITS PROVIDED TO ONE OF THEM APPLY TO THE ENTIRE PROPERTY? MY WIFE (HUSBAND) AND I HAVE AN APARTMENT IN SHARE (JOINT) OWNERSHIP, AND ONLY ONE OF US IS RIGHT TO BENEFITS - WILL I HAVE TO PAY TAX?

If you and your wife/husband have an apartment in joint ownership, and only you have the right to a benefit, your wife/husband will have to pay tax in proportion to her/his share in the property.

IS IT NEEDED TO RE-SUBMIT THE DOCUMENTS CONFIRMING THE RIGHT TO TAX BENEFITS IF THEY HAVE ALREADY BEEN SUBMITTED TO THE TAX AUTHORITY?

No, if you have already been granted a tax benefit, then you do not need to re-submit documents to the tax authority.

WHEN SHOULD I PROVIDE THE NOTIFICATION TO THE TAX AUTHORITY ON THE SELECTED TAX OBJECTS FOR WHICH THE TAX REDUCTION WILL BE PROVIDED?

If you do not notify the tax authorities, the tax credit will be granted in respect of one property of each type of property with the maximum assessed amount of tax (that is, in relation to the largest and/or most expensive property).

Notification of the selected objects of taxation must be sent to the tax authorities only if you want to change the property subject to the exemption.

Notification of the selected objects of taxation must be sent to the tax authorities if you want to independently choose the property subject to the exemption.

The notification must be sent to the tax authorities before November 1 of the year in which you want to receive a benefit in relation to this object. For example, if you want the 2015 tax credit to apply to a specific apartment of two apartments in your property, then notice must be sent by November 1, 2015.

However, if you do not notify the tax authorities, the tax credit will be granted in respect of one property of each type of property with the maximum amount of tax calculated (that is, in relation to the largest and / or most expensive property).

IS THERE ANY TAX REDUCTION FOR NON-RESIDENTIAL PREMISES (SUCH AS APARTMENTS)?

The exemption is only available for the following non-residential premises:

- Garage, parking space.

- Specially equipped premises, a structure used exclusively as a creative workshop, atelier, studio, as well as residential premises used to organize a non-state museum, gallery, library open to the public - for the period of such use.

- An economic building or structure with an area of not more than 50 square meters. m and which is located on a land plot provided for personal subsidiary, dacha farming, gardening, horticulture or individual housing construction.

The exemption does not apply to other non-residential facilities (including apartments).

WILL THE TAX AMOUNT WILL BE RECALCULATED IF I AM IN THE PREFERENTIAL CATEGORY BUT I HAVE NOT NOTIFIED THE TAX AUTHORITIES ABOUT IT?

Yes, after submitting the documents confirming your right to the benefit, the amount of tax can be recalculated, but not more than 3 years and not earlier than the date of occurrence of the right to the tax benefit. For example, if you became a pensioner in 2010, but submitted supporting documents to the tax authorities in 2015, you will be recalculated tax for 2014, 2013 and 2012.

Questions on the tax deduction for calculating the tax on property of individuals

Tax deduction when paying personal property tax (NIFL)

HOW IS THE AREA OF THE DEDUCTION IN THE NOTICE FOR THE PAYMENT OF TAX DETERMINED?

The deduction area is set depending on the type of property:

10 sq. m for the room;

20 sq. m for an apartment;

50 sq. m for home.

HOW IS THE CADASTRAL DECUTATION VALUE DETERMINED?

The cadastral value of the deduction is calculated as the area of the deduction (10 sq. m for a room / 20 sq. m for an apartment / 50 sq. m for a house) multiplied by the cadastral value of 1 sq. m. m of the property.

Cadastral value of 1 sq. m is determined by dividing the total cadastral value of the property by its area. For information on where to find out the cadastral value, see Section 3 of the Frequently Asked Questions.

HOW IS THE TAX DREDUCTION CALCULATED IF THE REAL ESTATE IS IN COMMON SHARING OWNERSHIP / COMMON JOINT PROPERTY?

The tax deduction applies to the property as a whole, regardless of the number of owners. That is, the tax deduction will be the same for an apartment with three owners and for an apartment with one owner.

IS THERE A TAX DREDUCTION FOR NON-RESIDENTIAL PREMISES (SUCH AS APARTMENTS)?

No, the tax deduction is not available for non-residential premises, including apartments.

Questions on the reduction coefficient for calculating the tax on property of individuals

WHAT IS A REDUCTION FACTOR?

This is a coefficient that reduces the amount of the calculated tax on the property of individuals. In order to ensure a smooth transition to the payment of tax calculated according to the new rules, the state has introduced a transitional reduction coefficient, which reduces the amount of tax. As a result of applying this coefficient when calculating the tax for 2015-2018, you will pay the full amount of tax on your property only in 2020.

HOW WILL THE REDUCTION FACTOR VALUES BE CHANGED?

The value of the reduction factor depends on the year for which the tax is calculated. The following values of the reduction factor are set:

Reduction factor

does not apply to tax

The procedure and terms for paying tax on property of individuals

WHEN WILL I GET A INDIVIDUAL PROPERTY TAX NOTIFICATION?

Tax notices are sent by the tax authorities by November 1 of the year following the tax calculation year (i.e. tax notices for 2015 will be sent to you by November 1, 2016). If you are registered in the Taxpayer's Personal Account Internet service on the website of the Federal Tax Service of Russia, a tax notice with a receipt will be sent to you electronically. If you are not registered with this service, a tax notice with a receipt will be mailed to you.

WHEN SHOULD YOU PAY TAX?

WHAT SHOULD I DO IF I DID NOT RECEIVE A TAX NOTIFICATION AND I OWNED THE PROPERTY IN THE LAST YEAR?

If you owned a property last year and did not receive a tax notice this year, you must report the property you own or have owned to the tax authorities.

DO I HAVE TO CALCULATE TAX AND FILE THE TAX RETURN BY MYSELF?

No, the tax authorities calculate the amount of tax and send you a tax notice with a tax receipt.

CAN I PAY TAX ONLINE? HOW SHOULD I DO IT?

Yes, you can. For this you need to use:

Internet service "Payment of taxes of individuals" on the website of the Federal Tax Service of Russia nalog.ru

Internet service "Personal account of the taxpayer" (registration required) on the website of the Federal Tax Service of Russia nalog.ru.

Using these services, you can generate a tax receipt for payment in any bank for cash or make a cashless payment on the website of the Federal Tax Service of Russia (you can see the list of banks for cashless payment on the website of the Federal Tax Service of Russia).

WHAT HAPPENS IF I DON'T PAY TAX?

In case of non-payment of tax within the time limits established by law, you will be charged penalties (1/300 of the Central Bank refinancing rate) for each day of delay. In this case, the tax authority has the right to apply to the court with an application for the collection of the amount of tax at the expense of your property, including cash and money in bank accounts. Subsequently, if you refuse to pay off the debt by a court decision, the bailiff has the right to issue a decision on you to temporarily restrict your exit from Russia, as well as to seize your property.

Questions about tax rates

WHAT TAX RATES APPLY IN MOSCOW?

For apartments, rooms, residential buildings, outbuildings on a summer cottage (if the area of such a building is not more than 50 sq. m), the tax rate depends on the cadastral value.

|

Cadastral value of an apartment/room/residential building |

tax rate |

|

up to 10 million rubles |

|

|

from 10 to 20 million rubles. |

|

|

from 20 to 50 million rubles. |

|

|

from 50 to 300 million rubles. |

For garages and parking spaces - 0,1% .

For unfinished private residential buildings - 0,3% .

For objects of taxation (non-residential premises, garages, parking spaces) in office and retail facilities (the list of such objects was approved by the Decree of the Government of Moscow of November 28, 2014 No. 700-PP):

1,2% for tax for 2015 (payable in 2016);

1,3% for tax for 2016 (payable in 2017);

1,4% for tax for 2017 (payable in 2018);

1,5% for tax for 2018 and subsequent years (payable in 2019 and beyond).

You can find out if the building in which your non-residential premises, garage or parking space are located is included in the approved list of retail and office facilities using a special service.

For any real estate with a cadastral value of more than 300 million rubles. - 2% .

For other non-residential real estate (for example, for a warehouse, industrial building) - 0,5% .

WHAT RATE IS THE APARTMENT TAXED?

Please note that the apartments are non-residential premises.

Therefore, when calculating the apartment tax:

tax rates for non-residential premises apply:

- 1,2% for tax for 2015 (payable in 2016) - if the apartment is located in a retail or office building;

- 0,5% - in other cases;

no federal tax credits;

At the same time, a Moscow benefit is provided for owners of apartments located in a building included in the register of apartments, approved by Decree of the Government of Moscow dated October 26, 2016 No.

no tax deductions apply.

You can get useful information for us, taxpayers, regarding what benefits are available in a particular region or municipality for property taxes (transport tax, land tax and personal property tax) by contacting a special service on the official website of the Federal Tax Service of Russia “Reference Information on rates and privileges on property taxes.

This electronic service allows you to find out everything about the regulations that establish payment deadlines, tax rates and benefits.

Of course, we must remember that the order of granting benefits is declarative in nature. This means that the benefit itself will not come to you and me. In order to get it, you must independently submit to the tax office, at the place of registration of the object of taxation (land, transport, real estate) an application and documents confirming our right to the benefit.

Then a recalculation of the specified taxes will be made. True, recalculation, in accordance with applicable law, can be made for no more than three previous years. But it's still nice!

Example: pensioners receiving pensions in accordance with the pension legislation of the Russian Federation are exempt from paying personal property tax. In order to receive a tax exemption, when you retire, you need to contact the tax office with a pension certificate and a corresponding application. (You can find out the address of the tax authority using the service "Address and payment details of your inspection" on the same website of the Federal Tax Service)

If the taxpayer, in the future, does not change his place of residence, the submission of such an application is not required again.

But in relation to the land tax, in some cases, the benefit must be confirmed annually. For example, disability in accordance with the procedure for re-examination is confirmed annually, and therefore, it is also necessary to submit a tax application with a new supporting document every year.

Car owners are required, as you know, to pay transport tax. Therefore, you should not forget to remove your sold car from the registration with the traffic police in a timely manner. Because the transport tax is calculated on the basis of the information provided by the traffic police.

Transport tax is not charged: in case of deregistration of the vehicle in the registration authorities; if the car is wanted, provided that the fact of car theft is confirmed by the original certificate of theft issued by the bodies of the Ministry of Internal Affairs of Russia.

Also, information on the provision of property tax benefits can also be found in the tax notice or use the “Taxpayer Personal Account for Individuals” service. To obtain a registration card and access to this service, the taxpayer must personally apply to any inspection of the Federal Tax Service of Russia with an identity document.

Personal property tax (hereinafter referred to as tax) is a mandatory annual payment for owning property: an apartment or a room; residential building; a room or structure, an outbuilding, a garage or a parking space. The tax is calculated on each individual object. If the object belongs to several owners, then the tax is determined in proportion to the shares for each owner.

What's new in 2015?

Previously, the personal property tax was approved by federal and local laws. To give importance to this tax, in 2015, Chapter 32 appeared in the Tax Code of the Russian Federation (TC RF) on the basis of the Law signed by the President of Russia. It is called: “Tax on the property of individuals”. This chapter allows municipal entities and cities of federal significance (Moscow, St. Petersburg and Sevastopol) to increase the property tax for individuals in order to replenish the local budget through this.

How was property tax calculated?

Since this is a local tax, it is transferred to the local budget. As before, so now it is considered and collected by the tax authorities according to the laws of the Local Authorities. Thus, the sum of the share of the value of the property of all its owners appears in the local budget. Each municipal entity independently sets tax rates, without going beyond the limits established by federal law. The value of the property was determined by the inventory value - the amount needed to restore a residential building minus depreciation, taking into account the coefficients for each object. The inventory value of the objects was carried out every year by the Bureau of Technical Inventory (BTI). The tax was defined as the inventory value of the property multiplied by the tax rate.

What caused the introduction of coordinating changes?

The transition to tax calculation from inventory to cadastral value is caused by the need to restore the principles of social justice and equality. That's what the authorities think. The method of calculation has become obsolete, does not correspond to reality. It was created when there were no market relations in the country yet. In some cases, the inventory value is many times lower than the market value, since it does not take into account indicators that significantly affect the value of the property. These are indicators such as the location of the object, its size. With this assessment, a two-room apartment on the outskirts of the city may be more expensive than a five-room apartment in the city center. And accordingly, the tax on kopeck piece will be higher, and this is unfair.

What changes have been made by Chapter 32 of the Tax Code of the Russian Federation?

Starting from 2015, the tax authorities will calculate the tax on the cadastral value of the property, which is calculated and established by the Federal Service of Cadastre and Cartography (Cadastral Chamber). Since December 2012, the cadastral value of apartments has increased several times and approached the market value. Tax rates, as before, can be set by local authorities, issuing local laws, without going beyond the Federal Law.

How much will you have to pay?

To determine how much you will have to pay for your property, you need to know exactly the tax base (cadastral value of the object) from which the tax will be calculated and, of course, the tax rate. You can get acquainted with the tax rates in the Decisions of local authorities for Municipalities independently. Information about the current rates and benefits for property taxes is on the main page of the website of the Federal Tax Service of Russia in the electronic services section. Service "Reference information on rates and benefits for property taxes".

In most subjects, a minimum rate of 0.1% is accepted for residential properties.

The tax base - the cadastral value - is also known and available to everyone.

How is the tax base determined?

The tax base is the cadastral value of the property, which can be found on the website

Rorestra. To do this, you need to use the electronic service "Reference information on real estate objects online". Information on the cadastral value of property can be obtained free of charge in the form of a cadastral certificate. For this you need:

1. Go to the site rosreestr.ru

2. Select the electronic service "Obtaining information from the State Property Committee"

3. Order a "Cadastral certificate of the cadastral value of the property" for the object of interest.

4. Receive the Xml help file and access key by e-mail, specifying it in the request

5. Using the electronic service "Checking an electronic document" open the help.

And so we move on. Suppose you have found the cadastral value of your property. But this is not yet a tax base. The legislation provides for a reduction in the cadastral value for all citizens by the so-called deduction, in other words, the State exempts part of the housing from tax. For different categories, the law sets its own minimum deductions (local authorities can increase them)

*If there are 2 houses on one summer cottage, then the owners of "single real estate complexes" will save 1 million rubles on the deduction, regardless of the total area.

Tax Calculation Examples

Flat

Area 57 sq.m, cadastral value 2,200,000, tax rate 0.1%

The cost of 1 sq. m.: 2,200,000 / 57 = 38,596

Tax base: 38,596 * (57 - 20) = 1,428,052, where 20 sq.m.

Tax amount: 1,428,052 * 0.1% = 1428.05 rubles.

Area 29 sq.m., cadastral value 1,100,000, tax rate 0.1%

The cost of 1 sq. m.: 1,100,000 / 29 = 37,931

Tax base: 37,931 * (29 - 10) = 720,689, where 10 sq.m.

Tax amount: 720,689 * 0.1% = 720.69 rubles.

House

Area 150 sq.m., cadastral value 5,500,000, tax rate 1%

The cost of 1 sq. m.: 5,500,000: 150 = 36,667

Tax base: 36,667 * (150 - 50) = 3,667,700, where, 50 sq.m is a benefit

Tax amount: 3,667,700 * 0.1% = 3666.7 rubles.

Single real estate complex (two houses)

Area 300 sq.m., cadastral value 8,000,000, tax rate 0.1%.

Tax base: 8,000,000 - 1,000,000 = 7,000,000, where 1,000,000 is a benefit

Tax amount: 7,000,000 * 0.1% = 7,000 rubles.

In addition, when calculating the tax for 4 years, reduction factors for years will be taken into account. 0.2;0.4; 0.6; 0.8. Thus, the tax increase will be gradual.

What is the worst option for all citizens?

New Article 406 of the Tax Code of the Russian Federation defines tax rates for property tax, which is calculated based on the cadastral value:

The law limits the scope of rates that local authorities can set. Paragraph 3 of Article 406 of the Tax Code of the Russian Federation states that local authorities can reduce tax rates to zero or increase, but not more than three times. As for the "reduce" we do not even dream of. But in the worst case, we will have to pay for housing at a rate of 0.3%. This means that the tax base will need to be multiplied by 0.003 and we will get the amount that will have to be paid annually to the municipal budget.

How can citizens themselves find out how much they will have to pay?

To calculate the property tax on property objects located in different regions of the Russian Federation, you can use the service of the Federal Tax Service of Russia “Preliminary calculation of property tax on individuals based on the cadastral value”. The service is located on the main page of the website of the tax service in the block "Individual property tax"

In those regions where the transition to determining the tax on the cadastral value of property has been adopted, citizens can more accurately calculate how much their tax on an apartment will increase.

How much will the tax increase in cities, especially in large ones?

The law will hit hardest those who live in large apartments in the city center. If housing costs more than 300 million rubles, you will have to pay 2% of the tax base. This is a significant amount. Some owners with an area of more than 1000 sq.m. will have to pay in the range of 5-7 million rubles a year, which is 100 or more times more than before the adoption of the law. So let's hope that the family budget of ordinary citizens with their modest square meters will not suffer much with the introduction of a new method of tax calculation.

How to check or dispute the cadastral value of housing?

If the cadastral value is higher than the market price, which we can determine from the information of real estate transactions. If Rosreestr made a mistake, for example, overestimated the area of the apartment or incorrectly assessed it according to some other criterion, then the owner of the apartment can go to court. For example, if the assessment does not pay attention to the fact that the house is located in an industrial area, or major repairs have not been carried out for several years, there is no playground and parking in the yard, and several kilometers to the nearest school and clinic, the court may again recognize such an assessment unreasonable. An application for revision of the cadastral value may be filed with the court no later than five years from the date of entering the disputed results into the state real estate cadastre.

Have the benefits been maintained?

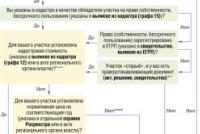

As before, pensioners, disabled people of groups I and II, disabled children, the military and several other categories of citizens are still exempt from property tax. Large families are not included in this list. Under the new legislation, the exemption is valid only for one object, but for each type of property: an apartment or a room; House; premises or building; economic building or structure; garage or parking space. For example, if you are a pensioner and you have 2 apartments, then you will have to choose which apartment does not pay tax. To do this, you will need to submit a Notification on the choice of a preferential apartment to the tax authority before November 1, 2015 for the tax period 2015.

When can we expect the results of the new law?

Starting from the tax period of 2015 and until 2020, at the choice of regions, regions, territories, the tax base can be the cadastral value or inventory value, while taking into account the deflator coefficient.

On January 1, 2015, in order to introduce a property tax, each region had to:

1) determine the procedure for determining the cadastral value of property;

2) establish a single date from which the tax base for tax in the region will be determined based on the cadastral value.

At the same time, it should be taken into account that the regions have the right to introduce a new tax calculation procedure as early as January 1, 2015. However, to do this, they must adopt and publish the relevant regional law no later than December 1, 2014. Therefore, the Tax Calculation Method will not change immediately. The regions have until 2020 to decide at what point they will switch to the new system. After that, the tax will gradually increase over 4-5 years. So in some regions, the new procedure has already been introduced and everyone will know when they receive a tax receipt in 2016 for 2015 with a payment deadline of October 1, 2016.

By TIN or SNILS

By tax document index (UIN)

To search for taxes, enter the TIN or SNILS number. We recommend checking both documents at the same time.

?

?

To search for taxes and penalties in the GIS GMP system

To search for a tax, enter the number of the Tax Document or the unique accrual identifier (UIN).

?

To check taxes and penalties on already issued Tax Documents Search taxes »

By clicking the "Search for taxes" button, you consent to the processing of personal data, in accordance with the Federal Law of July 27, 2006 N152-Ф3 "On Personal Data"

* The search is performed in the GIS GMP (taxes issued throughout Russia).

Our service allows you to check and pay online taxes for individuals: transport tax, land tax, property tax for individuals. Verification is carried out by TIN, SNILS or document index (UIN). Registration is not required.

Tax verification is carried out on the basis of the "State Information System on State and Municipal Payments" (abbreviated as GIS GMP). This database contains data on all tax charges in Russia.

In case of detection of tax accruals or debts, you can immediately pay them, MasterCard, Visa, MIR bank cards are accepted as a means of payment.

How to check taxes by TIN or UIN?

In order to check tax accruals and debts, you will need the number of one of the following documents:

- TIN - Taxpayer Identification Number

- SNILS - Insurance number of an individual personal account in the Pension Fund of Russia (green plastic card)

- UIN or document index - the number of the notification of the Federal Tax Service on accrued taxes

Checking taxes is carried out by the number of the document entered in the appropriate fields of the search form. You can check taxes by specifying both documents at the same time. SNILS number is entered without hyphens and spaces, only numbers.

By TIN or SNILS, you can only find out tax arrears, that is, accruals that were not paid within the period established by law. Current tax accruals can only be found by UIN.

After entering the data in the fields of the search form, click the "SEARCH TAXES" button. Tax review may take a long time, please wait for the result.

If taxes are found as a result of the check, detailed information will be provided: date, UIN, type of tax, amount payable, and so on. Otherwise, a message will appear stating that nothing was found.

Reference information on taxes of individuals

Below you will find answers to basic questions about personal taxes. If you did not find the answer to your question - send it through the feedback form.

What taxes do individuals have to pay?

Individuals pay the following types of taxes: tax on property of individuals, transport and land.

Can I check taxes by last name?

You cannot check taxes by the name of an individual. It is obvious that in Russia there are a huge number of people with a completely matching last name, first name and patronymic. In such a situation, checking taxes by last name would produce a meaningless result.

How to check taxes on passport data?

It is impossible to find out taxes directly from the passport data. However, there is a workaround - according to passport data, on the nalog.ru website, you can find out the TIN and then check taxes by TIN.

How to find out your TIN?

You can find out the TIN of an individual, according to passport data, on the website of the Federal Tax Service Nalog.ru - https://service.nalog.ru/inn.do

Is it possible to find out land tax by cadastral number?

Unfortunately, it is impossible to find out the charge of land tax by cadastral number. This tax can only be recognized by the TIN of the land owner or UIN.

Is it possible to find out taxes by last name on the nalog.ru website?

As noted above, on no site, including www.nalog.ru ( instructions for working with the site), you can not find out tax charges and debts by last name.

Is it possible to check taxes on the website of the Federal Tax Service (nalog.ru) without registration?

Checking taxes on the site nalog.ru without registration is not possible. Information on tax charges on the website of the Federal Tax Service is available only through the personal account of the taxpayer. To obtain a login and password, you can contact any inspection of the Federal Tax Service, regardless of the place of residence and registration. You must have a passport and an original / copy of the registration certificate with you.

How long does it take to pay personal taxes?

In accordance with the amendments made by Federal Law No. 320-FZ of November 23, 2015 to Part Two of the Tax Code of the Russian Federation, taxes must be paid no later than December 1 of the year following the expired tax period. For example, the tax on property of individuals, transport and land tax for 2018 must be paid no later than December 1, 2019. Taking into account the fact that December 1, 2019 falls on a day off - the deadline for paying taxes without penalties is December 2, 2019.

What happens if you don't pay taxes?

In the case when the taxpayer does not pay taxes, the Federal Tax Service forms a requirement for the payment of tax, penalties, fines. If the taxpayer fails to comply with the requirement for payment within the period specified in this requirement, the tax authority begins the procedure for collecting debts on mandatory payments to the budget system of the Russian Federation.

Debt collection from individuals who are not individual entrepreneurs is carried out under two conditions:

- the debtor has an unfulfilled obligation in the amount exceeding 3,000 rubles;

- the expiration of a three-year period for fulfilling the requirement for payment, if the total amount of unpaid taxes, fees, penalties, fines by the taxpayer does not exceed 3,000 rubles

In these cases, an application for recovery at the expense of the property of a taxpayer - an individual is submitted by the tax authority to the court upon the occurrence of one of the above conditions.

How to find out the UIN of the tax accrual?

Every year, the Federal Tax Service sends out a tax notice by mail, along with a receipt for payment. UIN is designated as a document index, consists of 20 digits and is located at the top of the receipt.

If you have not received a tax notice, then you can view it in the taxpayer's personal account or receive it by contacting the IFTS in person.

How do I get a tax deduction for personal property tax?

To begin with, it is necessary to clarify what a tax deduction is in relation to the property tax of individuals. In accordance with paragraphs 3-5 of Article 403 of the Tax Code of the Russian Federation:3. The tax base for an apartment is defined as its cadastral value reduced by the cadastral value of 20 square meters of the total area of this apartment.

4. The tax base for a room is determined as its cadastral value reduced by the cadastral value of 10 square meters of the area of this room.

5. The tax base for a residential building is defined as its cadastral value reduced by the cadastral value of 50 square meters of the total area of this residential building.

Thus, the tax deduction in relation to the tax on the property of individuals is a decrease in the tax base by the amount of the cadastral value of a certain area of the property.

For example, for an apartment of 50 square meters, the tax will be charged as follows. The cadastral value of the apartment must be divided by the area, the resulting cadastral value per square meter of area multiplied by 20 (tax deduction) and the resulting value subtracted from the cadastral value. specific calculation. An apartment with an area of 50 meters and a cadastral value of 10 million rubles. 10 million / 50 = 200 thousand rubles is the cadastral value of a square meter. Multiply 20 meters of tax deduction by 200 thousand = 4 million rubles. Calculation of the tax base: 10 million - 4 million = 6 million rubles. The tax deduction is calculated automatically, so no action is required to receive it.

It is important to understand that the tax deduction applies to the property and not to the individual. In other words, if an apartment of 80 square meters has 4 owners, the apartment tax will still be calculated based on the cadastral value of 60 square meters. Each of the owners, subject to equal shares, will actually receive tax charges for 15 sq. meters.

If an individual has several apartments, the tax deduction will be applied to each apartment.